⚖️ General Advice Disclaimer This article is general information only and does not constitute personal financial, legal or tax advice. The rules governing SMSFs are complex and individual circumstances vary significantly. You should obtain advice from a licensed financial adviser before acting on anything in this article. The author holds AFSL authorisation through Sonas Wealth Pty Ltd, corporate authorised representative of Viridian Advisory 476223.

Here is a little-known strategy where an SMSF can be involved in owning a business or property through an unrelated unit trust or company structure. This is often ideal for an early-stage business expected to grow rapidly over time where income and growth can be captured tax effectively in the SMSF. Most suited to those who do not need access to the capital and profits until retirement or where you want some in the SMSF and some personally but your shared ownership, between your related parties, does not exceed 50%.

When two unrelated SMSFs co-invest in a trading company, the result can be a genuinely tax-efficient, asset-protected business structure — but it comes with a set of compliance obligations that every trustee needs to understand before proceeding. This guide explains how the structure works, the critical questions to ask, and the key risks to manage. In many cases three unrelated parties can make it a lot less risky in terms of potential SIS law breaches.

The critical first question: is the company a “related party”?

This is the most important compliance question in the entire structure, and the answer determines almost everything else.

Under the SIS Act, a “related party” of your SMSF includes the fund’s members, their relatives, their business partners, and companies or trusts they control. Control means holding the ability to determine more than 50% of the voting rights, or being entitled to more than 50% of dividends or capital. I have a complete article on Related Parties here

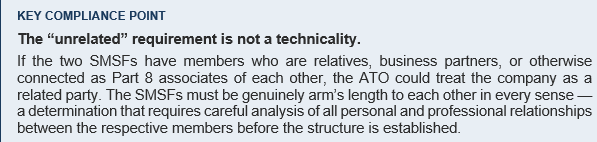

With a genuine 50/50 split between two unrelated SMSFs, neither fund’s members control the company outright. Neither party can determine outcomes alone. Accordingly, the company is generally not a related party of either SMSF — and this single fact unlocks the structure. So you can see that 3 unrelated entities will roughly even ownership would make this safer as less chance of one exceeding 50%.

Thinking About an SMSF — or Want a Second Opinion? If you’d like a no-obligation conversation about whether an SMSF is right for your situation — or you want a straight-talking second opinion on an offer you’ve received — reach out. That’s what The SMSF Coach is here for. http://www.smsfcoach.com.au | Sonas Wealth, Sydney www.sonaswealth.com.au

In-house assets — does the 5% rule apply?

SMSF trustees are familiar with the rule that no more than 5% of a fund’s total assets can be “in-house assets” — generally, investments in or loans to related parties. Because the trading company is not a related party (as established above), the shares your SMSF holds do not count as in-house assets based on the ownership relationship alone.

One important note: Regulation 13.22C provides a separate exclusion from the in-house asset definition for investments in certain closely held entities — but that exclusion is only available if the entity does not conduct a business. Since we are dealing with an actively trading company, Reg 13.22C is irrelevant here. The correct answer is that the company is simply not a related party, so the in-house asset classification does not arise in the first place. Here is a great white paper from Leigh Mansell of Heffron’s on In-house Assets

Tax treatment — where the real advantage lives

This structure can be exceptionally tax-efficient, particularly for SMSF members approaching or in retirement phase.

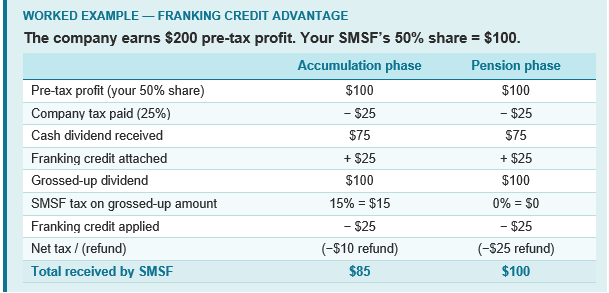

At the company level: A small trading company with turnover below $50 million will typically qualify as a base rate entity and pay company tax at 25%. This tax gives rise to franking credits attached to any dividends paid to shareholders.

At the SMSF level — accumulation phase: Your fund’s effective tax rate on investment income is 15%. When the company pays a franked dividend, the SMSF includes the grossed-up dividend in its assessable income, pays 15% tax, and offsets that liability with the franking credit. Because the company already paid 25% tax, the franking credit typically exceeds the SMSF’s liability — producing a refund.

At the SMSF level — pension phase: If your SMSF is paying pensions and the income qualifies as exempt current pension income, the effective tax rate is 0%. The full franking credit is refunded in cash, making this one of the most tax-efficient investment structures available in Australia.

NALI and arm’s length dealings

Non-arm’s length income (NALI) is taxed in your SMSF at a flat 45%, regardless of whether you are in accumulation or pension phase. Private company dividends are a known NALI risk area, and the ATO scrutinises them carefully.

All dividends must be paid on the same terms to both SMSFs, proportionate to their respective shareholdings, with no preferential treatment flowing to one fund over the other. Arm’s length requirements also apply to any other dealings between your SMSF and the company — including director salaries, lease arrangements, and any services the company provides.

Annual valuation — a compliance obligation you cannot defer

Your SMSF’s financial statements must record all assets at their true market value as at 30 June each year. Shares in a private unlisted trading company must be independently valued by a suitably qualified person using a recognised methodology — typically earnings-based, net tangible assets, or a combination of both. This is not optional; your auditor will require appropriate evidence.

Valuation complexity increases over time, particularly if the company retains significant profits, acquires assets, or if the trading environment changes materially. Factor in the annual cost of a formal valuation — and the management time required to facilitate it — when assessing the overall economics of the structure. My guide to SMSF asset valuations is available here

Before you proceed — a practical checklist

Confirm each of the following before shares are acquired:

Both SMSFs are genuinely unrelated — members are not relatives, business partners, or Part 8 associates of each other in any way

A properly drafted shareholders agreement is executed before shares are acquired

The SMSF investment strategy is updated to specifically contemplate and justify an investment of this type, size, and risk profile

The share acquisition occurs at market value from day one — a below-market acquisition creates permanent NALI taint on all future income from those shares

Dividends will be declared on identical terms for both SMSFs from the outset

An annual independent valuation process is established and budgeted for

The company has a separate ABN, ACN, and bank account entirely independent of any member’s personal finances

Any member who is also a director or employee of the company is remunerated at genuine market rates

Legal advice has been obtained on both the company establishment and the SMSF’s acquisition of shares

Your SMSF auditor has been informed of the investment and understands the basis on which it is not classified as an in-house asset

Always make sure that you’re your strategy complies with relevant superannuation and tax regulations before implementation

Are you looking for advisors that will keep you up to date and provide guidance and tips like in this blog? then why not contact us at our Castle Hill or Windsor office in North West Sydney to arrange a one-on-one consultation, just click the Schedule Now button up on the left to find the appointment options.

Please consider passing on this article to family or friends. Pay it forward!

Corporate Authorised Representative of Viridian Advisory Pty Ltd ABN 34 605 438 042, AFSL 476223

Important information

This article is general information only and does not constitute personal financial, legal, or taxation advice. The rules governing self-managed superannuation funds are complex and fact-specific. Individual circumstances vary significantly, and the application of the rules described in this guide depends on facts that can only be properly assessed by a qualified professional. Before establishing or participating in a structure of this type, seek advice from a licensed SMSF adviser and an experienced tax lawyer. Past tax outcomes are not a guide to future tax treatment.

We have only a short time left to the end of the 2026 financial year to get our SMSF in order and ensure we are making the most of the strategies available to us. Here is a checklist of the most important issues that you should address with your advisers before the year-end.

Get this wrong and your SMSF could lose tax exemptions, trigger penalties, or lock in avoidable tax

It’s been another busy year and I have not had as much time to put this together so if you find an error or have a strategy to add then please let me know. Links were working at the time of writing.

Warnings before we begin:

Know your Own Data: You need to check your personal super balances across all your accounts, contribution limits, total Super Balance and Transfer Balance caps and tax position before implementing any of these strategies as your own particular circumstances may warrant alternative options.

Confirm your annual return lodgement status: Log in to ATO online services and confirm your most recent SMSF annual return for 2025FY has been lodged and shows as processed (near the deadline now). As of December 2025, approximately 93,000 funds had one or more overdue returns. A fund with an overdue return faces penalties, potential interest charges, and likely removal from the Super Fund Lookup register. This can interrupt employer contributions and serious consequences under Pay Day Super requirements for your employer .

