This is part of series on the necessary changes to strategies and opportunities that have resulted from the pending 1 July 2017 changes which will see earnings on transition to retirement (TTR) pensions subject to 15% tax in the fund.

I know this has created concerns with many trustees and advisers around the question of should you access the relief and if so how to actually access the CGT relief provisions. People want to know what factors they must take in to consideration.

Some of the concerns have been clarified by the ATO. One concern was that trustees would need to commute their TTR pensions and roll back into accumulation before 1 July to access the CGT relief provisions. Those relief provisions would allow the cost base of all or selected eligible assets to be reset to the current market value on a date chosen by the trustees between now and 30 June. This CGT relief allows trustees to in effect, retain the tax-free status of unrealised capital gains accumulated prior to 30 June 2017.

The newly issued ATO issued Law Companion Guideline (LCG) 2016/8 has provided some excellent clarification. If your SMSF is operating as an unsegregated fund, the LCG states that member will not need to commute back to accumulation phase to be able to elect to reset the cost base of assets the wish to elect to apply the CGT relief.

It is intended that the same basis should be available for segregated funds, but the ATO has indicated is still reviewing options for how to make this work in practice. I will try to keep this blog updated with any guidance from the ATO on this matter but please make sure you adviser/administrator is on top of these matters. An SMSF that only has TTR or account-based pensions (and no accumulation phase) is automatically classified as a segregated fund. However if you put in a new contribution, as many are, this year then that money goes in to accumulation and the fund becomes automatically unsegregated. So look at your contribution intentions.

All is not lost as the fund would still have been segregated until that contribution was made and you may elect for that date to be the new CGT cost base valuation date.

Conversations need to start with YOUR advisers and administrators to check whether:

you should to continue a TTR pension after 1 July 2017 or to commute back to accumulation phase.

you may have already or can trigger a further condition of release such as leaving any one employment position after age 60. To move from Accumulation or TTR to Account Based Pension

Why are TTR pensions still relevant and for whom

The tax advantages of a TTR pension will reduce when the earnings in the fund start to be taxed on 1 July, but advantages may still arise for members who:

Are over age 60 and can draw tax-free income from the TTR

Wish to start accessing super to top-up income or increase income to pay off debts

Want to be able to nominate an automatic reversionary for estate planning purposes

Can use salary sacrifice or personal deductions to contribute a higher net amount into super than they need to withdraw.

If the TTR pension is no longer required, care should be taken with the commutation and timing of the commutation to ensure the CGT relief provisions can be accessed on any assets they wish to claim the relief for.

Looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make 2016 the year to get organised or it will be 2026 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such

I knew with all the recent changes to Superannuation that many of my clients would need to update their SMSF Trust Deeds and started doing my research for a blog. Then I came across a recent blog from Dr.Brett Davies at Legal Consolidated today and I could not really improve on it. So with his permission, I am re-blogging his content here.

Self-Managed Super Fund (SMSF) Deeds previously required updates in:

– 1999 – ‘Excluded Funds’ became ‘Self-Managed Super Funds’, preservation & in-house assets

– 2007 – ‘Simpler Super’

– 2017 – Legislation passed in 2016, requires the changes below

The 15 changes to SMSF Deeds required after the 2016 Budget are to:

Internally ‘rollback’ pensions to accumulation;

Segregate assets between accumulation and pension phases;

Reject contributions;

Refund contributions;

Deal with excess transfer balance tax and excess non-concessional contributions;

Allow income streams and Account Based Pension (grandfathered);

Specify guardians for incapacity and death;

Identify the Power of Attorney when living overseas for more than 2 years;

Resettle pensions with flexible timing without mingling with accumulation account;

Allow reversionary beneficiary nominations;

Provide for CGT relief;

Deal with segregated and unsegregated assets;

Cease or keep Transition to Retirement Income Streams;

Calculate member balances, across different funds; and

Calculate internal pension rollbacks to accumulation.

These SMSF updates are all required to give maximum flexibility to your accountant and adviser.

Why does my SMSF Specialist Advisor / Accountant want to apply these SMSF updates?

Pre-2012 SMSF Deeds fail to deal with these 10 issues:

Removing clauses requiring the Trustee to do something that is no longer legal or beneficial;

Changing the sections that are ‘regimented’ with unnecessary rules vs being ‘permissive’. There is no point stating mandatory SIS requirements. In fact, it is dangerous to re-state legislation. This is because it dates your deed;

Accounting for an increased concessional contribution cap;

Removing insurance cover where the conditions are out of date;

Incorporating clauses about losing the pension at death or when the minimum payment has not been made;

Allowing for excess concessional contributions taxed at member’s marginal rate (-15% offset);

Updating the Investment Strategy to incorporate the ATO’s new Audit approach;

Changing market valuation clauses to leave the mechanism for the Accountant;

Allowing remuneration for non-trustee duties; and

Allowing non-lapsing Death Benefit Nominations.

Update your Deed to ensure your SMSF is compliant. Then you get the most out of your SMSF.

There is no risk of resettlement

‘Resettlement’ is when you create a new ‘trust estate’ out of an old trust. This applies to SMSFs and causes significant tax implications. However, there is no risk of resettlement under the High Court authority of Commercial Nominees (2010).

Updating your SMSF Deed through Legal Consolidated does not result in the resettlement of your SMSF. We retain the parts of the old Deed that are required by legislation and previous court decisions. But this does not affect a resettlement.

Make sure to check your with your own current deed provider or ask your adviser to check out Legal Consolidated’s offer.

Looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make 2016 the year to get organised or it will be 2026 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

In it latest quarterly review of the SMSF sector Class have indicated that Platform use is actually rising a little among SMSF Trustees from 55% to 58%. However there is some change in the guard in terms of which platforms are seeing inflows. From the media release on the report:

Investment platforms have maintained their share of self-managed super funds in the past two years but the market share of the providers has shifted in favour of the non-aligned in the latest Class SMSF Benchmark Report.

The September quarter Report, based on an analysis of 120,000 SMSFs, shows that slightly less than 1 in 5 SMSFs use platforms and this has remained relatively stable for the past two years. However, the proportion of assets these funds hold on the platform has actually increased since 2014, from 55% to 58%, suggesting that predictions of the imminent demise of platforms in the SMSF market are premature. However, the market share of different platform types has shifted significantly over the same period.

