As an SMSF Specialist and Financial Planner I do not pretend to my clients that I am an investment guru or that I can tell what will be the next big thing!. I believe my job is to guide them in portfolio construction and advise on diversification while bringing up opportunities to their attention that they may not have considered. This includes some IPO’s and in the last few years I have supported HPI, MPL, QVE, BWP, PIC and avoided some I just couldn’t see long-term value in like MYR, Dick Smith (DSH), McGrath (MEA). I never call them all right but I do limit what clients invest in each to what they can afford to lose.

I did not make these decisions for my clients on my own. I relied heavily for support on services such as our own in-house research team at Magnitude and eQR equities research, third-party research services like Morningstar, Intelligent Investor and discussions with peers and those I believe are thought leaders in the SMSF and Investment space. See the Twitter list here

So when I saw the Guvera IPO come up and having followed them from about 2 years ago when I signed up to their beta service it tweaked my interest. But once I had done my own research and read what others had provided I decided this was a no go area for any SMSF client looking to build wealth for retirement as superannuation is intended.

The figures spoke for themselves. $1.2 million in revenue on a $81.1 million loss and a failed attempt to raise money from size-able seed investors. Believe me there are many sources of venture and angel capital funds out there for good start-up ventures with potential so when an idea has good prospects it will receive support and at such an early stage in its life it should not be seeking a listing on the ASX as it has not proved itself.

I struggle to see how a responsible advisor could recommend a IPO like Guvera’s to many SMSF investors let alone 3000 of them. It appears that the main fund-raiser for this IPO is promoting it via related Accounting firms and rumours of SMSFs being set up just to invest in this IPO as their only current asset. I also question if Accountants and Advisers who have become promoters of this IPO are receiving options or referral fees and assume that they are fully disclosing these to clients who must trust them for guidance. I question whether post July 2016 when Accountants’s will be legally obliged to provide Statements of Advice under a Best Interest’s duty and fully outlining the terms and risks on a personal basis for a client or their SMSF if such an investment could be as targeted to SMSFs.

Its not just me, the Australian Shareholders Association raise concerns about Guvera on Ross Greenwood’s show on 2GB. Listen here for the podcast. http://www.2gb.com/audioplayer/182331

This type of venture is a very, very highly speculative investment suitable for no more than 1-5% of the most aggressive of investors portfolios so I do not believe it should be promoted by private equity through accounting firms or financial planning firms to their SMSF clients. I will call it now as possibly the next Trio or WestPoint.

So that’s my call and guidance I have given to my clients. What are your thoughts? Am I becoming an old fuddy-duddy with no eye to the potential future of this firm?

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Ok so as SMSF trustees you are obliged to consider insurance for members but you might think you don’t need it or that you can manage risks. Here is a light-hearted look at some reasons why you might need to reconsider that decision.

Cats have 9 lives. You don’t. Enough said.

Cats get a free ride. You pay the rent/mortgage. Living in an lane way or the bush might work for a feral feline, but for your family, not so much. Your rent or mortgage still needs to be paid regardless of illness, injury or death.

Cats can hunt. You can barely handle the line at the Woolies.

Stalking prey for dinner is not an option. Your family needs cash to put food on the table.

Kittens move out at 8 weeks. Your kids may still be at home when they’re 25..30..and back again at 45 with a few kids in tow!

Your kids may leave for uni at 18, but they could be freeloading off your parental generosity well past their studying years…focusing on becoming an “entrepreneur”, an “artist” or just “finding themselves”.

Cats always land on their feet. You need a safety net. Life on the edge might be thrilling for you, but a nightmare for your family.

Cover your life and your income. Protect your family’s most important asset—you and your earning capacity (unless, of course, you’re a cat).

Contact us to figure out the life and income protection insurance you need.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I am breaking the Budget down in to bite size chunks with strategies to consider going forward for SMSF Trustees. The first part which dealt with pension strategies is available here . This second part deals with changes to contribution options, methods and caps.

Before I go into detail here is a summary of the changes that are relevant to SMSF members (No coverage of Defined Benefit Schemes in this article):

Concessional (Pre-Tax Contributions like employer superannuation guarantee (SGC), salary sacrifice and those contributions where you claim a tax deduction).

Reduction in the concessional contribution cap to $25,000 regardless of age

Carried forward concessional cap for account balances below $500,000 from 1 July 2018

All individuals under 65 will be eligible to claim a tax deduction for personal contributions (bye bye 10% rule). work test applies ot over those 65

Reduction in income threshold to $250,000 where additional super contribution tax applies

Reduction in contribution tax for people earning less than $37,000

Extension of low-income spouse contribution tax offset

Non-Concessional (Post Tax Contribution like personal after tax contributions and Government co-contributions).