High-impact strategies most people miss out without advice

Recontribution strategy for minimising death taxes

Pension vs lump sum strategy

Spouse equalisation for Division 296

Look out for more detail on these as you go through the checklist

The Checklist

1. It’s all about timingwith contributions

If you are making a contribution, the funds must hit the super fund’s bank account by the close of business on 30 June. Some clearing houses hold on to money for up to 14 days before presenting them to the super fund. Some Retail and Industry funds are asking for funds at least to be contributed by the 18th-19th June!

In addition, pension payments must leave the account by the close of business unless paid by cheque in which case the cheques must be presented within a few days of the EOFY. There must have been sufficient funds in the bank account to support the payment of the cheques on 30 June but a cheque should only be your very last-minute option! You can also ask your adviser or administrator about a Promissory Note if time is against you but funds are ready.

So, for SMSFs get your payments in the fund by Monday 22nd June or earlier to be sure (yes I’m Irish) as the 30th is a Tuesday this year. This is even more important if using a clearing house for contributions.

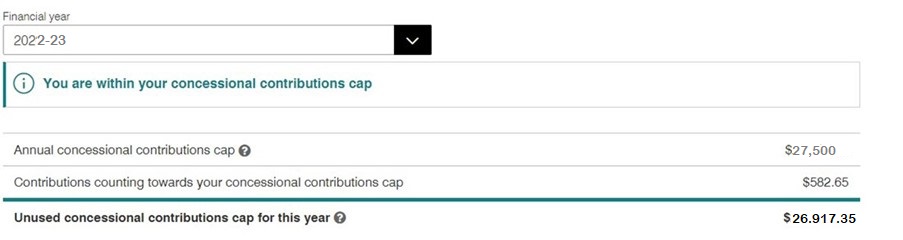

2. Review your Concessional Contributions (CC) options including Unused Carry Forward Limits

The 2025–26 concessional cap is $30,000. This includes all employer contributions, salary sacrifice, and any personal deductible contributions. Log in to ATO online services via myGov and confirm your year-to-date total before making any further contributions.

And remember that you have the ability to make concessional contributions up to age 67 even if not working and to 75 if you meet the Work Test . This is important for those who have retired but may have sold a property or shares and triggered a large capital gain during the year. Do not not exceed your limit unless you have Unused Carried Forward Concessional limits and Total Super Balance under $500K as of last 01 July 2025.

This current 5 year period for Unused Concessional Contributions applies from 2020-21 so effectively, this means an individual can make up to $172,500 of CCs in a single financial year by utilising unapplied unused CC caps since 1 July 2019 and this years limit. Guidance on how to check your Unused Carried Forward Concessional limits via MyGov records available here. ..

This is the last year to use the 2020-21 unused Carried Forward Concessional Caps as they fall outside the 5 year rolling period from 30 June 2026.

Beware that once your Income including Salary, Investment income, Employer SGC, Personal Concessional Contributions goes over $250,000 you will be subject to Div 293 Tax

TIP: The Super Guarantee now remains at 12% but the Concessional limit will rise to $32,500 from 1 July 2026. Re-evaluate your contribution plans for 2026-27

3. Review plans for Non-Concessional Contributions (NCC) options

The 2025–26 non-concessional cap is $120,000. You can only make non-concessional contributions if your Total Super Balance was below $2.0 million at 30 June 2025.

From 1 July 2022 the NCC contribution rules changed and currently the age limit of 75 (28 days after the end of the month your turn 75) applies to NCCs (that is, from after-tax money) without meeting the work test. Check out ATO superannuation contribution guidance.

NCCs are an opportunity to move investments into super and out of a personal, company or trust names.

For those couples where one has a higher balance that may be affected by the proposed Division 296 Tax, it is important to review you option to even-up spouse balances and maximise super in pension phase up to age 75. For couples where one spouse has exhausted their transfer balance cap and has excess amounts in accumulation or above $3m or even the $10m threshold, they are able to withdraw from the higher balance and recontribute to the other spouse who has transfer balance cap space available to commence a retirement phase income stream. This can increase the tax efficiency of the couple’s retirement assets as more of their savings are in the tax-free pension phase environment and may help minimise Div 296 Tax.

TIP 1: If you have considerable additional funds to add to contribution then maybe contribute up to $120,000 before June 30 and then you may be able to contribute up to $390,000 after 1 July to maximise contributions.

TIP 2:From 1 July 2026 the Non-Concessional Cap will rise to $130,000 per year or $390,000 under the 3 Year Bring Forward Rule.

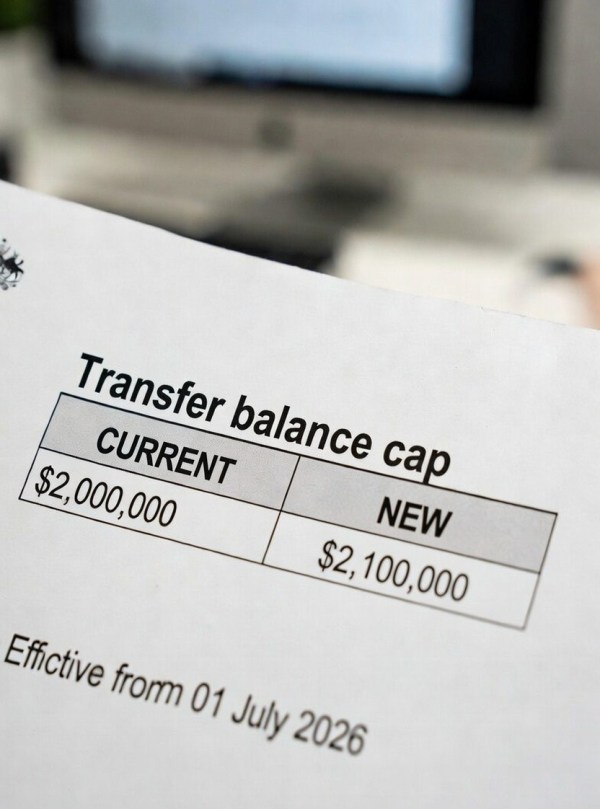

4. Recontribution Strategies

Consider doing the drawdown before 30 June 2026 so that your Transfer Balance Cap and Total Super Balance on 1 July 2026 gets some additional space with the rise in the TBC and TSB full limits to $2.1m. Note that if you had and existing pension(s) at 30 June 2025 your current TBC limit will be anywhere between $1.6m and $2.1m after 1 July (Frustrating for Advisers! so help by providing them your My Gov Super records)

You can also make your tax components more tax free by using recontribution strategies. SMSF members can cash out their existing super and re-contribute (subject to their contribution caps) them back in to the fund to help reduce tax payable from any super death benefits left to non-tax dependants. From 1 July 2022 you can do this until they turn age 75 (contribution to be made with 28 days after the end of the month you turn 75).

5. Downsizer contributions

If you have sold your home in the last year and you are over 55, consider eligibility for downsizer contributions of up to $300,000 for each member.

From 1 jan 2023, the eligibility age to make downsizer contributions into superannuation was reduced from 60 to 55 years of age. All other eligibility criteria remain unchanged, allowing individuals to make a one-off, post-tax contribution to their superannuation of up to $300,000 per person from the proceeds of selling their home. These contributions will continue not to count towards non-concessional contribution caps.

The $300,000 downsizer limit (or $600,000 for a couple) and the $360,000 bring forward NCC cap allow up to $660,000 in one year contributions for a single person and $1,320,000 for a couple subject to their contributions caps.

PLEASE BE CAREFUL AS THE DOWNSIZER IS A ONCE ONLY STRATEGY AND IF YOU WOULD BENEFIT MORE IN OLDER YEARS USING THE STRATEGY THEN MAXIMISE NCCs FIRST.

6. Calculate co-contributions

Check your eligibility for the co-contribution, it’s a good way to boost your super. The amounts differ based on your income and personal super contributions, so use the super co-contribution calculator. Is your spouse on maternity or paternity leave? See if they could benefit from this strategy to keep their balance growing. If you have moved to part-time work, this may boost your super.

7. Examine spouse contributions

If your spouse has assessable income plus reportable fringe benefits totalling less than $37,000 for the full $540 tax offset or up to $40,000 for a partial offset, then consider making a spouse contribution. Check out the ATO guidance here.