While all platforms increased the value of SMSF assets they held, most institutional platform providers lost ground compared to their non-aligned peers, especially Praemium, HUB24 and netwealth. The notable exception among the institutions was BT, which was able to build on its leading position and grow from 41% to 46% of all platform assets. Excluding BT, institutional platforms saw their share of platform assets drop from 47% to 40%.

I don’t find this a surprise as BT has launched its new generation BT Panorama platform which works especially well for SMSF investors. You can access Cash, very competitive Term Deposits from BT, Westpac and St George as well as shares, hybrids, ETFs, managed funds and managed accounts all on the one reporting platform as well as include external assets in the report. We have started using this platform for new clients as it is keenly priced with no administration charge for cash or term deposits and competitive admin fees for shares and managed funds.

Platform users more likely to use Managed Funds

Again the report also shows a higher use of managed funds by those using Platforms which no doubt is due somewhat to the preference for platforms by many SMSF advisers and also that many trustees use platforms to access sectors or managers they can’t get direct/retail. Again from the report:

The Report also found that SMSFs that use a platform allocate their assets differently to those that don’t. SMSFs that use platforms hold less cash and direct property but almost three times the percentage of managed funds as other SMSFs.

While the two categories of SMSFs have a similar direct exposure to shares, those that use platforms appear to be increasingly holding their equities off the platform, such as through a broker.

You can access the full Class Benchmark report and previous release here

I found the table of the Top 20 investment holdings in each class very insightful as it shows the increase in use of ETFs in SMSF portfolios. Hear is a summary of the top 5 ETFs from the data:

1 IVV Ishares S&P 500 ETF – Chess Depositary Interests 1:1 IshS&P500

2 IOO Ishares Global 100 ETF – Chess Depositary Interests 1:1 Ishglb100

3 STW SPDR S&P/ASX 200 Fund – Exchange Traded Fund Units Fully Paid

4 VTS Vanguard Us Total Market Shares Index ETF – Chess Depositary Interests 1:1

5 VEU Vanguard All-World Ex-Us Shares Index ETF – Chess Depositary Interests 1:1

Likewise the top 5 Managed funds

1 PLA0002AU Platinum International Fund

2 MGE0001AU Magellan Global Fund

3 PLA0004AU Platinum Asia Fund

4 FID0008AU Fidelity Australian Equities Fund

5 MAQ0482AU Winton Global Alpha Fund

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

On the home page of this blog I outline the Benefits of a Self Managed Super Fund – SMSF in some detail. Well, when looking at any investment structure I always like to assess the alternative options and eventual exit strategies. While many of you will know of the Retail and Industry superannuation fund options, you may not be as familiar with a close relation to the SMSF known as a Small APRA fund (SAF). So let’s look at little closer at this option.

What is an Small APRA Fund (SAF)?

An SAF is similar to an SMSF but instead of the client(s) being the trustee(s), a professional licensed trustee is responsible for all of the administrative, compliance and legislative responsibilities of running the superannuation fund.

SAFs offer an alternative for clients looking for the increased flexibility of an SMSF but without the burden of being a trustee and the associated compliance risk. They are also an effective solution for clients who are non-residents or bankrupt and therefore unable to be trustees of an SMSF.

I always warn new clients that if your career or business relies on you being a director then you must take the decision to set up an SMSF very carefully and be ready to put the time and effort in or choose SMSF specialist advisors to ensure your fund remains compliant so that you don’t lose your ability to be a director of any company because of breaching SMSF legislation.

SAFs provide all of the legislative advantages afforded to SMSFs, without the risks associated with breaching legislative compliance requirements.

Let be very honest up front and say this is not a suitable option for small balances as you are incurring an extra layer of trustee fees. However for those with larger balances the option can be very cost-effective especially when you consider the ability to relieve yourself of the trustee responsibilities.

Main benefits of the SAF structure

1. Offloading the Compliance risk

The main advantage of running an SAF is that the compliance risk is borne by the professional licensed trustee whose core responsibility is the provision of trustee services. If an SAF is in breach of the rules, the members of the fund will not be liable for the compliance mistakes of the professional trustee. In an SMSF, all members must be a trustee or director of a corporate trustee which means all members bear the compliance liability. You cannot claim your spouse was solely responsible for running the fund. One case clearly shows the risk of being a “silent trustee”where the verdict found the former wife, in her role as a trustee of the fund, was personally liable when it became non-complying after her former husband stripped out most of the assets and headed overseas. See Shail Superannuation Fund and Commissioner of Tax[2011] AATA 940

2. Administration of the fund

A professional licensed trustee in charge of an SAF typically appoints professional organisations to carry out the administration of the fund or is skilled and experienced enough to avoid common breaches of legislative requirements. As the professional licensed trustee administers all information and transactions, record keeping is typically timely and accurate. In SMSFs, the trustees are typically responsible for collating all the documentation and reports so their chosen administration service can prepare the financials of their fund (Not so hard as it sounds nowadays but when your busy?…paperwork suffers)

3. Travelling overseas for extended periods

SAFs are more flexible for people who may go overseas for an indefinite period compared to SMSFs which are strictly regulated in that circumstance. Members of an SMSF who relocate for an extended period of time have to fulfil two requirements – the central management and control of an SMSF needs to be in Australia, and the active member test needs to be fulfilled . If any of these requirements are breached, the SMSF loses its residency status, is deemed non-compliant and will face exorbitant penalty taxes of up to 46.5%. An SAF however can have offshore members – as long as they are Australian residents for tax purposes.

4. Protection and access to Superannuation Complaints Tribunal

In the case of fraudulent conduct or theft, SAFs have more readily available redress options including a grant of financial assistance as statutory compensation and access to the Superannuation Complaints Tribunal which deals with complaints about the decisions and conduct of APRA-regulated fund trustees and other decision makers. Conversely, no compensation scheme exists for SMSFs and they instead have to rely on courts to resolve disputes or look to the Corporations Law to take action against a financial adviser, accountant or administrator for losses they believe are due to misconduct, negligence or inappropriate action.

5. Disqualified persons – Bankruptcy or Criminal record

Individuals are not allowed to be trustees of an SMSF or directors of a corporate trustee if they have committed a crime involving dishonesty such as fraud, theft or embezzlement or if they have been declared bankrupt. The Tax Office will ban individuals from taking on positions of responsibility in an SMSF if it believes the person has breached the superannuation laws either very seriously or persistently or it believes the person is not a fit or proper person and hence should be disqualified. There are no issues with a disqualified person becoming a member of an SAF as they are not required to fill the role of trustee and it is in fact an often preferred solution for those with an SMSF who find themselves in that unenviable position with assets that aren’t liquid.