Reduction in Non-concessional contribution cap limit to $100 per annum

Reduction of existing annual non-concessional bring forward provisions

Now the detail:

Reduction in the concessional contribution cap to $25,000 regardless of age

The concessional contribution cap will be reduced from the current level of $30,000 to $25,000from 1 July 2017, irrespective of the age of the individual. The higher cap of $35,000 that currently applies to individuals over age 50 will be abolished. The reduced cap will continue to be indexed in future years in line with wages growth.

Carried Forward or Catch-up concessional contributions

From 1 July 2018 individuals will be able to make additional concessional contributions where they have not reached their concessional contributions cap in previous years. Access to these unused cap amounts will be limited to those individuals with a superannuation balance less than $500,000. Unused amounts accrued from 1 July 2018 will be able to be carried forward on a rolling basis for a period of five consecutive years.

This measure allows some additional flexibility in the timing of your contributions like making $125,000 for a tax deduction on the sale of a property or share portfolio if you did not make contributions in the previous 4 years. Your ability to save may vary throughout your career and this measure will assist to some extent, but falls well short of my preferred option for a lifetime cap on concessional contributions. The restriction based on size of account balance will add complication to the administration of this measure when multiple funds are involved.

All individuals under 65 will be eligible to claim a tax deduction for personal contributions

From 1 July 2017, all superannuation fund members up to age 65 will be able to claim an income tax deduction for personal superannuation contributions up to the concessional contribution cap ($25,000), regardless of their employment circumstances. This is good news for people who are partially self-employed and partially wage and salary earners, and individuals whose employers do not offer salary sacrifice arrangements, as they will benefit from this proposal. Personal contributions for which a tax deduction is claimed will count towards the concessional, rather than the non-concessional cap.

While I accept the government’s intention is to increase flexibility for more people to access the concessional contribution cap if they are able to do so, the mechanism requiring individuals to notify their fund of their intention to claim a tax deduction for their personal contributions will add considerable complexity to fund administration. the “she’ll be right” and “I’ll do it later factor” will lead to many missing opportunities.

Over 65’s will still need to meet the work test.

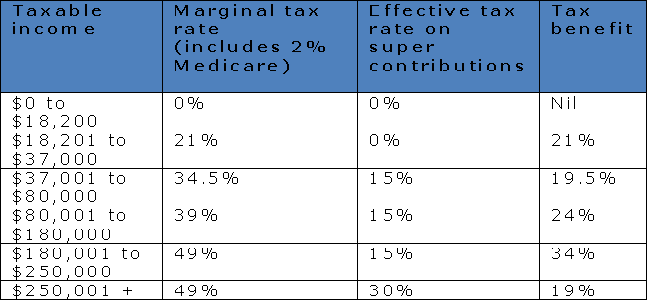

Reduction in income threshold to $250,000 where additional super contribution tax applies

From 1 July 2017, individuals with “relevant income” greater than $250,000 will pay an additional 15 per cent tax on their concessional contributions, down from $300,000. The additional tax, referred to as “Division 293 tax” after the section of the tax legislation which governs the tax, will be payable where the individual’s taxable income (including reportable fringe benefits and certain other amounts) plus concessional contributions (excluding those that exceed the concessional contributions cap) is greater than the $250,000 threshold.

Superannuation still remains attractive despite this change, the 30% tax applied to concessional contributions is still less than the marginal tax rate on earnings so contributing to super remains attractive. But with the lower $25,000 concessional contribution there will be limited scope for you to make optional concessional contributions. For example, if you earn $250,000 and your employer pays the 9.5% SG on your full salary this is an annual employer contribution of $23,750 which has almost fully utilised the new lower cap. If you are on a higher income with disposable income you may look for alternatives outside superannuation or top up your partner/spouse’s superannuation (and potentially receive a tax offset if they earn less than $37,000).

After earlier reports that the threshold would be reduced to $180,000, the proposed threshold of $250,000 means the tax will apply to only around 1 per cent of superannuation fund members. Retention of the existing mechanism which minimises the administrative costs to superannuation funds associated with this tax is welcome.

Reduction in tax for people earning less than $37,000

From 1 July 2017, the Government will introduce a Low Income Superannuation Tax Offset (LISTO) to reduce the tax on superannuation contributions for low-income earners. The measure will apply to individuals with taxable income less than $37,000, and will effectively refund the tax on concessional contributions up to an annual cap of $500. This measure will replace the Low Income Superannuation Contribution (LISC) which was scheduled to be abolished from 1 July 2017, however, the mechanism will be slightly different. Rather than the government making a direct

contribution to the individual’s superannuation account, the offset will apply to the contribution tax deducted by the superannuation fund. The Australian Taxation Office will determine an individual’s eligibility for the LISTO and advise their superannuation fund annually. The fund will then contribute the LISTO to the individual’s account. The government will consult on the implementation of this scheme.