You can implement this strategy up to age 75 as a Spouse Contribution is treated as a NCC in their account (and therefore counted towards your spouse’s NCC cap).

8. Give notice of intent to claim a deduction for contributions first

A notice must be made before you commence a pension or split to a spouse. Many people like to start pension in June and avoid having to take a minimum pension in that financial year but make sure you have claimed your tax deduction first. The same notice requirement applies if you plan to take a lump sum withdrawal from your fund.

9. Consider contributions splitting to your spouse

Consider splitting contributions with your spouse, especially if:

your family has one main income earner with a substantially higher balance or

if there is an age difference where you can get funds into pension phase earlier or

if you can improve your eligibility for concession cards or age pension by retaining funds in superannuation in the younger spouse’s name.

This is a simple no-cost strategy I recommend for everyone here.

Remember, any spouse contribution is counted towards your spouse’s NCC cap.

10. Act early on off-market share transfers

If you want to move any personal shareholdings ETFs. or Managed Funds into super (as a contribution) you should act early. The contract is only valid once the broker or fund manager receives a fully-valid Off Market Transfer form so timing in June is critical. There are likely to be brokerage costs involved. Some fund managers only price weekly/monthly/quarterly so check first. For unlisted managed funds you will also need a new Account Application with the Off Market Transfer form.

11. Review options on pension payments

Ensure you take the standard minimum pension at your age-based rate. If a pension member has already taken pension payments of equal to or greater than the the minimum amount, they are not required to take any further pension payments before 30 June 2025. For transition to retirement pensions, ensure you have not taken more than 10% of your opening account balance this financial year.

Minimum annual payments for pensions.

Age at 1 July

2025FY – Standard Minimum % withdrawal

Under 65

4%

65–74

5%

75–79

6%

80–84

7%

85–89

9%

90–94

11%

95 or older

14%

If a pension member has already taken a minimum pension for the year, they cannot change the payment but they can get organised for 2026/27. No, you can’t sneak a payment back into the SMSF bank account unless you treat to as a new contribution!

If you need more than the minimum pension payments for living expenses then it may be a good strategy for amounts above the minimum to be treated as either:

a partial lump commutation sum rather than as a pension payment. This would create a debit against the pension member’s Transfer Balance Account (TBA). Please discuss this with your accountant and adviser first as all funds now have to report these quarterly to the ATO.

for those with both pension and accumulation accounts, take the excess as a lump sum from the accumulation account to preserve as much in tax-exempt pension phase as possible.

Failure to pay minimum pensions just got a lot more costly

SMSF trustees, accountants and financial advisers should take note of significant changes to pension commencement rules that came into effect on 1 July 2025. These changes impact how pensions are treated for tax purposes if a minimum pension is missed and could have serious implications for retirement planning strategies. Read more detail here

12. Check your documents on reversionary pensions

A reversionary pension to your spouse will provide them with up to 12 months to get their financial affairs organised before making a final decision on how to manage your death benefit. In NSW this may avoid issues with Binding Death Nominations and the Notional Estate (see Benz v Armstrong; Benz v Armstrong; Benz v Armstrong – 2022 NSWSC)

You should review your pension documentation and check if you have nominated a reversionary pension in the context of your family situation. This is especially important with blended families and children from previous marriages that may contest your current spouse’s rights to your assets. Also consider reversionary pensions for dependent disabled children.

The reversionary pension has become more important with the application of the $1.6-$2.1m million Transfer Balance Cap (TBC) limit to pension phase.

Tip:If you have opted for a nomination instead then check the existing Binding Death Benefit Nominations (many expire after 3 years in older deeds) and look to upgrade to a Non-Lapsing Binding Death Benefit Nomination. Check your Deed allows for this first.

Tip 2: Under Division 296Tax, the Reversionary Beneficiary’s Total Super Balance (TSB) increases immediately, potentially triggering a 15% tax if their TSB exceeds $3 million or up to 25% if above $10m at financial year-end. Beneficiaries must weigh the cost of this new tax against the benefits of tax-exempt pension income, while noting that converting to a non-reversionary pension requires careful review of the specific SMSF deed. Ultimately, this decision depends on the Reversionary Beneficiary’s individual financial position and broader estate planning goals.

13. Review Capital Gains Tax on each investment (For every one)

Review any capital gains made during the year and over the term you have held the asset and consider disposing of investments with unrealised losses to offset the gains made. If in pension phase, then consider triggering some capital gains regularly to avoid building up an unrealised gain that may be at risk to legislation changes.

Consider the Division 296 CGT cost base election for 30 June 2026

For SMSF trustees, the election to reset the cost base of assets to their 30 June 2026 market value is a critical one-time opportunity to shield pre-existing capital gains from the Division 296 tax.

Key Planning Considerations

“All-or-Nothing” Election:

The choice applies to every capital gains tax (CGT) asset held by the fund on 30 June 2026.

Trustees cannot pick and choose; they must reset all assets or none.

Irrevocability and Purpose:

The election is irrevocable once made.

This reset applies exclusively for Division 296 purposes. The fund’s standard CGT and income tax calculations still use the original acquisition cost.

Impact of Unrealised Losses:

If an asset’s market value on 30 June 2026 is lower than its original cost, resetting will lock in a lower cost base for Division 296 purposes.

This could result in a larger Division 296 capital gain in the future if the asset recovers and is later sold.

Read more about this option on our LinkedIn post here

14. Collate records of all asset movements and decisions

Ensure all the fund’s activities have been appropriately documented with minutes, and that all copies of all statements, valuations and schedules are on file for your accountant, administrator and auditor.

The ATO has now beefed up its requirements for what needs to be detailed in the SMSF Investment Strategy so review your investment strategy and ensure all investments have been made in accordance with it and the SMSF Trust Deed, including insurances for members. See my article on this subject here.

15. Arrange market valuations (beware of the proposed Div 296 Tax Sting)

Regulations now require assets to be valued at market value each year, including property and collectibles. For more information refer to ATO’s publication Valuation guidelines for SMSFs.

On collectibles, play by the new rules that came into place on 1 July 2016 or remove collectibles from your SMSF.

Tip:The ATO is targeting audit compliance this year on Property Valuations in SMSFs as we approach the implementation of the proposed Division 296 Tax from 1 July 2026.

Tip 2: It would be better to ensure your properties truly match the market value on 1 July 2026 than to have a large rise in value recorded in future years that will trigger higher Div 296 Tax.

Tip 3:Do a 3 year deal with your Valuer!! SMSF Auditors generally accept a full, independent property valuation every three years, provided that in the intervening years you can supply objective and supportable evidence to demonstrate that the property is still recorded at market value.

This evidence must be supplied to the auditor annually and can include:

Title Searches: An annual title search indicating no new charges or liens on the property

Comparable Sales: Evidence of recent sales for similar properties in the same area.

Independent Appraisals: A “kerbside” appraisal or market appraisal from a licensed real estate agent.

Rate Notices: Council or water rates notices (if consistent with other evidence).

Rental Statements: Agent reports showing rental income for the year, which can be used to justify market value through a rental yield analysis.

16. Check the ownership of all investments.

Make sure the assets of the fund are held in the name of the trustees (including a corporate trustee) on behalf of the fund. Carefully check any online accounts and ensure all SMSF assets are separate from your other assets.

We recommend a corporate trustee to all clients. This might be a good time to change, as explained in this article on Why SMSFs should have a corporate trustee. If you have previously moved to a Corporate Trustee then double check all accounts/investments were changed to the name of this trustee.

17. Review Estate Planning and loss of mental capacity strategies

Review any Binding Death Benefit Nominations (BDBN) to ensure they are valid, consider Non-Lapsing Nominations and check the wording matches that required by the Trust Deed. Ensure it still accords with your wishes.

Also ensure you have appropriate Enduring Powers of Attorney (EPOA) in place to allow someone to step into your place as trustee in the event of illness, mental incapacity or death. Ensure that your Power of Attorney is valid for the state you are in living in now if you have retired interstate. This article explains how it can all go wrong

Tip: Check your Trust Deed and the details of the rules. For example, did you know you cannot leave money to stepchildren via a BDBN if their birth-parent has pre-deceased you?