6. Responsibility concerns due to ageing or onset of mental illness

Some older people may prefer to use an SAF because they have reached an age where they are no longer able, or may not want to, make effective management and operational decisions. SAFs still allow investors to be in charge of the asset allocation – subject to trustee approval (but they are becoming a lot more flexible) – and to maintain or acquire a similarly broad range of assets and avail of strategies available to SMSF investors. Problems often arise in an SMSF when an older trustee loses the capacity to function and participate in the fund’s inner workings whereas in an SAF, the professional licensed trustee will continue to manage the fund for the benefit of its members.

7. Estate planning

There are a number of estate planning scenarios where an SAF being a better alternative to an SMSF. In an SMSF, the death of a fund trustee changes the composition of the trustees and may provide potential for disputes especially in blended families. In an SAF, the licensed trustee is an independent and unbiased party with no family relationship issues that we often see arise with estates. In an SMSF, it is possible to try to include safeguards into the trust documentation; however, if one of several feuding beneficiaries has the cheque book, it may take the remaining beneficiaries considerable time and expense to track down the person and the money. As one colleague said:

“a remaining trustee with a cheque book can do a lot of damage to an SMSF balance while family fight for control in the courts”

8. Taking care of vulnerable beneficiaries

SAFs can provide very tax effective death benefit income streams to intellectually disabled adult children. The hurdle of the person with a disability or their legal personal representative needing to be a trustee is removed because, unlike an SMSF, an SAF has a professional trustee. The use of the professional trustee also ensures that ongoing services can continue to be provided to a disabled person is over 18 and once the parents have died or lost capacity. There is the ability to pay a death benefit income stream to the disabled child and then have any capital remaining return to the parent’s estate on death.

9. Employer – Employee Fund

In an SMSF, a trustee cannot be an employee of another member – unless they are family. In an SAF however, a member can be an employee of another member. Further, since SAFs have a professional licensed trustee, the related-party issues that crop up in an SMSF are not an issue in an SAF.

In summary while an SMSF may be ideal for people who want to be fully in control of their investment decisions and retirement savings, an SAF is ideal for those who would like to actively participate in investment decisions but retain a low-level of compliance and legislative responsibilities. It is possible to switch from an SMSF to an SAF or vice versa without incurring capital gains tax as all they have to do is retire as trustees themselves and appoint a professional licensed trustee to govern their SAF.

So why may a SAF be a better option than a Retail or Industry Fund?

Moving to a SAF is Not a CGT event whereas it would be if you moved to a retail or industry fund

Likely to be able to keep assets such as direct shares, bullion, collectables and residential and commercial property subject to rules.

The member can still direct investments within the approved list

Member directed death benefit nominations are still possible and in fact often more achievable as the trustee can follow your wishes.

No issues with single member funds

Retains privacy for those in high-profile positions

I would like to acknowledge that much of my information in this area has been gathered from articles and presentations by Julie Steed of Australian Executor Trustees who are very experienced in running SAFs and working as a team with clients and their financial planners.

I hope this guidance has been helpful and please comment below. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want additional information on switching fund structures.We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

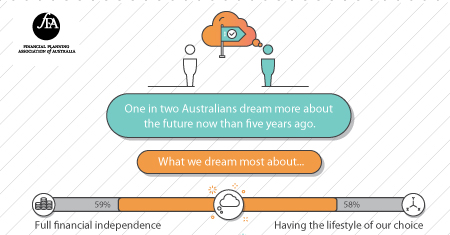

Source: FPA Dare to Dream national research report conducted by McCrindle Research, August 2016

So do you or a family member or friend talk about your future dreams of an early retirement or what you plan to do in retirement but then give a big sigh and say it is “Just a dream” or “a pipe dream” or maybe put it in the “to hard basket” to try and achieve those goals. Realistic goals are achievable with good planning and some of the whackier ones just take a little more effort or courage!

Did you know that this week is Financial Planning Week? Every year, the Financial Planning Association (FPA) holds Financial Planning Week, to remind Australians about the importance of financial planning.

The theme for this year is “Dare to Dream” and I think it’s a great reminder of why we need a plan in place to realise our biggest dreams. After all, financial planning is not just about numbers – it’s about deciding what we want out of life, then putting in steps to achieve it. It’s also a nice reminder about the importance of financial independence – whatever life stage we find ourselves at.

This short video featuring Jane Caro sets the scene to the dare to dream challenge:

So are you ready to read a bit more? Something you might find particularly interesting, is the Dare to Dream research report which has some eye opening insights about how Australians feel about their financial future. The report highlights that whilst one in two Australians dream more about the future now than five years ago, a massive 63% have made “no plans” or “very loose plans” to practically achieve those dreams. Just click the link Dare to Dream research report

The report also shows that property is still a big part of the ‘Great Australian Dream’ (surprisingly even for Gen Y), and that the biggest financial regret in life for Australians is a lack of saving (a huge 47% stated this!). The report is well worth a read.

The FPA has also developed a fun online quiz, to help you discover what kind of financial personality you are. I encourage you to take the quiz and share it on Facebook with your family and friends. You can access this quiz here at Dreamer Profiles

Oh in case you want to know I got “Mover and Shaker” as my financial personality ….my dreams have already been put in to an Action Plan…what about yours?

I hope this guidance has been helpful and please take the time to comment or at least let me know what your personality result was! Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options and achieving those dreams. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

In my earlier blog Get Super Scheme Smart – ATO warns on dangers of retirement planning schemes I went through the ATO guidance and their push to educate trustees about early release schemes and fraud attempts. In a recent case they showed that they will enforce the penalty regime where a trustee has deliberately flouted the rules. The penalty, $40,000 and loss of right to be a trustee in future.

The case of Deputy Commissioner of Taxation v Rodriguez resulted in significant penalties being imposed following a large number of unauthorised withdrawals by an SMSF trustee.

In this case, the fund trustee fabricated a loan arrangement, made cash withdrawals to purchase gold bars (later selling them and depositing the proceeds of sale into his own bank account), as well as making a number of other unauthorised withdrawals for his own personal benefit over a number of years.