Extension of low-income spouse contribution tax offset

The government will increase access to the low-income spouse superannuation tax offset by raising the income threshold for the low-income spouse from $10,800 to $37,000 and phasing out up to $40,000. This arrangement provides a tax offset of 18 per cent of contributions made by the contributing spouse, up to a maximum offset of $540 per annum.

Non-concessional contribution cap limit of $100,000 or phasing down towards $300,000 using the bring forward provisions

For 2016-17 the single year capped contribution amount is $180,000 and then from 1 July 2017 it reduces to $100,000. So this year you can still use the bring forward rule to contribute the full $540,000 before June 30th 2017 and that has been confirmed by treasury. However if you do not have enough to meet that full contribution limit you can still trigger your cap by contributing at least $180,001 before the end of the year. Note that you may also have already triggered that rule in one of the 2 previous financials years and be wondering how much of the cap you have remaining. Well this table will clarify that for you.

In summary the Limit to Bring Forward Contributions based on year triggered are:

The cap now also limits the ability to use the cash-out and recontribution strategy for members who have triggered a condition of release. We normally used this between age 60 -65 to reduce the taxable component of your account balance. Before considering this strategy you should check the available lifetime cap with your administrator / advisor including all retail / industry funds you have been a member of at any time. Many SMSF members took annual pensions and simply recontributed the payments as NCC every year. DO NOT DO THIS! check your cap first PLEASE!

Phew! that was a lot!

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I am breaking the Budget down in to bite size chunks with strategies to consider going forward for SMSF Trustees. Let’s start with Pensions.

The government is removing the tax exemption for earnings on assets supporting ‘transition to retirement’ pension / income streams but has allowed the pension payments and withdrawals from superannuation by people over age 60 to remain tax-free. No special rules for Self Managed Superannuation funds so these rules apply to all.

Taxing Transition to Retirement Pension earnings

From 1 July 2017 in the TTR pension phase of superannuation the tax-exemption on earnings will no longer apply to transition to retirement (TTR) pensions from.

Most TTRs were started as a tax planning strategy using salary sacrifice and the exempt status of pension income. From 1 July 2017 tax will be applied to the earnings derived in a TTR pension.

In addition, you cannot elect for payments to be taxed as lump sums rather than as pension payments to gain a better tax outcome. We used this for people aged 55-60 and fully retired up until now

Strategy implications for current TTR clients:

SMSFs with existing TTRs for members may wish to maintain them until the changes take effect (and legislation is passed). At that point they should consider one of the following options:

Do a commutation of the pension and roll back to the accumulation phase of superannuation

Convert to a full account-based pension if a condition of release has been met

Continue the Transition to Retirement pension if it suits your circumstances.

Seek advice before making any rash decisions.

From 1 July 2017, 15% tax will be applied to the earnings derived in a TTR pension and combined with the lower concessional contribution caps these strategies are likely to be less effective and less popular but still offer some opportunities for clients so we will review the appropriateness on an individual basis before 1 July 2017

Pension transfer cap of $1.6 million

From 1 July 2017, the maximum amount of superannuation that a person can transfer into pension phase is limited to $1.6 million.

Clients who are already in pension phase before 1 July 2017 will be required to transfer any balance above $1.6 million back into accumulation phase. Clients who are starting pensions from 1 July 2017 cannot roll more than $1.6 million into the pension phase (in total), but the balance rolled over can grow over $1.6 million due to earnings without penalty. some CGT relief will be available on investments moving back to accumulation phase but I will deal with that in a later blog.

The capital value of any Defined Benefit Income Streams will be counted towards the $1.6m limit using a multiple of 16 times the annual income stream.

The ATO has promised a portal or access to a central place where people can check their balances across SMSF, retail, DB and industry funds will be available soon.

Amounts transferred in excess of $1.6 million to retirement will be taxed in a similar way to excess non-concessional contributions. That means both the excess amount and earnings on that excess amount in retirement phase will be taxed. So please do not ignore this limit which applies from 01 July 2017.

Strategy implications for current SMSF pension clients:

This measure limits the tax-free benefits generated from pension phase but do not limit the amount that can be saved in accumulation phase which is only taxed at a maximum of 15%. However the overall amount you can get in to Superannuation is limited by changes to contribution caps.

Those clients who have pension balances in excess of $1.6 million can choose to:

leave savings in the accumulation phase of superannuation where tax on earnings is applied at 15% or

withdraw to invest outside superannuation or

withdraw and recontribute to a spouse / partner with a lower superannuation balance who has not used up their caps.

The $1.6 million cap will be indexed in $100,000 increments in line with the consumer price index. Where a member has previously used up a proportion of their retirement balance limit, they will be able to us the remaining proportion of the indexed cap.

Investment Strategies

We will look at each available strategies to consider the tax implications and comparisons of investment options inside or outside superannuation.