18. Review any SMSF loan arrangements

Have you provided special terms (low or no interest rates, capitalisation of interest etc) on a related party loan? Review your loan agreement and see if you need to amend your loan.

Have you made all the payments on your internal or third-party loans, have you looked at options on prepaying interest or fixing the rates while low?

Have you made sure all payments in regards to Limited Recourse Borrowing Arrangements (LRBA) for the year were made through the SMSF trustee? If you bought a property using borrowing, has the Holding Trust been stamped by your state’s Office of State Revenue? For Related Party LRBA’s the Variable interest rate is currently 8.95% (will be updated for 2027FY in late May)

19. Ensure SuperStream obligations are metand be ready for PayDay Super from 1 July 2026

For super funds that receive employer contributions, the ATO is now enforcing the use of SuperStream, a system whereby super contributions data is made electronically and from 1 July 2026 the Pay Day Super legislation will apply

Payday Super affects SMSFs as well. Is your SMSF Bank account NPP Enabled? Read more here

All funds should be able to receive the contributions same day using NPP and data electronically and you should obtain an Electronic Service Address (ESA) to receive contribution information.

If you change jobs your new employers may ask SMSF members for their ESA, ABN and bank account details.

20. Ensure you are meeting your Quarterly TBAR Reporting deadlines

IF you are in Pension Phase then you need to be checking in with your accountant/administrator Quarterly to ensure TBAR reporting is up to date.

All SMSFs are required to report quarterly. This means you must report the event that affects the members transfer balance within 28 days after the end of the quarter in which the event occurs.

Example: All unreported events that occurred between 1 April and 30 June 2026 must be reported by 28 October 2026. This means you cannot report at the same time as your SMSF annual return (SAR) for the 2023-24 income year. More info here

21. ASIC fee increased from 1 July 2026 and how to avoid the sting with a discount

ASIC is increasing fees by $2 for the annual review of a special purpose SMSF trustee company $65 to $67. The Government is moving gradually to a “user pays” model so expect increases to accelerate in future years. Before 30 June, for $457 you can pre-pay the company fees for 10 years and lock in current prices with a decent discount. There is a remittance form linked here.

Why would you do this? – THE PENALTIES IF YOU MISS RENEWAL!!!

On 6 December 2024, regulations were released to allow the commutation of legacy pensions for a limited 5-year period. There is considerable additional detail in this feature so consult an adviser if you are affected, especially to ensure you do not lose other entitlements such as the age pension.

The regulations allow a five-year timeframe for lifetime or life expectancy pensions and MLIS to be commuted.

You have the following options:

▪ withdraw the funds from superannuation (all these clients have previously met a condition of release) ▪ rollover the amount to accumulation phase, or

▪ use the funds to commence an account based pension (if transfer balance cap space is available).

Under this measure, if a lifetime or life expectancy pension is commuted, any reserve supporting that income stream is also added to the commutation value. However, no amount from the reserve is counted tow

OTHER ISSUES

23. HAS NOT PASSED: Relaxing residency requirements for SMSFs– Labor Government has failed to move on this issue.It appears lost in the ether!

SMSFs and small APRA funds still do not have relaxed residency requirements through the extension of the central management and control test safe harbour from two to five years as the LNP government failed to pass it before the last election and Labor have put it on the backburner. The active member test was also to be removed, allowing members who are temporarily absent to continue to contribute to their SMSF. So if you are heading overseas on an extended secondment or to live please review your options and here is a great guide to your options

24. Improved the Home Equity Access Scheme – Highlighting Social security benefits for you or your parents

Is your SMSF / Super balance getting low and you want to preserve as much as you can for later in your life?

The Home Equity Access Scheme formerly called The Pension Loan Scheme is now up and running. The Government introduced a No Negative Equity Guarantee for HEAS loans and allow people access to a capped advance lump sum payment.

No negative equity guarantee – Borrowers under the HEAS, or their estate, will not owe more than the market value of their property, in the rare circumstances where their accrued HEAS debt exceeds their property value. This brings the HEAS in line with private sector reverse mortgages.

Immediate access to lump sums under the HEAS – Eligible people will be able to access up to two lump sum advances in any 12-month period, up to a total value of 50% of the maximum annual rate of Age Pension Current Maximums (effective 20 March 2026):

Singles: $15,611.70 (based on a maximum annual pension rate of approximately $31,223.40).

Couples (Combined): $23,535.20 (based on a maximum annual pension rate of approximately $47,070.40).

25. Careful if replacing Income Protection or TPD Insurance (Total Permanent Disability)

Have you reviewed your insurances inside and outside of super? Don’t forget to check your current TPD policies owned by the fund with an own occupation definition as the rules changed a few years ago. So be careful about replacing an existing policy as you may not be able to obtain this same cover inside super again.

There were major changes to Income Protection insurance in 2021 so be very careful about switching insurer unless costs have blown out as new cover is often vastly inferior to current covers. Read more here before switching cover.

26. Large one-off Personal income or gain – Bring forward Concessional Contributions

For those who may have a large taxable income this year (large bonus or property sale) and are expecting a lower taxable next year you should consider a contribution allocation strategy to maximise deductions for the current financial year by bringing some or all of your 2026FY limit forward to this year. This strategy is also known as a “Contributions Reserving” strategy but the ATO are not fans of Reserves so best to avoid that wording! Just call is an Allocated Contributions Holding Account. See my article on this strategy here.

27. Providing Proof of Crypto Currency Holdings as of 30 Juneand now Exchanges must have AFSL

As of April 2026, cryptocurrency exchanges and custody platforms in Australia that meet specific asset thresholds are required to hold an Australian Financial Services Licence (AFSL) within 12 months. You should be using an exchange that is set up for SMSF accounts. They should provide a Tax Summary but it may cost extra. Some exchanges are now partnering with Specialised services that are experts in Australian to offer tax reports that meet Australian Audit requirements.

The auditor will also want to verify holdings by checking:

An exchange account is set up in the name of the fund

Wallet purchased using funds from the SMSFs cash account

Cold Wallet Audit management extra step: For annual audit purposes, take a screenshot of the assets held in your Ledger wallet (e.g. via the Ledger ‘Live’ App or similar) on 30 June 2025 and also on the day you submit your paperwork and email this to the tax agent at tax time.

29. NALE/NALI applies in the 2026FY (in the sense the ATO are going to enforce it) – please ensure that if members perform services for their SMSF which is their ‘day job’ (ie. Accounting work for Accountants, Building and repair work for tradies, etc) that these are charged at the appropriate commercial rate that they charge their clients. A good article explaining this in more detail here from ASF Audits

Don’t leave it until after 30 June, review your Self Managed Super Fund now and seek advice if in doubt about any matter.

Some ideas for 1 July 2026

28. Check your Salary Sacrifice or Personal Contributions as Concessional Cap rises to $32,500 and Non-Concessional Cap to $130,000

The superannuation guarantee (SG) rate will remain the same but the Concessional Cap will rise from $30,000 to $32,500. You’ll need to use the new rate to calculate how much of your $30,000 concessional cap will be available to salary sacrifice or make personal deductible contributions.

The annual non-concessional contribution (NCC) cap is set to rise to $130,000 (up from $120,000 in 2025–26) due to indexation. The three-year bring-forward cap will consequently increase to $390,000, allowing higher after-tax contributions depending on total super balance

29. Check your SMSF Trust Deed is current

If your SMSF’s trust deed was last updated before 2015, it may not support current pension strategies, contribution rules, or binding death benefit nomination formats. Legislative changes since then mean older deeds can inadvertently restrict what your fund can legally do. Consider an update every 3-5 years.

30. Check your Investment Strategy is ready for Audit and 2027FY

As mentioned earlier The ATO has now beefed up its requirements for what needs to be detailed in the SMSF Investment Strategy so review your investment strategy and ensure all investments have been made in accordance with it and the SMSF Trust Deed, including insurances for members. See my article on this subject here.

Warning: Don’t jump into the implementation of any strategy without checking your personal circumstances first.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact our team at our Castle Hill or Windsor office in Northwest Sydney to arrange a one-on-one consultation, just click the Schedule Now button up on the left to find the appointment options.

Please consider passing on this article to family or friends. Pay it forward!

Oh and please leave a comment or a “like” so I don’t feel I am talking in a vacuum!