The court considered that there had been the following contraventions of the SIS Act:

− in making the loans and giving financial assistance the trustee failed to ensure that the fund was maintained solely for one or more of the purposes prescribed in section 62(1)

− in making the loans and giving financial assistance, the trustee failed to ensure that the fund did not lend money or give any other financial assistance using the resources of the fund to a member, contravening section 65(1)

− the trustee failed to prepare a written plan specifying: the amount by which the in-house assets of the fund exceeded the market value ratio of 5% at the end of each income year; and the steps by which the trustee proposed to dispose of the in-house assets equal to or greater than the excess amount, contravening s 82.

In imposing the penalties, the court took into account the trustee’s cooperativeness with the ATO, investigating officers, solicitors and the court process. The court also accepted that the trustee was contrite and apologetic, and was a person of good character. It was also apparent from the material before the court that the trustee was a troubled person at the time of the contraventions.

It should also be noted that some attempt had also been made to repay amounts withdrawn (including an interest component).

In addition to a monetary penalty of $40,000, the trustee was barred from acting as a trustee.

This should be taken as a strong warning to small business owners and company directors who may also endanger their ability to control their business or be a company director in their business life because of issues caused by managing their Self Managed Superannuation Fund poorly.

For those who feel the additional risk of running an SMSF may expose their career to unacceptable risk then they should consider a retail or industry fund or if you have assets that are unable to be held via one of those, like a property, art or bullion, then you should consider moving the Trustee responsibilities to a professional trustee via a Small APRA fund. I will deal with this option in a future blog.

If you are in a position of financial hardship or want to do a complex investment then why not contact us to se if there is a legal way to achieve the same goal without getting yourself in trouble.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

The old adage “if it sounds too good to be true then it usually is” holds firm especially with superannuation “release” schemes. The ATO is stepping up its education efforts to help consumers while clamping down on promoters of such schemes. Here at SMSF Coach and our sister firm Verante Financial Planning we are always willing to offer a second opinion on any recommendation you are concerned about.

The Australian Taxation Office (ATO) is extending a helping hand to pre-retirees through Super Scheme Smart, a new initiative launched recently that educates people on the dangers of risky and illegal retirement planning schemes.

The ATO has identified a significant number of retirement planning schemes designed solely to help people avoid paying tax on their assets in an illegal manner and is working to close these down.

From the ATO media video below with ATO Deputy Commissioner, Michael Cranston, he warns:

While retirement planning schemes can vary, there are some common features that people should be aware of. Usually these schemes:

• are artificially contrived and complex, usually connected with a SMSF

• involve a lot of paper shuffling

• are designed to leave the taxpayer with minimal or zero tax, or even a tax refund

• aim to give a present day tax benefit by adopting the arrangement

Individuals caught using an illegal scheme identified by the ATO may incur severe penalties under tax laws. This includes risking loss of their retirement nest egg and also their rights as a trustee to manage and operate a SMSF.

The ATO is delivering practical help and information through their Super Scheme Smart website, including a comprehensive information pack, case studies and videos, as well as sending taxpayer alerts into the community about schemes and why they don’t fit within the law.

Mr Cranston urged people undertaking retirement planning to remain vigilant and to come forward if they believe they are at risk or are already involved in a scheme.

“Retirement planning makes good sense provided it is carried out within the tax and superannuation laws. Make sure you are receiving ethical professional advice when undertaking retirement planning, and if in doubt, seek a second opinion from an independent, trusted and reputable expert.

“We do our best to shut down dodgy schemes but the best defence is working together. Blowing the whistle on those promoting retirement planning schemes will help us stop them from risking your or others’ retirement savings,” Mr Cranston said.

All those approaching retirement who are yet to get “Super Scheme Smart”, are encouraged to take advantage of these resources and report promoters of dodgy schemes by calling 1800 177 006, or via email to reportataxscheme@ato.gov.au

Some examples provided of the current schemes they are concerned about include:

The schemes the ATO are currently worried about include:

Dividend stripping – Where the shareholders in a private company transfer ownership of their shares to a related SMSF so that the company can pay franked dividends to the SMSF. The purpose being to strip profits from the company in a tax-free form. (refer to Taxpayer Alert (TA 2015/1))

Non-arm’s length limited recourse borrowing arrangements – When an SMSF trustee undertakes limited recourse borrowing arrangements (LRBAs) established or maintained on terms that are not consistent with an arm’s length dealing. For more information, see Practical Compliance Guide.

Personal services income – Where an individual (with an SMSF often in pension phase) diverts income earned from personal services to the SMSF where it is concessionally taxed or treated as exempt from tax (refer to Taxpayer Alert (TA 2016/6)).

As mentioned above at Verante Financial Planning we take very good care of our clients and ensure all our client strategies are fully compliant and tick all the boxes so our client can sleep securely at night know that while they have used the superannuation and tax systems to maximise their savings position, they are always within the regulations and the spirit of the law.

The whole focus of this blog, the SMSF Coach is about educating and promoting use of legal strategies and we are consistently warning people of the pitfalls of some strategies and investments out there such as our recent warning on the failed GUEVRA IPO not being suitable for SMSF clients or our very popular Property through super in a SMSF – Part 3: 20 most common mistakes

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Let’s start with a definition of what is an Enduring Power of Attorney (EPoA).

An enduring power of attorney is a legal agreement that enables a person to appoint a trusted person – or people – to make financial and/or property decisions on their behalf. An enduring power of attorney is an agreement made by choice that can be executed by anyone over the age of 18, who has full legal capacity.

We make decisions for ourselves on a range of family, work and lifestyle issues everyday and often we are reluctant to admit that there may come a time when we may no longer be able to do so. People don’t like to think about becoming mentally incapacitated by illnesses such as Alzheimer’s or dementia, or becoming physically or mentally incapacitated as the result of an illness or accident. But if it does occur it is vital there is a vehicle in place allowing someone else to legally make decisions.

If we have legal documents prepared prior to us losing capacity to make them, our decisions can be made by someone we know and trust. If we do not have those documents in place before we lose capacity then decisions may have to be made by a government department set up for the purpose of dealing with financial and personal affairs of an incapacitated person.

Most of us given the choice would probably choose the first one but to do this we need to make the documents whilst we have the mental capacity to make them. A person has capacity to make valid legal documents if they can understand why they are making the document and the choices which may be involved (choosing a person to act for you). You must be able to weigh up the result of giving power to someone else to act for you and you must be able to communicate your decision to make a legal document.

The main reason why we have legal documents giving a person or persons the power to act for us is that they will know our wishes and preferences and will act in our best interests. It is also a cost-effective way of protecting our family, finances and assets.