For many the option to withdraw some funds when fully retired and seek other tax effective arrangements including using the Low Income Tax Offset and Seniors and Pensioners Tax Offset to minimise tax on earnings outside of super

For the funds kept in Superannuation we will look at ways to maximise returns from investments within the caps by looking at segregating assets supporting the pension and focusing those on high yield, high return assets that can grow the tax exempt pension balance through earnings above the minimum withdrawal rates. That means we will focus on cash, fixed interest and term deposits in the still concessionally taxed accumulation balance, taxed at a maximum 15%.

Other issues

We have been strong advocates of evening up balances in superannuation between partners and this strategy implemented over the last 10 years will benefit many clients.

The Government has also confirmed that they will remove tax barriers to the development of new retirement income products by extending the tax exemption on earnings in the retirement phase to products such as deferred start lifetime annuities and group self-annuitisation products (Yeah , I am not sure what they are either).

These products can provide more flexibility and choice for Australian retirees, and help them to better manage consumption and risk in retirement.

This change was recommended by the Retirement Income Streams Review. The Government has released the Review and agreed all its recommendations. The announcement also states that they will consult on how the new retirement income products will be treated under the Age Pension means test.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

Rate for 2025-26 Related Property LRBA is 8.95%and Listed Shares 10.95%

Old Rate for 2024-25 Related Property LRBA was 9.35% and Listed Shares 11.35%

The ATO have issued long-awaited guidelines providing SMSF trustees with suggested ‘Safe Harbour’ loan terms on which trustees may use to structure a related party Limited Recourse Borrowing Arrangement (LRBA) consistent with dealing at arm’s length with that related party.

By implementing these “Safe Harbour” loan terms, SMSF trustees are assured by the ATO Commissioner that

..for income tax purposes, the Commissioner accepts that an LRBA structured in accordance with this Guideline is consistent with an arm’s length dealing and that the NALI provisions do not apply purelybecause of the terms of the borrowing arrangement.

It is absolutely essential that all non-bank SMSF borrowing arrangements (LRBAs) be reviewed prior now extended to 1 Jan 2017

Where has this come from?

The ATO first released and then re-issued ATO Interpretative Decisions in 2015 (ATO ID 2015/27 and ATO ID 2015/28), dealing with Non-Arm’s Length Income(NALI) derived from listed shares and real property purchased by an SMSF under an LRBA involving a related party lender – where the terms of the loan were not deemed to be on commercial terms.

These ATOIDs state that the use of a non-arm’s length LRBA gives rise to NALI in the SMSF. Broadly, the rationale for this view is that the income derived from an investment that was purchased using a related party LRBA, where the terms of the loan are more favorable to the SMSF, is more than the income the fund would have derived if it had otherwise being dealing on an arm’s length basis.

NALI is taxed at the top marginal tax rate, currently 47% – regardless of whether the income is derived while the fund is in accumulation phase where tax is normally 15% or in pension phase when the income would usually be tax exempt.

After that bombshell, the ATO announced that it would not take proactive compliance action from a NALI perspective against an SMSF trustee where an existing non-commercial related party LRBA was already in place, as long as such an LRBA was brought onto commercial terms or wound up by 30 June 2016.

The Nitty Gritty Details of the Safe Harbour Steps

The ATO has issued Practical Compliance Guideline PCG 2016/5. As a result, provided an SMSF trustee follows these guidelines in good faith, they can be assured that (for income tax compliance purposes) their arrangement will be taken to be consistent with an arm’s length dealing.

The ‘Safe Harbour’ provisions are for any non-bank LRBA entered into before 30 June 2016, and also those that will be entered into after 30 June 2016.

Broadly, this PCG outlines two ‘Safe Harbours’. These Safe Harbours provide the terms on which SMSF trustees may structure their LRBAs. An LRBA structured in accordance with the relevant Safe Harbour will be deemed to be consistent with an arm’s length dealing and the NALI provisions will not apply due merely to of the terms of the borrowing arrangement.

The terms of the borrowing under the LRBA must be established and maintained throughout the duration of the LRBA in accordance with the guidelines provided.

Safe Harbour 1

Safe Harbour 2

Asset Type

Investment in Real Property

Investment in a collection of Listed Shares or Units

Interest RateNote: as of 10 Jan 2019: The RBA no longer round the rates to the nearest 5 basis points.

RBA Indicator Lending Rates for banks providing standard variable housing loans for investors. Use the May rate immediately preceding the tax year. (2015/16 year = 5.75%)(2016-17 year = 5.65%)(2017-18 year = 5.8%)(2018-19 year = 5.8%)(2019-2020 year = 5.94%)(2020-2021 year = 5.1%) (2021-2022 year = 5.1%)(2022-2023 year = 5.35%)2024 FY = 8.85% (2024-25 year = 9.35%) (2025-26 year 8.95%)

Same as Real Property + a margin of 2%

Fixed / Variable

Interest rate may be fixed or variable.