Corporate Authorised Representative of Viridian Advisory Pty Ltd ABN 34 605 438 042, AFSL 476223

This information has been prepared without taking into account your objectives, financial situation, or needs. Because of this, you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation, and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

⚖️ General Advice Disclaimer This article is general information only and does not constitute personal financial, legal or tax advice. The rules governing SMSFs are complex and individual circumstances vary significantly. You should obtain advice from a licensed financial adviser before acting on anything in this article. The author holds AFSL authorisation through Sonas Wealth Pty Ltd, corporate authorised representative of Viridian Advisory 476223.

Hi, I’m Liam Shorte — better known as The SMSF Coach. As a Financial Planner and SMSF Specialist Advisor with over two decades helping families take control of their super, I’ve seen it all. We often see people, who jumped in to an SMSF before really understanding how it works and it can be a time consuming and an expensive mistake to unwind.

Introduction

An SMSF can be one of the most powerful retirement structures available to Australians — but it is not the right choice for everyone. With over 661,000 SMSFs now operating across Australia and record numbers being established each quarter, I want to make sure that enthusiasm doesn’t outpace understanding.

Before we help anyone establish a fund at Sonas Wealth, we work through a rigorous set of questions together. Some people come in certain an SMSF is what they need. Some leave the conversation feeling the same way. Others discover a better path. Either outcome is a good one — because the goal is never to set up a fund. The goal is to protect and grow your retirement.

This is always the first question. Setting up an SMSF because you’ve heard it’s a good idea, or because a colleague mentioned it over coffee, is not a strategy. I want to understand your short, medium and long-term goals — and whether an SMSF is genuinely the best vehicle to get you there.

Sometimes the answer is clearly yes. Often it opens a broader conversation about alternatives that may serve your true objectives just as well, or better. I’ll never hesitate to point you toward a different path. An SMSF is not the right answer for everyone, and I don’t believe in setting one up just because we can.

2. Is Locking Money Away the Right Move Right Now?

Superannuation is long-term money. For most people, it cannot be accessed until their preservation age — typically 60 — when they meet a condition of release. Before directing more wealth into super, we need to look honestly at your current financial commitments and what flexibility you might need in the next decade.

In many cases, redirecting surplus funds into debt reduction, a personal investment portfolio, or an insurance bond for tax-effective investing can deliver better outcomes while preserving access to capital. Super is a powerful tool — but it needs to be the right tool for the right job at the right time in your life.

💡 Worth Knowing: Carry-Forward Contributions

If your total super balance (TSB) is below $500,000, you may be eligible to use carry-forward concessional contributions — sweeping up unused cap room from the previous five financial years into a single large pre-tax contribution. This can be a powerful complement to an SMSF strategy, particularly when triggered by a significant asset sale or inheritance. Ask your adviser whether this applies to you before deciding how much to contribute and when.

3. Do You Have the Time, Knowledge and Discipline to Run a Fund?

This is the question that surprises people most. Running an SMSF is not passive. It requires you to understand your trustee obligations, review your investment strategy regularly, stay across legislative changes, and commit genuine time to governance — every year, not just at setup.

📖 From the Coaching Files

I’ve had to talk a number of busy executives and business owners out of SMSFs when they couldn’t find a single hour in their week for a meeting — yet expected to manage an $800,000 investment portfolio. I’ve also worked with a couple who considered themselves property experts because they owned four regional Queensland properties, none of which they had ever visited. When we analysed the numbers, the yields were poor, capital growth was flat, and deferred maintenance costs were substantial. Their existing diversified super fund was objectively the safer option until they genuinely developed their property knowledge.

4. What Do You Have to Roll Over — and Can You Actually Move It?

Not all superannuation balances can be rolled into an SMSF without careful consideration. Before making any decision, we need to confirm:

Access restrictions — Some government, military or defined benefit funds (MSBS, Local Government Super) cannot be accessed before a specific age or in certain circumstances.

Defined benefit value — In some cases, the guaranteed benefit from a defined benefit scheme is simply too valuable to walk away from. The certainty of income in retirement may outweigh the flexibility of an SMSF.

Exit costs and liquidity — High exit fees or illiquid underlying investments can make an immediate rollover costly.

Employer mandated funds — Some enterprise bargaining agreements require contributions to flow to a specific fund, which may limit your ability to redirect future Super Guarantee payments. Also some employers offer 1%+ extra to employees using their default fund…don’t lose out!

We work through exactly what you hold, what’s moveable, and what the true cost of moving is — before any action is taken.

5. Have Your Insurance Needs Been Properly Addressed?

Insurance inside superannuation is one of the most commonly overlooked elements of an SMSF transition. When you leave an APRA-regulated industry or retail fund, you typically lose group insurance cover — often cover that would be difficult or impossible to replace on the open market due to health changes since you first obtained it.

⚠️ Critical: Insurance Lost on Rollover Cannot Always Be Reinstated

Once you roll out of an industry or retail fund, group life, TPD and income protection cover is typically cancelled and cannot be reinstated. If your health has changed since that cover was granted, you may find individual cover is either unavailable or prohibitively expensive. Get a full needs analysis before you move a single dollar. Your SMSF trust deed must also document that insurance needs have been considered — it is a compliance requirement, not optional.

6. Are You Genuinely Clear on Your Trustee Responsibilities?

When you sign the Trustee Declaration, you are making a legal commitment that you understand the obligations of a trustee under superannuation law. Saying you didn’t understand those obligations after a compliance breach is not a defence.

As a trustee you are personally responsible for every compliance decision, every investment decision, all record-keeping obligations, and every reporting requirement the fund faces — even if you outsource administration to a professional. We will make sure you have a solid knowledge base before you commit. Your urgency to establish a fund doesn’t override our duty of care to you.

Fixed costs don’t scale down with a smaller balance. The maths needs to work in your favour before an SMSF makes financial sense compared to the APRA-regulated fund you’re currently in.

Cost Component

Typical Range (2025–26)

Setup costs (establishment + trust deed)

$1,500 – $3,000

Annual running costs

$2,000 – $5,000+ (You can find lower at a trade off)

Annual independent audit

$400 – $800

ATO supervisory levy

$259 per year

ASIC annual review fee – sole purpose trustee co.

$67 (look at paying 10 years upfront)

Fund Balance

Annual Cost ($3,500)

Effective Fee Rate

$150,000

$3,500

2.3% — hard to overcome

$200,000

$3,500

1.75% — borderline

$300,000

$3,500

1.1% — becoming viable

$500,000+

$3,500

0.7% or less — cost effective

You can run your SMSF for lower with some online providers but beware of limitations or deals with related parties where they get a cut of brokerage or mortgage commission or straight our referral fees that you ultimately pay.

$200,000–$250,000 in combined member balances is the minimum we normally use.

8. Do You Understand the Risks — Not Just the Benefits?

SMSFs offer genuine advantages: investment control, tax flexibility, estate planning sophistication, and the ability to hold assets such as direct property and business real property. These are real, and for the right person at the right balance, they are compelling.

✅ Potential Benefits

⚠️ Key Risks to Manage

Engagement: we find people who take an active interest in their super are more likely to contribute more, invest consistently and therefore benefit from compound growth

Not understanding how the SMSF works or losing interest.

Full control over investment decisions

Personal trustee liability for all compliance failures. Could mean you can no longer be a director of your own business!

Access to direct property, unlisted assets and collectibles

Concentration risk — especially in property-heavy funds

Economies of scale investing as a couple or family and one SMSF set of fees rather than paying for multiple accounts.

Disagreements on how fund should be managed like different risk tolerances or something more serious like divorce

Tax planning flexibility (timing of contributions and capital gains). Not having to move accounts when changing from accumulation to pension.

Liquidity problems in retirement if assets are illiquid

Superior estate planning via binding death benefit nominations

ATO audit risk if governance is poor

Business real property can be held and leased to related parties

Poor diversification if trustees lack investment expertise

Tax-free income in pension phase on eligible assets

Fines up to $18,000 per trustee for serious breaches

Agility and Transparency: Members have full transparency over their investments, fees, and tax positions. The fund can also react quickly to market changes or legislative updates.

Indecision – being reluctant or afraid to press “Buy” or more often reluctance to admit a wrong call and “Sell”

We’ll give you a balanced view, not a sales pitch in either direction. No reasonable investment reliably produces excessive returns over the long term — and any adviser suggesting otherwise should be a red flag.