So why is it important for an SMSF member to have an EPoA

Well except in very limited circumstances, a self managed superannuation fund will only qualify as an SMSF where each member of the fund is either a trustee of the fund or a director of the fund’s corporate trustee. It is because of this threshold requirement for existence as an SMSF that the EPoA becomes a very important document for the SMSF member.

Consider the implications for the SMSF if someone is incapable of making decisions:

How does the SMSF run?

How can documents be executed?

How does a corporate trustee operate?

How can a new trustee appointed?

How will assets be bought or sold?

How are pensions or lump sum withdrawals approved and facilitated?

If there isn’t an EPoA what can happen?

Documents requiring two signatures, can’t be executed

Possible Audit contravention

The ATO may render the fund non-complying

Cannot roll-out an incapacitated member as SIS regulations require member consent (can’t be given if incapacitated)

Apply to QCAT, VCAT, NCAT, SAT(for WA) – Civil and Administrative Tribunal

Apply for guardianship

But who will they appoint? Surviving spouse, son/daughter, Public Trustee?

Do you think the Public Trustee wants to be running a SMSF?

What happens to the SMSF while waiting?

Technical Part (I don’t like to quote reams of legislation but sometimes it is necessary)

Subsection 17A(3) if the Superannuation Industry (Supervision) Act 1993 (SISA) provides that an SMSF will continue to be an SMSF where, amongst other things:

(b) the legal personal representative of a member of the fund is a trustee of the fund or a director of a body corporate that is the trustee of the fund, in place of the member, during any period when:

(i) the member of the fund is under a legal disability; or

(ii) the legal personal representative has an enduring power of attorney in respect of the member of the fund;

The term “legal personal representative” is defined at subsection 10(1) of the SISA as follows:

… the executor of the will or administrator of the estate of a deceased person, the trustee of the estate of a person under a legal disability or a person who holds an enduring power of attorney granted by a person.

So, in short, under the superannuation legislation:

the enduring power of attorney is the key to allowing a fund to continue to qualify as an SMSF notwithstanding that the member may not be acting as trustee of the fund;

the enduring power of attorney “relief” can be invoked to assist not only when the member is under a legal disability.

However, as also evident from the above, the fact of the EPoA being drawn up, properly signed and sitting in someone’s drawer is not enough.

Implementing the exercise of the EPoA with your SMSF

In order to meet the requirements set out in the Superannuation Industry (Supervision) Act and the Self Managed Superannuation Funds Ruling SMSFR 2010/2, the following conditions must be satisfied:

The LPR/EPoA must be appointed as a trustee of the SMSF, or as a director of the corporate trustee of the SMSF. The appointment of the LPR/EPoA must be in accordance with the trust deed, the constitution of the trustee company (if any), the Superannuation Industry (Supervision) Act, and any other relevant legislation (such as the Powers of Attorney Act 1998 (Qld), the Guardianship and Administration Act 1990 (WA) and the Corporations Act 2001 (Cth)).

A member who has lost capacity must cease to be a trustee of the SMSF or a director of the corporate trustee upon the appointment of their LPR.

Where the EPoA appoints multiple attorneys, one or more of those attorneys can be appointed as trustee or as director of the corporate trustee in place of the member.

Similarly, multiple members are able to execute an EPoA for the same LPR, who can be appointed as a trustee or a director of the corporate trustee in place of each of those members.

A member is also able to execute an EPoA in favour of an existing member who is a trustee or director of the corporate trustee. In this case, the incapable member can cease to be a trustee, or director of a corporate trustee, and their LPR, already a trustee or director in their own capacity, will also be considered to be appointed in the capacity as LPR for the incapable member.

Acting as a trustee under the EPOA

Once appointed, the attorney performs their duties as trustee or director of the trustee company as a trustee or a director rather than as attorney or agent for the member. The attorney will be subject to the obligations of a trustee and must sign the trustee declaration stating that they understand their duties as a trustee. The attorney cannot be a disqualified person and must be eligible to be appointed as trustee.

The decision to act as an attorney and the legal duties are significant. The attorney must:

Consider the interests of the donor when making decisions as the attorney;

Take care of property/assets;

Avoid conflicts of interest;

Comply with relevant legislation, and

If necessary, prove that they have been appointed your attorney.

In summary

While the decision to grant an EP0A should not be taken lightly, it is an important document which all adult Australian’s should have in place, but it is particularly vital that every adult who is a member of a SMSF execute a valid EPoA. Failing to have an EPoA can result in delays or a financial disaster if a member loses capacity. Having an EPoA will ensure that upon the loss of capacity of a member, the fund can continue to be a complying SMSF.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Ok so as SMSF trustees you are obliged to consider insurance for members but you might think you don’t need it or that you can manage risks. Here is a light-hearted look at some reasons why you might need to reconsider that decision.

Cats have 9 lives. You don’t. Enough said.

Cats get a free ride. You pay the rent/mortgage. Living in an lane way or the bush might work for a feral feline, but for your family, not so much. Your rent or mortgage still needs to be paid regardless of illness, injury or death.

Cats can hunt. You can barely handle the line at the Woolies.

Stalking prey for dinner is not an option. Your family needs cash to put food on the table.

Kittens move out at 8 weeks. Your kids may still be at home when they’re 25..30..and back again at 45 with a few kids in tow!

Your kids may leave for uni at 18, but they could be freeloading off your parental generosity well past their studying years…focusing on becoming an “entrepreneur”, an “artist” or just “finding themselves”.

Cats always land on their feet. You need a safety net. Life on the edge might be thrilling for you, but a nightmare for your family.

Cover your life and your income. Protect your family’s most important asset—you and your earning capacity (unless, of course, you’re a cat).

Contact us to figure out the life and income protection insurance you need.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Rate for 2025-26 Related Property LRBA is 8.95%and Listed Shares 10.95%

Old Rate for 2024-25 Related Property LRBA was 9.35% and Listed Shares 11.35%

The ATO have issued long-awaited guidelines providing SMSF trustees with suggested ‘Safe Harbour’ loan terms on which trustees may use to structure a related party Limited Recourse Borrowing Arrangement (LRBA) consistent with dealing at arm’s length with that related party.

By implementing these “Safe Harbour” loan terms, SMSF trustees are assured by the ATO Commissioner that

..for income tax purposes, the Commissioner accepts that an LRBA structured in accordance with this Guideline is consistent with an arm’s length dealing and that the NALI provisions do not apply purelybecause of the terms of the borrowing arrangement.