Interest rate may be fixed or variable.

Term of Loan

Variable interest rate loans:Original loan – 15 year maximum loan term (both residential and commercial).Re-financing – maximum loan term is 15 years less the duration(s) of any previous loan(s) in respect of the asset (for both residential and commercial).Fixed interest rate loan:

Rate may be fixed for a maximum period of 5 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 5.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 5 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

Variable interest rate loans:Original loan – 7 year maximum loan term.Re-financing – maximum loan term is 7 years less the duration(s) of any previous loan(s) in respect of the collection of assets.Fixed interest rate loan:

Rate may be fixed up to for a maximum period of 3 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 7 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 7.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 3 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan cannot exceed 7 years.

Loan-Value –RatioLVR

Maximum 70% LVR for both commercial & residential property. Total LVR of 70% if more than one loan.

Maximum 50% LVR.Total LVR of 50% if more than one loan.

Security

A registered mortgage over the property.

A registered charge/mortgage or similar security (that provides security for loans for such assets).

Personal Guarantee

Not required

Not required

Nature & frequency of repayments

Each repayment is to be both principal and interest.Repayments to be made monthly.

Each repayment is to be both principal and interest.Repayments to be made monthly.

Loan Agreement

A written and executed loan agreement is required.

A written and executed loan agreement is required.

Information sourced from Practical Compliance Guidelines PCG 2016/5.

Potential Trap to be aware of: Importantly, as part of this announcement, the ATO also indicated that the amount of principal and interest payments actually made with respect to a borrowing under an LRBA for the year ended 30 June 2016 must be in accordance with terms that are consistent with an arm’s length dealing.Information sourced from Practical Compliance Guidelines PCG 2016/5.

For the 2017-18 and 2018-19 years the rate is 5.8%

For the 2019-20 year the rate is 5.94%

For the 2020-21 year the rate is 5.1%

For the 2021-22 year the rate is 5.1%

For the 2022-23 year the rate is 5.35%

For the 2023-24 year the rate is 8.85%

For the 2024-25 year the rate is 9.35% until 30 June 2025

For the 2025-26 year the rate is 8.95%

For 2019-20 and later years, the rate published for May (the rate for the month of May immediately prior to the start of the relevant financial year)

It is the applicable rate under Column H of the above spreadsheet (click on link). The rate seems to have started in August 2015 but I assume we must use the May rate from now on.

In referencing the Indicator Rate you can use: Ref: Title: Lending rates; Housing loans; Banks; Variable; Standard; Investor Lending rates; Housing loans; Banks; Variable; Standard; Investor Frequency: Monthly Units: Per cent per annum Source RBA Publication Date 04-Apr-2016 Series ID: FILRHLBVSI

A complying SMSF borrowed money under an LRBA, using the funds to acquire commercial property valued at $500,000 on 1 July 2011.

The borrower is the SMSF trustee.

The lender is an SMSF member’s father (a related party).

A holding trust has been established, and the holding trust trustee is the legal owner of the property until the borrowing is repaid.

The loan has the following features:

the total amount borrowed is $500,000

the SMSF met all the costs associated with purchasing the property from existing fund assets.

the loan is interest free

the principal is repayable at the end of the term of the loan, but may be repaid earlier if the SMSF chooses to do so

the term of the loan is 25 years

the lender’s recourse against the SMSF is limited to the rights relating to the property held in the holding trust, and

the loan agreement is in writing.

We do not consider that this LRBA has been established or maintained on arm’s length terms. The income earned from the property, which is rented to an unrelated party, may give rise to NALI.

At 1 July 2015, the property was valued at $643,000, and the SMSF has not repaid any of the principal since the loan commenced.

If after considering TD 2016/16, it is determined that the income earned from the property is in fact NALI, to avoid having to report NALI for the 2015-16 year (and prior years) the Fund has a number of options.

Option 1 – Alter the terms of the loan to meet guidelines

The SMSF and the lender could alter the terms of the loan arrangement to meet Safe Harbour 1 (for real property).

To bring the terms of the loan into line with this Safe Harbour, the trustees of the SMSF must ensure that:

The 70% LVR is met (in this case, the value of the property at 1 July 2015 may be used).

Based on a property valuation of $643,000 at 1 July 2015, the maximum the SMSF can borrow is $450,100. The SMSF needs to repay $49,900 of principal as soon as practical before 30 June 2016.

The loan term cannot exceed 11 years from 1 July 2015.

The SMSF must recognise that the loan commenced 4 years earlier. An additional 11 years would not exceed the maximum 15 year term.

The SMSF can use a variable interest rate. Alternatively, it can alter the terms of the loan to use a fixed rate of interest for a period that ensures the total period for which the rate of interest is fixed does not exceed 5 years. The loan must convert to a variable interest rate loan at the end of the nominated period.