9. Have You Thought Carefully About Your Investment Strategy?

Your investment strategy is not a formality — it is a legally required, living document that must genuinely reflect your objectives, risk tolerance, diversification approach, liquidity needs, and the insurance requirements of all members. The ATO expects it to guide every investment decision and to be reviewed regularly, particularly when member circumstances change.

A strategy that says “we will invest in whatever we feel like” is not compliant. We help you build something grounded in realistic expectations and genuine retirement planning — not just a document to tick a box.

10. If Borrowing Is Part of the Plan, Is It Genuinely Affordable?

Limited Recourse Borrowing Arrangements (LRBAs) can be a legitimate strategy inside an SMSF, particularly for acquiring commercial or business real property. But they add significant complexity, increase risk, and must be structured correctly from day one — a defect in the LRBA structure can invalidate the arrangement and create a compliance breach.

Before proceeding with any gearing strategy, we assess:

Whether borrowing is genuinely appropriate for your circumstances and risk profile

Whether the loan is serviceable from the fund’s income and contributions, without relying on member contributions to cover shortfalls indefinitely

Whether the long-term retirement outcome is improved — not just the short-term tax position

Whether the trust deed and LRBA documentation are correctly structured

We’ll walk you through the rules, the process, and the most common mistakes to avoid before you commit to anything.

In fact we have an Education section just on Property in an SMSF with over 17 articles to guide you on every aspect of the strategy. WE DO NOT SELL PROPERTY BUT WE DO CATER FOR YOUR INVESTMENT PREFERENCES

11. What Happens If Circumstances Change?

Life doesn’t stay still. Divorce, death, disability, loss of income, or a decision to move overseas can all complicate an SMSF significantly — and if you haven’t planned for these contingencies from the beginning, unravelling them can be expensive and stressful.

Death benefit nominations — Binding nominations direct the trustee how to distribute your super on death. Not all trust deeds allow binding nominations; check yours. Non-lapsing nominations provide greater certainty.

Incapacity — If a trustee loses capacity, the fund may be unable to operate without an enduring power of attorney in place. This is a commonly overlooked risk.

Relationship breakdown — Super splitting orders following a divorce can create significant complexity in an SMSF, particularly where illiquid assets are involved.

Moving overseas permanently — If all members relocate offshore, the fund may fail the Australian residency test and lose its concessional tax status. Seek advice well before any long-term departure.

Winding up — Once a fund is wound up, it cannot be reactivated. Ensure you have a clear exit strategy and understand the process before you need it. We have you covered How to Wind Up Your SMSF

My View as The SMSF Coach

I’ve spent my career helping trustees get more from their SMSF — but I’ve also spent a lot of time talking people out of one when the timing, balance, or circumstances weren’t right. Both conversations matter equally.

The SMSF sector is growing rapidly — over 661,000 funds, more than 1.2 million members, and record establishment numbers in recent quarters. Some of that growth reflects genuinely well-considered decisions by people who understand what they’re taking on. Some of it reflects enthusiasm running ahead of understanding.

An SMSF done well can be one of the most effective long-term wealth structures available to an Australian. An SMSF done poorly — or set up for the wrong reasons at the wrong time — can quietly erode the retirement security it was meant to protect. My job is to make sure you know which one you’re looking at before you commit.

If you’ve read this and still think an SMSF might be right for you, let’s have that conversation properly.

Pre-Decision Checklist

Before committing to establishing an SMSF, work through each of the following with your adviser:

#

Checklist Item

✅

1

Your goals and objectives genuinely align with what an SMSF can deliver

☐

2

Locking money in super is the right move given your current financial position and commitments

☐

3

You have the time, knowledge and discipline to fulfil trustee obligations year-on-year

☐

4

Your current fund balances can be rolled over — access restrictions and exit costs confirmed

☐

5

Your current fund balances can be rolled over — access restrictions and exit costs confirmed

☐

6

A full insurance needs analysis has been completed before any rollover

☐

7

You have read the Trustee Declaration and understand your legal obligations

☐

8

The cost-benefit analysis confirms an SMSF is cost-effective compared to your current fund

☐

9

You understand both the benefits AND the risks, including compliance penalties

☐

10

A compliant, meaningful investment strategy has been drafted and reviewed

☐

11

If borrowing is planned — LRBA affordability, structure and documentation confirmed

☐

12

Death benefit nominations, power of attorney and exit strategy have been considered

☐

13

Corporate trustee vs individual trustee decision made and reasons documented

☐

📌 Key Takeaways

✅ An SMSF can be a powerful retirement structure — but only when established for the right reasons, at the right balance, and by trustees who understand the obligations.

💰 The cost-effectiveness threshold is around $200,000–$250,000 in combined member balances. Below that, fixed running costs represent a significant fee drag on returns. The true cost depends on the mix of investments and services you engage.

⚠️ Insurance cover held inside an industry or retail fund is typically lost on rollover and may not be replaceable. Get a needs analysis before moving any funds.

📋 Signing the Trustee Declaration is a legal commitment. Not understanding your obligations is not a defence if something goes wrong.

🚫 ATO penalties for serious trustee breaches can reach $18,000 per trustee — and non-compliance can result in the fund being taxed at 45%.

🔑 Your investment strategy is a legal document, not a formality. It must genuinely reflect your objectives, diversification approach, liquidity needs and member insurance requirements.

💡 Always obtain personal advice from a licensed SMSF specialist before establishing a fund or making any rollover decision.

Thinking About an SMSF — or Want a Second Opinion? If you’d like a no-obligation conversation about whether an SMSF is right for your situation — or you want a straight-talking second opinion on an offer you’ve received — reach out. That’s what The SMSF Coach is here for. http://www.smsfcoach.com.au | Sonas Wealth, Sydney www.sonaswealth.com.au

Always make sure that you’re your strategy complies with relevant superannuation and tax regulations before implementation

Are you looking for advisors that will keep you up to date and provide guidance and tips like in this blog? then why not contact us at our Castle Hill or Windsor office in North West Sydney to arrange a one-on-one consultation, just click the Schedule Now button up on the left to find the appointment options.

Please consider passing on this article to family or friends. Pay it forward!

Corporate Authorised Representative of Viridian Advisory Pty Ltd ABN 34 605 438 042, AFSL 476223

This information has been prepared without taking into account your objectives, financial situation, or needs. Because of this, you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation, and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

⚖️ General Advice Disclaimer This article is general information only and does not constitute personal financial, legal or tax advice. The rules governing SMSFs are complex and individual circumstances vary significantly. You should obtain advice from a licensed financial adviser before acting on anything in this article. The author holds AFSL authorisation through Sonas Wealth Pty Ltd, corporate authorised representative of Viridian Advisory 476223.

Hi, I’m Liam Shorte — better known as The SMSF Coach. As a Financial Planner and SMSF Specialist Advisor with over two decades helping families take control of their super, I’ve seen it all. Every week I speak to people who’ve been approached about setting up a Self-Managed Super Fund (SMSF). Some of those approaches are genuine but many are not.

Too often, what looks like helpful advice is really a cleverly disguised sales pitch — designed to get you to move your super so the promoter can sell you their product, charge high fees, or worse, put your retirement savings at risk. The ATO is watching this space more closely than ever, and the consequences for getting it wrong as a trustee are serious and personal.

This is your no-nonsense guide before you sign anything.

1. How Are You Being Approached? Sales Pitch or Genuine Advice?

Legitimate SMSF advice starts with your situation — not the adviser’s product. A proper adviser asks about your retirement goals, risk tolerance, existing super balance, insurance needs, available time, and whether an SMSF even makes sense for your circumstances. Only then do they make a recommendation.

The product-led approach works the other way around. The SMSF is not the goal — it is the vehicle. Someone wants to sell you a property, a managed fund, an unlisted investment, or a crypto platform. The SMSF is simply how they access your superannuation balance.

Warning Signs in How You Were Approached

Unsolicited contact — cold calls, emails, social media ads, or “free seminars” promising to “unlock the power of your super”.

Pressure to act fast — “limited time offer”, “EOFY special”, or “get your money out before the rules change”.

Promises that sound too good to be true — guaranteed returns, easy access to your super before retirement, or “we’ll handle everything so you don’t have to lift a finger”.

Focus on a single product — a specific property deal, crypto scheme, or investment the promoter (or their related parties) controls.

A referral chain where the adviser, accountant, mortgage broker and property manager all recommend each other — and all earn from the same transaction.