It is absolutely essential that all non-bank SMSF borrowing arrangements (LRBAs) be reviewed prior now extended to 1 Jan 2017

Where has this come from?

The ATO first released and then re-issued ATO Interpretative Decisions in 2015 (ATO ID 2015/27 and ATO ID 2015/28), dealing with Non-Arm’s Length Income(NALI) derived from listed shares and real property purchased by an SMSF under an LRBA involving a related party lender – where the terms of the loan were not deemed to be on commercial terms.

These ATOIDs state that the use of a non-arm’s length LRBA gives rise to NALI in the SMSF. Broadly, the rationale for this view is that the income derived from an investment that was purchased using a related party LRBA, where the terms of the loan are more favorable to the SMSF, is more than the income the fund would have derived if it had otherwise being dealing on an arm’s length basis.

NALI is taxed at the top marginal tax rate, currently 47% – regardless of whether the income is derived while the fund is in accumulation phase where tax is normally 15% or in pension phase when the income would usually be tax exempt.

After that bombshell, the ATO announced that it would not take proactive compliance action from a NALI perspective against an SMSF trustee where an existing non-commercial related party LRBA was already in place, as long as such an LRBA was brought onto commercial terms or wound up by 30 June 2016.

The Nitty Gritty Details of the Safe Harbour Steps

The ATO has issued Practical Compliance Guideline PCG 2016/5. As a result, provided an SMSF trustee follows these guidelines in good faith, they can be assured that (for income tax compliance purposes) their arrangement will be taken to be consistent with an arm’s length dealing.

The ‘Safe Harbour’ provisions are for any non-bank LRBA entered into before 30 June 2016, and also those that will be entered into after 30 June 2016.

Broadly, this PCG outlines two ‘Safe Harbours’. These Safe Harbours provide the terms on which SMSF trustees may structure their LRBAs. An LRBA structured in accordance with the relevant Safe Harbour will be deemed to be consistent with an arm’s length dealing and the NALI provisions will not apply due merely to of the terms of the borrowing arrangement.

The terms of the borrowing under the LRBA must be established and maintained throughout the duration of the LRBA in accordance with the guidelines provided.

Safe Harbour 1

Safe Harbour 2

Asset Type

Investment in Real Property

Investment in a collection of Listed Shares or Units

Interest RateNote: as of 10 Jan 2019: The RBA no longer round the rates to the nearest 5 basis points.

RBA Indicator Lending Rates for banks providing standard variable housing loans for investors. Use the May rate immediately preceding the tax year. (2015/16 year = 5.75%)(2016-17 year = 5.65%)(2017-18 year = 5.8%)(2018-19 year = 5.8%)(2019-2020 year = 5.94%)(2020-2021 year = 5.1%) (2021-2022 year = 5.1%)(2022-2023 year = 5.35%)2024 FY = 8.85% (2024-25 year = 9.35%) (2025-26 year 8.95%)

Same as Real Property + a margin of 2%

Fixed / Variable

Interest rate may be fixed or variable.

Interest rate may be fixed or variable.

Term of Loan

Variable interest rate loans:Original loan – 15 year maximum loan term (both residential and commercial).Re-financing – maximum loan term is 15 years less the duration(s) of any previous loan(s) in respect of the asset (for both residential and commercial).Fixed interest rate loan:

Rate may be fixed for a maximum period of 5 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 5.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 5 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

Variable interest rate loans:Original loan – 7 year maximum loan term.Re-financing – maximum loan term is 7 years less the duration(s) of any previous loan(s) in respect of the collection of assets.Fixed interest rate loan:

Rate may be fixed up to for a maximum period of 3 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 7 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 7.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 3 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan cannot exceed 7 years.

Loan-Value –RatioLVR

Maximum 70% LVR for both commercial & residential property. Total LVR of 70% if more than one loan.

Maximum 50% LVR.Total LVR of 50% if more than one loan.

Security

A registered mortgage over the property.

A registered charge/mortgage or similar security (that provides security for loans for such assets).

Personal Guarantee

Not required

Not required

Nature & frequency of repayments

Each repayment is to be both principal and interest.Repayments to be made monthly.

Each repayment is to be both principal and interest.Repayments to be made monthly.

Loan Agreement

A written and executed loan agreement is required.

A written and executed loan agreement is required.

Information sourced from Practical Compliance Guidelines PCG 2016/5.

Potential Trap to be aware of: Importantly, as part of this announcement, the ATO also indicated that the amount of principal and interest payments actually made with respect to a borrowing under an LRBA for the year ended 30 June 2016 must be in accordance with terms that are consistent with an arm’s length dealing.Information sourced from Practical Compliance Guidelines PCG 2016/5.

For the 2017-18 and 2018-19 years the rate is 5.8%

For the 2019-20 year the rate is 5.94%

For the 2020-21 year the rate is 5.1%

For the 2021-22 year the rate is 5.1%

For the 2022-23 year the rate is 5.35%

For the 2023-24 year the rate is 8.85%

For the 2024-25 year the rate is 9.35% until 30 June 2025

For the 2025-26 year the rate is 8.95%

For 2019-20 and later years, the rate published for May (the rate for the month of May immediately prior to the start of the relevant financial year)

It is the applicable rate under Column H of the above spreadsheet (click on link). The rate seems to have started in August 2015 but I assume we must use the May rate from now on.

In referencing the Indicator Rate you can use: Ref: Title: Lending rates; Housing loans; Banks; Variable; Standard; Investor Lending rates; Housing loans; Banks; Variable; Standard; Investor Frequency: Monthly Units: Per cent per annum Source RBA Publication Date 04-Apr-2016 Series ID: FILRHLBVSI

A complying SMSF borrowed money under an LRBA, using the funds to acquire commercial property valued at $500,000 on 1 July 2011.

The borrower is the SMSF trustee.

The lender is an SMSF member’s father (a related party).

A holding trust has been established, and the holding trust trustee is the legal owner of the property until the borrowing is repaid.

The loan has the following features:

the total amount borrowed is $500,000

the SMSF met all the costs associated with purchasing the property from existing fund assets.

the loan is interest free

the principal is repayable at the end of the term of the loan, but may be repaid earlier if the SMSF chooses to do so

the term of the loan is 25 years

the lender’s recourse against the SMSF is limited to the rights relating to the property held in the holding trust, and

the loan agreement is in writing.