The interest rate of 5.75% applies for 2015-16 and 5.65% p.a. applies from 1 July 2016 to 30 June 2017. The SMSF trustee must determine and pay the appropriate amount of principal and interest payable for the year. This calculation must take the opening balance of $500,000, the remaining term of 11 years, and the timing of the capital repayment, into account.

After 1 July 2016, the new LRBA must continue under terms complying with the ATO’s guidelines relating to real property at all times.

For example, the SMSF must ensure that it updates the interest rate used for the loan on 1 July each year (if variable) or as appropriate (if fixed), and make monthly principal and interest repayments accordingly.

Option 2 – Refinance through a commercial lender

The fund could refinance the LRBA with a commercial lender, extinguish the original arrangement and pay the associated costs.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant part of the 2015-16 year.

Option 3 – Payout the LRBA

The SMSF may decide to repay the loan to the related party, and bring the LRBA to an end before 30 January 2017.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and the relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant period.

Each option will have many advantages and disadvantages – so it is important to understand what the practical implications of each option are, and how physically you will approach each option. Seek specialised advice on this matter as it is not a strategy suitable for DIY implementation

Important Note to 13.22C or Unrelated Unit Trust Investors

The guidelines provided in this PCG are not applicable to an SMSF LRBA involving an investment in an unlisted company or unit trust (e.g. where a related party LRBA has been entered into to acquire a collection of units in an unrelated private trust or a 13.22C compliant trust). As such, trustees who have entered into such an arrangement will have no option but to benchmark their particular loan arrangement based on commercial loan terms, or to bring the LRBA to an end.

Please visit out SMSF Property page to get details on all available strategies for SMSF property investors.

UPDATE (Relief for those caught by Budget measures)

In a letter to an industry association, the Treasurer, Scott Morrison, has outlined transitional arrangements to allow additional non-concessional contributions above the proposed lifetime limit in certain limited circumstances. Contributions made in the following circumstances may be permitted without causing a breach of the lifetime cap:

where the trustees of a self managed superannuation fund (SMSF) have entered into a contract to purchase an asset prior to 3 May 2016 that completes after this date and non-concessional contributions were planned to be made to complete the contract of sale. Non-concessional contributions will be permitted only to allow the contract to complete provided they are within the relevant non-concessional cap that was applicable prior to Budget night, and

where additional contributions are made in order to comply with the Australian Taxation Office’s (ATO) Practical Compliance Guideline (PCG) 2016/5 related to limited recourse borrowing arrangements, provided they are made prior to 31 January 2017.

Additional non-concessional contributions made under these proposed transitional arrangements will count towards the lifetime cap, but will not result in an excess.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Click here for appointment options.

Liam Shorte B.Bus FSSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 9899 3693, Mobile: 0413 936 299

PO Box 6002, Norwest NSW 2153

U40, 8 Victoria Ave., Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I deal with a lot of couples where one spouse has retired well in advance of the other and has established a routine or habits they are comfortable with and enjoy. The working spouse is often totally engrossed in their career or business with little else in the way of interests or hobbies. When they do eventually retire they can not only struggle to make the most of the free time, but they can also destroy the lifestyle their parter has come to enjoy.

This letter printed in Newsweek in 2004 sums it up better than I ever could and should be a warning to you to ensure your spouse or partner regardless of gender, has interests that extend beyond their working life.

THE ‘GOLDEN YEARS’ ARE BEGINNING TO TARNISH

My worst nightmare has become reality. My husband retired. As the CEO of his own software company, he used to make important decisions daily. Now he decides when to take a nap and for how long. He does not play golf, tennis or bridge, which means he is at home for what seems like 48 hours a day. That’s a lot of togetherness.

Much has changed since he stopped working. My husband now defines “sleeping in” as staying in bed until 6 a.m. He often walks in the morning for exercise but says he can’t walk if he gets up late. Late is 5:30. His morning routine is to take out the dog, plug in the coffee and await the morning paper. (And it had better not be late!) When the paper finally arrives, his favorite section is the obits. He reads each and every one–often aloud–and becomes angry if the deceased’s age is not listed. I’d like to work on my crossword puzzle in peace. When I bring this to his attention, he stops briefly–but he soon finds another article that must be shared.

Some retirement couples enjoy this time of life together. Usually these are couples who are not dependent on their spouse for their happiness and well-being. My husband is not one of these individuals. Many wives I’ve spoken to identify with my experience and are happy to know that they’re not alone. One friend told me that when her husband retired, he grew a strip of Velcro on his side and attached himself to her. They were married 43 years and she hinted they may not make it to 44. Another woman said her husband not only takes her to the beauty shop, but goes in with her and waits! Another said her husband follows her everywhere but to the bathroom… and that’s only because she locks the bathroom door.

