Let’s say you have a successful business Widgets Pty Ltd, which is looking for bigger commercial premises to expand but the cost is out of your personal or SMSF budget on their own.

One way you can purchase a property with your SMSF and a related party as co-owners is to establish a unit trust to purchase the property. For this to work you must ensure that the strategy complies with the SIS Act 1993 and in particular Regulation 13.22C of the Superannuation Industry (Supervision) Regulations 1994 at all times.

Here is a simple practical example of how this strategy works:

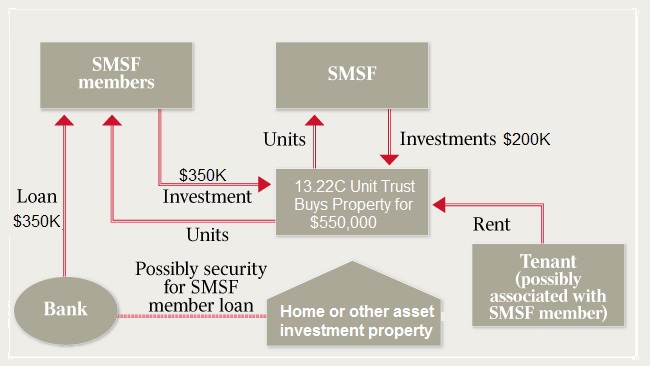

Nancy & Colin have an SMSF that has $250,000 that they would like to invest in a commercial property. In their personal names, they also have the ability to borrow $350,000 against their home that they would like to invest in property.

A unit trust is established and their SMSF purchases $200,000 of units leaving $50,000 liquidity in the fund and they purchase $350,000 of the units personally which funds the unit trust with $550,000 in cash and the SMSF owning 36% and Nancy & Colin owning 64%.

The unit trust then uses this money to purchase an Industrial Unit/ commercial property, pay for any purchase costs such as transfer duty and legal fees and maintains some extra funds in a bank account for some liquidity.

The unit trust enters into the lease with Widgets Pty Ltd as tenants, receives the rent and pays the expenses such as rates, insurance and repairs. The net income is then distributed to the unit holders based on their ownership. In the scenario above the super fund would receive 36% of the net rent and Nancy & Colin would receive 64%. Each owner would include their share of the income in their tax returns.

This is called a 13.22C Ungeared Trust and works well for simple scenarios where you wish to buy a property and your SMSF can contribute towards the cost.

Advantages:

- The SMSF can in later years later acquire more units from the related party which allows it to increase its ownership of the property. The idea would be to have the property eventually owned 100% by the fund and the money paid to Nancy & Colin for the units is used to pay down their personal loan. This is not possible when a Self Managed Super Fund and related party co-own a property as tenants in common unless it is business real property;

- The related party and/or the SMSF can subscribe to new units in disproportionate amounts if more capital is needed for improvements or renovations;

- The related party (Nancy & Colin in the above example) can borrow to acquire their units in the unit trust (generally by offering another asset such as their home as security) and then claim the interest on the loan as a personal tax deduction because the trust is income-producing. This effectively allows them to gear their share of the ownership much like they would if they owned it as a tenant in common with the SMSF.

Disadvantages:

- The unit trust must comply with the provisions of 13.22c at all times. Any breach of any of the provisions will mean that the trust is subject to the in-house asset rules which limit the value of this investment in the fund to 5% of its assets. This almost always means that the SMSF must dispose of its investment in the trust even if the breach is rectified;

- There are additional costs to establish this structure due to the set-up of a unit trust (and corporate trustee if desired);

- There are additional costs to run this structure because the unit trust is a separate entity and must lodge a tax return;

SUMMARY OF 13.22c RULES:

To meet the requirements of SIS regulation 13.22C, the trust must:

- Be a unit trust;

- Have no debt and not allow any security to be taken over its assets;

- Have no lease arrangement with a related party other than one relating to business real property;

- Not acquire an asset (other than business real property) from a related party;

- Not lend money to any entity other than an authorised deposit taking institution (eg, a bank);

- Not conduct a business. Therefore, depending on the size and scale of the development, the trustee should consider engaging a third party to develop the land for a fee.; and

- Not own an interest in another entity – which means it cannot own shares or invest in another trust.

Broadly, this means the trust will only own residential or business real property and cash on deposit.

Other consequences you may have to consider

- Some of the transactions outlined above could have capital gains tax (CGT) implications and

- may be subject to duty as the trust may be or in the future become be a ‘land rich entity’ under the various state Duty Acts.

However, with careful planning, these outcomes can be managed in some circumstances. For example:

- If the Units are disposed of by the SMSF during pension phase they would generally be CGT-free;

- Some of the different States Duty Acts offer concessions in some form or another where there are transactions between an SMSF and its members; and

- The related party may be able to utilise the small business CGT concessions when disposing of units in the trust.

Not a strategy to prop up a failing business:

A holding in a 13.22C trust that is not owned by an SMSF may be offered as security for a loan. If this is done, the interest would potentially be available to the owner’s creditors if the business failed.

SMSF trustees who co-invest in such a trust need to consider the risks involved, which could be considerable if the SMSF is a minority unit holder and the trust came to be directly controlled by creditors.

The trustee of the unit trust would need to conduct its affairs on a purely arm’s length basis to avoid audit problems for the SMSF investors including:

- Putting in place a lease agreement on commercial terms

- Ensuring rents are collected promptly and no leeway uis provided because of the relationship (you need to be as hard or harder than if you were unrelated)

- Ensuring proper liability insurance and property insurance is maintained on the property.

As mentioned above if any of the conditions in Regulation 13.22C are not satisfied, the SMSF’s units in the unit trust will be treated as an in-house asset of the SMSF and the in-house exception in Regulation 13.22C cannot be subsequently applied even if the breach is rectified (refer to Regulation 13.22D(3)).

We also refer you to Taxpayer Alert TA 2012/7 where the ATO warns SMSF trustees and advisors to exercise care ensuring any arrangements entered into by a SMSF to invest in property are properly implemented, particularly those involving LRBAs or the use of a related unit trust.

This is a strategy where you must include your Accountant and a SMSF Specialist Advisor to ensure you get the process correct and run the strategy correctly going forward. We are happy to work with your current accountant on any strategies.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.