Many clients believe delaying their retirement is a solution to inadequate savings, but they often find themselves out of the workforce sooner than they’d planned. None of us has that crystal ball!

Many clients believe delaying their retirement is a solution to inadequate savings, but they often find themselves out of the workforce sooner than they’d planned. None of us has that crystal ball!

It is likely that the shortfall in retirement savings here in Australia stems in part from our “she’ll be right” attitude towards life, which leads us to believe that we do not need to start saving early and that somehow it will all work out ok.

Delaying retirement can be a powerful boost to your superannuation nest-egg. But relying on the ability to work for a few extra years to stretch retirement savings out a little longer is fraught with risk and does not reflect personal and family health or other issues that may arise. As an example I have had some clients forced to retire to look after their grandchildren due to the illness of the parent.

If you played with any retirement planning calculator or have spoken to an adviser, the “work a little longer” solution would have been investigated and many put it forward as the solution to the GFC “dip” (read plunge) in savings.

The concept is easy to grasp: By working longer then you originally planned, you get more years of concessionally taxed growth in your superannuation accounts especially if you used a Transition to Retirement Pension from 55 or 60. You can also continue to salary sacrifice and make non-concessional contributions while getting the benefit of the Senior And Pensioners Tax Offset (SAPTO) that I mentioned a few weeks ago here.

The idea is the longer you work and save and more you get into a superannuation income stream then your capital will last longer and you may also benefit from more Age Pension when required.

Back to reality with a jolt!

But there is a huge disconnect between workers’ expectations and retirement reality. Over half of the retirees surveyed in a US study last year said they left the workforce earlier than planned, and just 8% of them said that positive factors — such as the ability to afford early retirement — prompted the move. For the vast majority of early retirees, negative circumstances, such as personal or spouse health problems or company downsizing played a role.

40% of Australians will suffer a critical illness before age 65 (Cologne Life Re study). They will most likely survive but their retirement funding will be devastated.

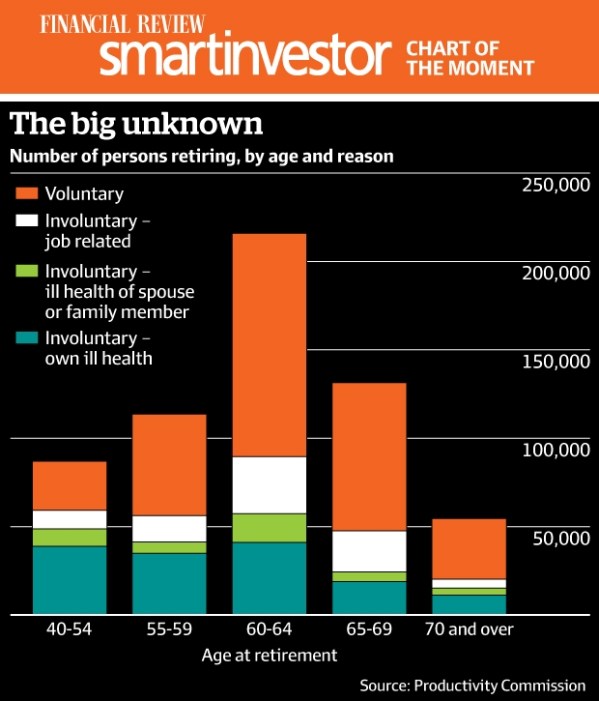

The 2015 Productivity Commission report on post-retirement shows that about 40 per cent of Australians who retire between the age of 60 and 64 do so involuntarily, either because of their own or a family member’s ill health, or redundancy.

For those aged between 65 and 69 who retire involuntarily is not that different, while for younger age groups most people who retire do so involuntarily.

Clearly, workers relying on delayed retirement are rolling the dice. Yet, most people discount the future so much that they’re willing to take that gamble. May hope that an inheritance will save the day but do not realise that age care costs and parents living longer may eat heavily into any expected inheritance.

Strangely the people most likely to plan on working a few more years to boost their retirement security may actually have the least ability to postpone their retirement. People who suffer an illness or injury are more likely than those in good health to have pushed back their expected retirement date in recent years, according to a report from consulting firm Towers Watson. Yet health problems or disabilities were cited by more than half of retirees forced to retire earlier than planned.

Don’t put you head in the sand – start now

As psychologists are quick to point out, we all have that inner voice that loves to procrastinate who loves to put off till tomorrow what we should do today – beause its “all too hard to get your head around”. Saving more today is a sure thing, and extra years in the workforce are anything but. If you know you don’t have enough, you should start saving more today, because that’s by far the less risky alternative.

Let’s look at an example using the Retirement Planner on the MoneySmart.gov.au site for a 55-year-old pre-retiree with just $30K in superannuation. If she earns $80,000, makes $17,500 annual salary sacrifice contributions (in addition to Employers SGC contributions of 9.5%) and earns a 7.5% return pre retirement and 6.5% after, she could be looking at an Income in retirement of $32,143 by age 67 including the Age Pension. If she’s forced to retire at that point, she’s still in better shape than most Australian’s. And if she can continue working, she counld improve on this lifestyle with a better retirement income.

A final don’t is cancelling TPD or Income Protection insurances to save money while in your most productive earning years (read here for more on that subject). The loss of 5-10 years of earnings potential is one guaranteed way to destroy your lifestyle in retirement. Your ability to earn is your biggest asset

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

![]()

![]()

![]()

![]()

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.