When I leave the house, my husband asks: “Where are you going?” followed by “When will you be back?” Even when I’m at home he needs to know where I am every moment. “Where’s Jan?” he asks the dog. This is bad enough, but at least he hasn’t Velcroed himself to me–yet.

I often see retired couples shopping together in the grocery store. Usually they are arguing. I hate it when my husband goes shopping with me. He takes charge of the cart and disappears. With my arms full of cans, I have to search the aisles until I locate him and the cart, which is now loaded with strange-smelling cheeses, high-fat snacks and greasy sausages–none of which was on the shopping list.

Putting up with annoying habits is easier when hubby is at work all day and at home only in the evening and on weekends. But little annoying habits become big annoying habits when done on a daily basis. Hearing my husband yell and curse at the TV during the evening news was bad enough when he was working, and it was just once a day. Now he has all day to get riled up watching Fox News. Sometimes leaving the house isn’t even a satisfying reprieve. When I went out of town for a week and put him in charge of the house and animals, I returned to have my parrot greet me with a mouthful of expletives and deep-bellied belches. It wasn’t hard to figure out what had been going on in my absence.

Not that my husband has any problem acting out while I’m around. He recently noticed that our cat had been climbing the palm trees, causing their leaves to bend. His solution? Buy a huge roll of barbed wire and wrap the trunks. After wrapping 10 palms, he looked like he had been in a fight with a tiger and the house took on the appearance of a high-security prison. Neighbors stopped midstride while on their daily walks to stare. I stayed out of sight. In the meantime, the cat learned to negotiate the barbed wire and climbed the palms anyway.

It is now another hot, dry summer, and the leaves on our trees are starting to fall. Yesterday my husband decided to take the dog out for some fresh air. They stood in the driveway while he counted the leaves falling from the ash tree. Aloud. Another meaningful retirement activity.

I think my husband enjoys being at home with me. I am the one with the problem. I am a person who needs a lot of “alone time,” and I get crazy when someone is following me around or wanting to know my every move. My husband is full of questions and comments when I am on the phone, working on my computer or taking time out to read. It is his way of telling me he wants to be included, wanted and needed. I love that he cares–but he still drives me up the wall.

I receive a lot of catalogs. In one there is a pillow advertised that says grow old with me. the best is yet to be. Another catalog has a different pillow. It reads screw the golden years. Right now it’s a tossup as to which pillow will best describe our retirement years together. Just don’t ask me while I’m working on my crossword puzzle.

Zeh lives in Houston.

Do you get the point I am trying to get across? Retirement takes as much planning as working years. You still have to fill all those waking hours previously filled with commuting and work. If you don’t plan ahead and ensure your partner does too then you could end up destroying both of your retirements and often your relationship. It is no surprise that their has been a rise in what is term “grey divorce as couples find themselves with an empty nest and only each other for company. We start planning the transition to retirement with clients 5-10 years out to ensure they have covered off all facets of their retirement needs. That’s what a professional planner covers rather than just an investment advisor.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of stockimages at FreeDigitalPhotos.net