If the conversation quickly moves to rolling your super into a new SMSF so they can “invest it for you” or “help you buy that investment property” — stop. That is usually the gateway to selling their product, not acting in your best interest.

💡 From The SMSF Coach Ask yourself one question before you go any further: is this person excited about my retirement goals, or excited about my super balance?

🚩 Red Flag 1: The Approach Starts With a Product, Not Your Situation You were contacted unsolicited — by phone, email, social media or a seminar. The pitch centres on a specific investment or property rather than a review of your financial situation. You feel pressured, rushed, or told there is a deadline you must meet. The adviser cannot clearly explain what they earn if you proceed — or refuses to tell you.

Quick Licence Check — Do This Before Anything Else

Anyone who recommends you set up an SMSF must hold an Australian Financial Services (AFS) licence, or be an authorised representative of a licensee. This is not optional — it is the law. Check them on:

The ASIC Financial Advisers Register (search at moneysmart.gov.au)

The Tax Practitioners Board register (if they are advising on tax matters)

No licence? Walk away immediately and consider reporting them to ASIC.

2. Do They Provide Genuine Education — or Just Hype?

Real SMSF education explains the responsibilities, not just the glamour. Any adviser worth trusting will make sure you understand what you are signing up for before you commit to anything.

What Proper Education Must Cover

The sole purpose test — your SMSF must exist solely to provide retirement benefits to members. No personal benefit, no holidays, no business bailouts.

Arm’s length rules — every transaction must be done on commercial terms, as if with an unrelated third party.

Your annual audit obligation — an independent approved auditor must review your fund every single year.

Investment strategy requirements — you must have a written, current strategy that actually reflects how your fund is invested.

Record-keeping and valuation duties — all assets must be valued at market value at 30 June each year, with supporting evidence.

Your personal liability as trustee — you are personally responsible for compliance. Administrative penalties cannot be paid from fund assets.

Red flag material is all glossy brochures and “success stories” with no mention of the paperwork, record-keeping, or what happens if you get it wrong. If they say “we’ll do it all for you” and gloss over your ongoing trustee duties, they are not educating you — they are disarming you.

💡 From The SMSF Coach An SMSF puts you in the driver’s seat, but you still have to steer. If the promoter doesn’t equip you to understand the road rules, they’re not coaching — they’re selling.

🚩 Red Flag 2: No Meaningful Education Is Being Provided The conversation focuses on the benefits of an SMSF but skips the responsibilities, compliance obligations and time commitment.You have not been told that as trustee you are personally responsible for every investment decision, every lodgement, and every breach — even accidental ones.There is no discussion of your existing insurance or how it may be affected when you roll your balance into a new fund.There is no Statement of Advice (SOA) documenting why an SMSF is specifically recommended for your situation.

3. The True Costs of Running an SMSF

Here is the reality the glossy flyers rarely show. The cost of running an SMSF is one of the most consistently misrepresented aspects of the whole conversation — and for many people at lower balances, it is the deciding factor.

What You Should Expect to Pay

Setup costs: Expect $1,400–$2,000 for a proper trust deed, corporate trustee structure, ATO registration, and an initial investment strategy. Cheap setups often cut corners on documentation you will regret later.

Ongoing costs: Based on the latest ATO statistical data, median annual operating expenses run to approximately $4,139–$4,628 per year. This includes auditor fees, accounting, administration, and the supervisory levy.

Many people are shocked to learn the real annual cost often lands between $3,500 and $6,000 once everything is factored in — before investment fees, platform costs, or adviser fees.

Cost Item

Typical Range

Notes

Trust deed & company setup

$500 – $1,500

Higher for corporate trustee structure

Accounting & tax return

$1,200 – $3,000+

Increases with complexity

Independent audit

$300 – $900

Mandatory every year

ATO supervisory levy

$259

Netted in annual return

Financial advice fees

$2,000 – $5,000+

If you engage an adviser

ASIC company annual fee

$67 / year

Corporate trustee only

LRBA / bare trust setup

$1,500 – $3,000+

Required if borrowing for property

Actuarial certificate

$300 – $600

If fund has pension-phase members

Investment & platform costs

Varies widely

Brokerage, managed fund fees, platform access

Insurance review

Varies

Critical — existing cover is often lost on rollover

The old ASIC figure of $13,900 per year was significantly overstated, but the ATO’s median numbers are the ones you should use as your benchmark. If your balance is under $500,000–$750,000, those fixed costs can seriously erode your returns when expressed as a percentage of your balance.

🔑 Before You Proceed: Demand Written Fee Disclosure Total fees expressed in dollars AND as a percentage of your fund balanceA side-by-side comparison between the SMSF and your current super fund, after all fees and taxFull disclosure of any referral fees, commissions or benefits the adviser or their network receivesConfirmation that ATO administrative penalties are your personal liability — not payable from fund assets

🚩 Red Flag 3: Costs Have Not Been Fully and Transparently Disclosed You have only been quoted setup costs, not ongoing annual running costs.No comparison has been provided between the SMSF and your current fund as a percentage of your balance.No one has mentioned that ATO administrative penalties are personally payable by trustees — not from the fund.Insurance implications of rolling out of your current fund have not been raised.

4. The Most Common Mistakes — and What the ATO Does About Them

The ATO regulates more than 630,000 SMSFs and its compliance data makes uncomfortable reading: contraventions increased by 10% in the 2024 income year, and by a further 13% in the first half of the following year. Here are the traps that catch trustees out most often.

Mistakes I See Every Year

🚨 Illegal early access — setting up an SMSF specifically to withdraw funds before you meet a condition of release (generally age 60 with retirement, or age 65 regardless). This is the ATO’s single biggest compliance focus.

Lending to yourself or related parties — or using SMSF assets to support a struggling business. The ATO’s estimate of prohibited loans this year is $231.7 million.

In-house asset breaches — investing more than 5% of the fund’s assets in related-party assets or loans.

Poor record-keeping and valuations — no market-value asset valuations at 30 June, missing trustee minutes, or unsigned trustee declarations.

No investment strategy — or a strategy that does not match your actual investments.

Mixing personal and fund money — paying private bills from the SMSF bank account, or depositing SMSF income into a personal account.

Contribution cap breaches and NALI — non-arm’s length transactions that trigger punitive tax at the highest marginal rate.

Ignoring ATO authority notices — including excess contribution determinations and commutation authorities. Not responding does not make them disappear.

Non-lodgement of annual returns — approximately 85,000 SMSFs had not lodged their 2023 return as at early 2025. Non-lodgement removes your complying status from Super Fund Lookup, cutting off employer contributions and rollovers.

🚩 The Cost of Getting It Wrong Administrative penalties can reach 60 penalty units — currently around $18,780 per breach, per trustee. Loss of complying fund status means the fund’s income is taxed at 45% instead of 15%. Trustee disqualification goes on the public record and applies to all future SMSF roles. These penalties are paid personally by trustees — not from the fund.

Real ATO Cases That Should Make You Think Twice

The ATO does not just issue warnings — it acts. The following court and tribunal decisions illustrate what happens when things go wrong.

📋 ATO Case: NSW Promoter — Federal Court PenaltyOne of the most striking enforcement actions involved a NSW promoter who set up (or attempted to set up) 35 SMSFs for 68 individuals. She charged fees to help people who were not eligible to access their super to roll it into a new SMSF and withdraw it immediately — often the same day — for home renovations, stamp duty and personal expenses.The Federal Court imposed a $220,000 penalty and banned her from setting up SMSFs for seven years. The individuals involved were also exposed to back-taxes, penalties and trustee disqualification.

📋 ATO Case: Ryan v Deputy Commissioner of Taxation [2015] FCA 1037The Ryans withdrew nearly $210,000 from their SMSF in 68 transactions over three years, leaving a minimal balance. Withdrawals were treated as loans but were completely undocumented, unsecured, interest-free and had no repayment date.The Federal Court found breaches of the sole purpose test, the prohibition on member loans, and the arm’s length requirement. Each trustee was fined $20,000 ($40,000 combined), disqualified as trustees, and had their remaining benefits rolled into a public fund. They were ordered to pay the ATO’s costs.