We do not consider that this LRBA has been established or maintained on arm’s length terms. The income earned from the property, which is rented to an unrelated party, may give rise to NALI.

At 1 July 2015, the property was valued at $643,000, and the SMSF has not repaid any of the principal since the loan commenced.

If after considering TD 2016/16, it is determined that the income earned from the property is in fact NALI, to avoid having to report NALI for the 2015-16 year (and prior years) the Fund has a number of options.

Option 1 – Alter the terms of the loan to meet guidelines

The SMSF and the lender could alter the terms of the loan arrangement to meet Safe Harbour 1 (for real property).

To bring the terms of the loan into line with this Safe Harbour, the trustees of the SMSF must ensure that:

The 70% LVR is met (in this case, the value of the property at 1 July 2015 may be used).

Based on a property valuation of $643,000 at 1 July 2015, the maximum the SMSF can borrow is $450,100. The SMSF needs to repay $49,900 of principal as soon as practical before 30 June 2016.

The loan term cannot exceed 11 years from 1 July 2015.

The SMSF must recognise that the loan commenced 4 years earlier. An additional 11 years would not exceed the maximum 15 year term.

The SMSF can use a variable interest rate. Alternatively, it can alter the terms of the loan to use a fixed rate of interest for a period that ensures the total period for which the rate of interest is fixed does not exceed 5 years. The loan must convert to a variable interest rate loan at the end of the nominated period.

The interest rate of 5.75% applies for 2015-16 and 5.65% p.a. applies from 1 July 2016 to 30 June 2017. The SMSF trustee must determine and pay the appropriate amount of principal and interest payable for the year. This calculation must take the opening balance of $500,000, the remaining term of 11 years, and the timing of the capital repayment, into account.

After 1 July 2016, the new LRBA must continue under terms complying with the ATO’s guidelines relating to real property at all times.

For example, the SMSF must ensure that it updates the interest rate used for the loan on 1 July each year (if variable) or as appropriate (if fixed), and make monthly principal and interest repayments accordingly.

Option 2 – Refinance through a commercial lender

The fund could refinance the LRBA with a commercial lender, extinguish the original arrangement and pay the associated costs.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant part of the 2015-16 year.

Option 3 – Payout the LRBA

The SMSF may decide to repay the loan to the related party, and bring the LRBA to an end before 30 January 2017.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and the relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant period.

Each option will have many advantages and disadvantages – so it is important to understand what the practical implications of each option are, and how physically you will approach each option. Seek specialised advice on this matter as it is not a strategy suitable for DIY implementation

Important Note to 13.22C or Unrelated Unit Trust Investors

The guidelines provided in this PCG are not applicable to an SMSF LRBA involving an investment in an unlisted company or unit trust (e.g. where a related party LRBA has been entered into to acquire a collection of units in an unrelated private trust or a 13.22C compliant trust). As such, trustees who have entered into such an arrangement will have no option but to benchmark their particular loan arrangement based on commercial loan terms, or to bring the LRBA to an end.

Please visit out SMSF Property page to get details on all available strategies for SMSF property investors.

UPDATE (Relief for those caught by Budget measures)

In a letter to an industry association, the Treasurer, Scott Morrison, has outlined transitional arrangements to allow additional non-concessional contributions above the proposed lifetime limit in certain limited circumstances. Contributions made in the following circumstances may be permitted without causing a breach of the lifetime cap:

where the trustees of a self managed superannuation fund (SMSF) have entered into a contract to purchase an asset prior to 3 May 2016 that completes after this date and non-concessional contributions were planned to be made to complete the contract of sale. Non-concessional contributions will be permitted only to allow the contract to complete provided they are within the relevant non-concessional cap that was applicable prior to Budget night, and

where additional contributions are made in order to comply with the Australian Taxation Office’s (ATO) Practical Compliance Guideline (PCG) 2016/5 related to limited recourse borrowing arrangements, provided they are made prior to 31 January 2017.

Additional non-concessional contributions made under these proposed transitional arrangements will count towards the lifetime cap, but will not result in an excess.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Click here for appointment options.

Liam Shorte B.Bus FSSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 9899 3693, Mobile: 0413 936 299

PO Box 6002, Norwest NSW 2153

U40, 8 Victoria Ave., Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Every time I see the SMSF statistical results issued by the ATO I am dismayed by the number of new SMSF funds being set up with Individual Trustees. I can only assume this is people setting up self managed superannuation funds without good advice or reasonable research.

A few times over the last 5 years I have run polls asking professionals in the SMSF industry whether they would recommend individual or corporate trustees. Every time the overwhelming result is in favour of Corporate Trustees.

So over 90% of professionals who deal day in day out with SMSF issues and like myself deal with some of the fallout when approached by grieving widows(ers), recommend a Corporate trustee for an SMSF.

I have set out my arguments for a Corporate Trustee in this previous article Why Self Managed Super Funds Should Have A Corporate Trustee. If you are considering an SMSF the I would encourage you to read through that article and feel free to pass it on to your friends, family or advisors.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

In another harsh interpretation by the ATO, they has recently released an interpretative decision which says that insurance held in a self managed superannuation fund (SMSF) to fund a buy-sell agreement may breach the sole purpose test and the prohibition on giving financial assistance.

In this interpretative decision the ATO explored a situation where a member of an SMSF and his brother run a business through a company in which they were the only two shareholders.

The SMSF member and his brother entered into a buy-sell agreement. The terms of the agreement required:

the SMSF to purchase a life insurance policy over the life of the member with the insured amount based on an agreed market value of the member’s shares in the company;

the company to make contributions to the SMSF which the SMSF trustee would then use to pay the premiums on the insurance policy. These contributions were in addition to superannuation guarantee contributions and salary sacrificed contribution; and

on the death of the member:

the insurance proceeds were to be paid to the SMSF trustee who would then add the proceeds to the member’s benefits;

the SMSF trustee would then pay the deceased member’s death benefit (including the policy proceeds) to their spouse; and

the deceased member’s shareholding in the company would be transferred to the member’s brother for nil consideration and the deceased member’s spouse will relinquish all claims to that shareholding in the company.

The ATO ruled that the SMSF trustee’s purchase of the life policy contravened both the sole purpose test under section 62 and section 65(1(b) of the Superannuation Industry (Supervision) Act 1993 (SIS Act) which covers the giving of financial assistance by an SMSF to a member or their relative. Breaching the sole purpose test and/or the financial assistance provisions can lead to the SMSF being non-complying and significant monetary penalties being imposed on the SMSF trustees.

Sole purpose test

Broadly the sole purpose test requires an SMSF to be created for the core purposes of providing retirement benefits and death benefits.

Whilst historically the ATO has provided guidance that superannuation funds involved in buy-sell arrangements would not contravene the sole purpose test, the ATO’s decision in ATO ID 2015/10 represents a new position taken by the ATO. Under this new position the ATO indicates that in assessing whether the sole purpose test is met, it will look at all the wider circumstances surrounding a trustee’s decision to make an investment or carry out a particular activity. In the context of buy-sell arrangements this involves the manner and circumstances in which the SMSF are to hold the insurance policy.

Subsection 62(1) of the SISA expressly allows an SMSF to be maintained for the provision of death benefits.

However, the manner and circumstances in which the SMSF came to hold the policy in question caused the ATO to conclude that the benefits sought by the parties of the agreement cannot be regarded as being merely incidental to the core purpose of providing death benefits. The buy-sell agreement is a major component of the member’s and his brother’s company succession plan.

The SMSF is required to use contributions made to it in a manner that may not accord with its investment strategy. The SMSF is essentially directed to invest contributions made to it in an asset it may not otherwise choose to hold.

Having the policy held in the SMSF enables the member’s brother to gain total ownership of the company after the member’s death without personally incurring any expenditure. This immediate benefit to a related party (who is not a member) of the SMSF cannot be described as something that is incidental, remote or insignificant provided to the members of the fund.

Financial assistance provided to a relative of a member

In addition to the sole purpose test concerns discussed above, as the terms of the agreement allow the member’s brother to obtain total ownership of the company upon the member’s death without the need to pay any consideration, the SMSF was also seen to be providing financial assistance to a relative of the member (eg the brother). S.65 of SISA prohibits a SMSF trustee from assisting a member or relative of a member using the fund’s resources. The ATO concluded that the arrangement constituted the provision of financial assistance to the member’s brother which is in breach of section 65(1)(b) of the Act.

What should SMSF’s involved in new buy-sell agreements do?

Although ATO ID 2015/10 is not a binding public ruling, it outlines the ATO’s current position on superannuation and buy-sell arrangements. SMSF trustees and their advisers considering new buy-sell arrangements with the ownership of the policy held in superannuation (SMSF or retail) should consider alternative ownership structures instead.

Existing SMSF arrangements

Unfortunately despite ATO ID 2015/10 representing a change of position by the ATO on buy-sell arrangements, the ATO has not outlined any grandfathering provisions in relation to existing buy-sell arrangements where SMSFs have been involved on the basis of the ATO’s previous view that the sole purpose test was not breached.

As a regular review of the SMSF’s investment strategy is required, which also involves a review of the fund’s insurance arrangements, this review should prompt a discussion by the Trustee(s) around whether existing insurance cover is still required and whether it is still appropriate to hold the cover inside or outside of superannuation.

When conducting such investment strategy reviews, Trustee(s) who have existing buy-sell insurance arrangements funded through their SMSF are encouraged to:

• discuss their options with the fund’s auditor, and/or

• seek SMSF Specific Advice, relevant to their arrangement, from the ATO.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

I have had three calls this week on the subject of making contributions for people who turned 65 this year and want to make non-concessional (after tax) contributions to their funds. I have had to tell one to reject the contribution already made. one to go do some work and the other to relax. The lessons to learn are; do not listen to friends, don’t rush in and seek professional advice from your accountant, financial planner or if you are really smart a SMSF Specialist Advisor™.

Get advice – Get it right

GENERAL INFORMATION ONLY: DO NOT RELY ON THIS CONTENT FOR YOUR PERSONAL SITUATION – GET PERSONAL ADVICE.

If you are 64 then you can still make a contribution of up to the $300,000 max up to June 30th as long as long as you have not triggered your “bring forward” cap previously or exceeded your Total Super Balance Cap.

If you have turned 65 this year already then you can still make a contribution of up to the $300,000 max up to June 30th as long as you meet the work test this year (40 hours in 30 days) or if you meet the criteria for the Work Test Exemption which applies from 1 July 2019. Again you must not have exceeded your Total Super Balance Cap

If you have turned 65 this year already and have not met the work test yet, then you cannot make a contribution until after you meet the work test this year (40 hours in 30 days).

So here is how each of my callers found my advice essential to making their decision.

Client 1

He turned 65 in January 2018 and had fully retired but made a large contribution on the basis he would be managing their son’s business for 2 weeks in June 2018 and would meet the work test easily. As he had not met the test at the time of contribution I had to tell him as SMSF Trustee, he had to reject the contribution and return the funds to his personal account. They can contribute the funds in late June after meeting the work test.

Client 2

He is fully retired and turned 65 in March and at least called me before making the contribution. He has not met the work test yet but has an offer of part-time work in the “Big Green Shed”. Great way of meeting the 40 hours in 30 day Work Test and I personally would probably pay them to work there as I spend so much time and money in there already.

Client 3

She is still working but turns 65 next week and sent through an urgent request to sell down shares in her personal name and so I called to ask why and “her friend had told her she could not use the bring forward rule after her 65th birthday.” So she had panicked and decided to sell down what are excellent shares but with huge capital gains. I had to tell her to relax and take a breath! We have a term deposit maturing in the May and can use that to make the contribution and avoid the estimated $300,000 CGT on the sale of the shares. As she running her own business, she has met the work test and can make her $300,000 contribution anytime up to June 30th 2020 as long as she does not exceed her Total Super Balance cap..

So here is a breakdown of the specific contribution rules applying at various ages.

If you turn 65 in a financial year the question of whether you are able to make a contribution to superannuation depends on:

• the amount you wish to contribute;

• whether you wish to claim a tax deduction for all or some of the contribution;

• whether you need to meet a work test during the year;

• whether you are under your Total Super Balance Cap.

Here are some tables that put it all together.

Table 1: Non-concessional Contributions

Age at the beginning of the financial year

Work test or Work Test Exemption to contribute?

Maximum non-concessional contribution without penalty

Less than 64

No

As long as you have room in your Ttoal Super Balance cap, $100,000 standard non-concessional contribution; $300,000 two year bring forward rule is triggered if greater than $100,000 has been contributed in year 1.

64