📋 ATO Case: Fitzmaurice and Commissioner of Taxation [2019] AATA 2217The Administrative Appeals Tribunal upheld the disqualification of a trustee following cumulative breaches: lending to a member, sole purpose test violation, illegal early release, missing annual returns, investments not at arm’s length, failure to maintain current asset valuations, and record-keeping failures.Critically, the Tribunal held that vague verbal advice from the fund’s accountant was not a valid defence. Primary responsibility for compliance rests with the trustee — not the adviser.

Other Schemes the ATO Has Shut Down

Property “rebate” arrangements where part of the purchase price is secretly returned to the member personally.

Contrived property development joint ventures that use related parties to divert profits into the SMSF at non-commercial rates, triggering non-arm’s length income (NALI) rules.

High-return crypto or offshore investment apps pushed after an SMSF is established, using the fund balance as the entry ticket.

📊 ATO Enforcement in Numbers — 2024-25 Over 660 SMSF trustees disqualified in 2023-24, largely due to illegal early accessMore than $7 million in administrative penalties and $16 million in additional tax raised$481.8 million estimated in illegal early access and prohibited loans in the most recent year10% increase in contraventions in 2024 income year, with a further 13% rise in early 2025Most common contraventions: member loans (19%), in-house assets (16%), asset separation (13%)

5. My Final Coaching Advice

An SMSF is a genuinely powerful tool — I’ve helped hundreds of families use them successfully for direct property, shares, and real retirement control. But only when it is the right fit and set up properly. The key question is always: who is this arrangement actually serving?

✅ Before You Say Yes: Your Pre-Commitment Checklist Ask yourself honestly: is this person acting in my best interest, or theirs?Demand clear, written disclosure of all fees and ongoing costs — in dollars, not just percentages.Insist on a Statement of Advice (SOA) that documents why an SMSF is recommended for your specific situation.Insist on proper education about your trustee responsibilities before you sign anything.Check every licence on the ASIC Financial Advisers Register and the Tax Practitioners Board.Get a second opinion from an independent SMSF Specialist Adviser who has no connection to the product being recommended.Confirm your existing insurance coverage position before rolling out of your current fund.If anyone promises access to your super now for a non-retirement purpose — stop. That is illegal, and the ATO will find you.

💡 From The SMSF Coach An SMSF done right is one of the best structures available for building retirement wealth. An SMSF done wrong — for the wrong reasons, promoted by the wrong people — can cost you your retirement savings, your trustee status, and years of financial recovery.

📌 Key Takeaways ✅ An SMSF is right for the right person — but the approach, the advice, and the cost disclosure must all check out first.🚨 If someone approached you unsolicited and led with a product, the starting position is one of conflict of interest.💰 Understand the full annual cost (typically $3,500–$6,000+) and compare it to your current fund before deciding.⚠️ The most common contraventions are member loans, in-house asset breaches and non-lodgement — all carry personal penalties.🔑 Always verify licences, demand a written SOA, and get an independent second opinion.📋 The ATO will find non-compliance. Trustees cannot hide behind their accountant or adviser.

Thinking About an SMSF — or Want a Second Opinion? If you’d like a no-obligation conversation about whether an SMSF is right for your situation — or you want a straight-talking second opinion on an offer you’ve received — reach out. That’s what The SMSF Coach is here for. http://www.smsfcoach.com.au | Sonas Wealth, Sydney www.sonaswealth.com.au

Always make sure that you’re your strategy complies with relevant superannuation and tax regulations before implementation

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why not contact us at our Castle Hill or Windsor office in North West Sydney to arrange a one-on-one consultation, just click the Schedule Now button up on the left to find the appointment options.

Please consider passing on this article to family or friends. Pay it forward!

Corporate Authorised Representative of Viridian Advisory Pty Ltd ABN 34 605 438 042, AFSL 476223

This information has been prepared without taking into account your objectives, financial situation, or needs. Because of this, you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation, and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

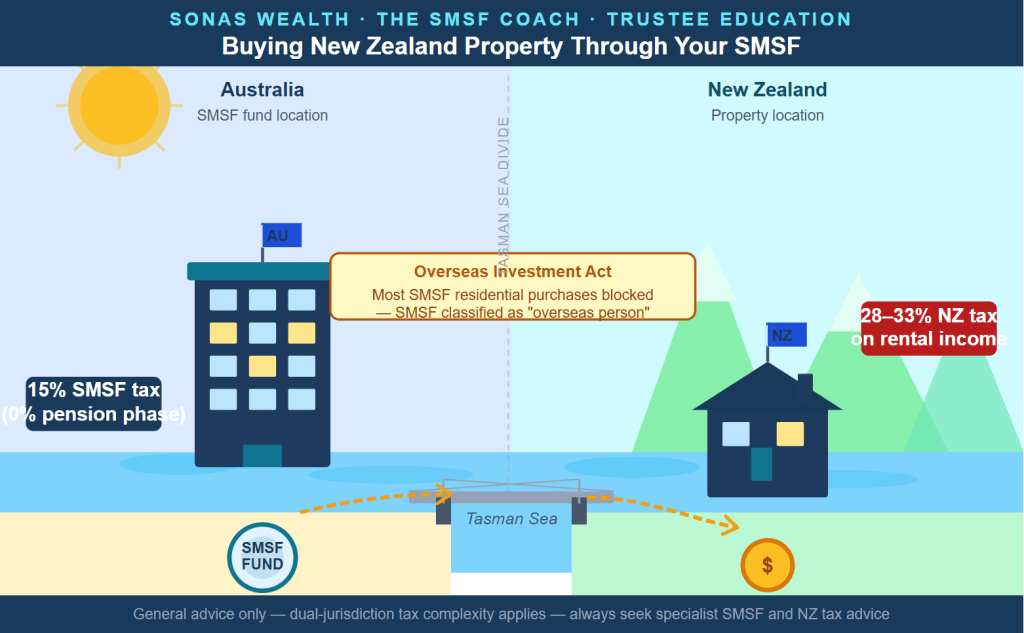

This article is general information only and does not constitute personal financial, legal or tax advice. The rules governing SMSF investments in overseas property are complex and the tax laws of two countries apply simultaneously. You should obtain advice from a licensed financial adviser and a specialist international tax adviser before acting on anything in this article. The author holds AFSL authorisation through Sonas Wealth Pty Ltd corporate authorised representative of Viridian Advisory

Introduction

Australia and New Zealand share more than just the Tasman Sea. We share currency conversations, sporting rivalries, and — for many Australians with family ties, holiday-home dreams, or investment instincts — a temptation to buy property across the ditch. The question I receive more frequently than you might expect is: “Can my SMSF buy a property in New Zealand?”

The short answer is technically yes — but the path is lined with regulatory hurdles, dual-country tax complexity, and structural constraints that make this one of the most challenging overseas investments an SMSF can attempt. It is not a strategy to pursue without specialist advice, and in many situations the practical obstacles mean it simply is not worth the effort.

This article breaks down everything Australian SMSF trustees need to understand before they consider buying a New Zealand property inside their fund.

1. Can an SMSF Legally Own Overseas Property?

First, the baseline: the Superannuation Industry (Supervision) Act 1993 (SIS Act) does not expressly prohibit an SMSF from investing in overseas property. There is no geographic restriction on the asset classes an SMSF may hold, provided every investment decision satisfies the fund’s governing rules and the overarching compliance framework.

In practice, however, several conditions must be satisfied simultaneously for an overseas property purchase to be compliant:

Sole Purpose Test — the acquisition must be made solely to provide retirement benefits to fund members. There can be no present-day benefit to any member or related party.

Investment Strategy — the fund’s documented investment strategy must contemplate overseas property. The trustee must also be able to demonstrate that the holding is consistent with the fund’s risk profile, return objectives, liquidity needs, and diversification requirements.

Trust Deed — the fund’s trust deed must permit investment in overseas or foreign assets. Some older deeds contain geographic restrictions that rule out non-Australian holdings without a deed amendment. Read the Deed!

Arm’s Length Dealings — the property must be purchased from, and (if applicable) leased to, entirely unrelated parties at market rates. No member, relative of a member, or entity connected to a member may acquire a benefit from the property.

Related Party Rules — as with Australian property in an SMSF, residential property cannot be rented to any related party under any circumstances.

In-House Asset Limits — if any arrangement with a related party is involved, the 5% in-house asset limit applies.

Annual Valuation — the fund must obtain an annual market valuation of the property as at 30 June each year, supported by comparative sales evidence in the local market.

🔑 Key ATO Position on Overseas Property