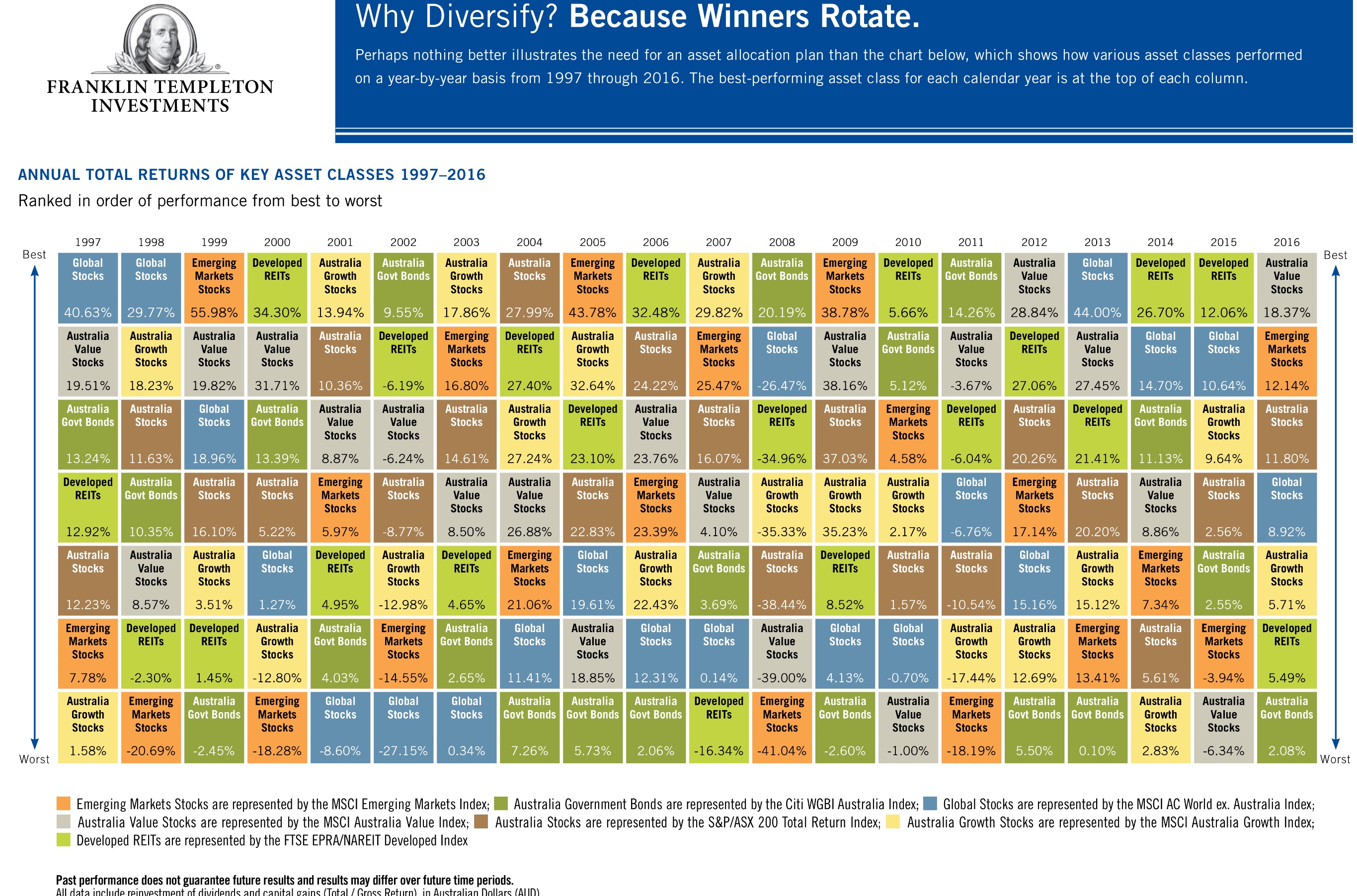

Do you know which asset sector performed best last year, the year before? Do you think those results will guide you for next year? Think again. I don’t think many SMSF Investors would have guessed Australian Listed Property would have been the strongest in 3 out of the last 4 years but in 2016 was a disappointing underperformer. Many burnt in the property sector in the GFC had avoided it like the plague and missed some of the upside.

Franklin Templeton Austalia’s annual asset class ladder for 2016 is a great tool to visualise how each asset class/sector has performed over the last 20 years and pour water on ideas that we can reliably predict next years winners.

What becomes glaringly obvious after scrutinising the table is that no single asset class consistently outperforms the others. Just in case you subscribe to the ‘last years greyhound is this years dog” or that cycles are predictable, the table shows no clues or discernible pattern into how the previous year’s winners or losers will perform in the following year as the pattern appears totally random.

We coach clients to build a diversified strategy with some tactical allocations when sectors or assets appear oversold or opportunities arise like when the Aussie dollar was getting USD $1.10 a few years back and the opportunity came to overweight international stocks.

I hope this information has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

There are many reasons to get a superannuation review especially if you are within 15 years of using your super funds more tax effectively (hint over age 45). A lot can be done to dramatically improve your retirement prospects given time. However if you leave it too late, the chances of making significant improvements are limited. Getting good financial advice can make all the difference to the quality of your retirement. You may not want a full advice service but you can just have a Superannuation and Insurance review. So here are a few reasons why a review could be one of the best decisions you make.

You’ve being putting money in to Super for over 20 years and not sure what it’s doing for you. You have more than one superannuation account and cannot keep a track of how them or how they are performing. Consolidating your accounts together could make keeping track of your savings much easier and moving house less of a hassle!

You may be considering adding funds or your tax agent may have recommended some salary sacrifice and you are suddenly more interested in getting value for money.

You may be interested and want to explore the use of a Self Managed Superannuation Fund known as a SMSF (its only one option but we can help you assess if it is right for you).

You may not be satisfied with the level of service and advice you are receiving from your superannuation company and/or your adviser if you are getting any at all. Many people receive no service at all but continue paying fees year after year. Is it time for you to step-up and demand advice, we invite clients for a review at least twice per year.

You are concerned that your super or multiple accounts may not be performing very well. Sadly, most people in superannuation schemes have little or no idea how their funds are invested or performing from one year to the next. Reports get thrown in a drawer because the jargon is mind bending!

You may be unsure how much risk you are taking with your superannuation investments. It is undeniable that in order to increase your nest egg value, some risk will need to be taken. However the risk you are taking may not be suitable for you and categories like “Balanced or Core” don’t actually mean what they suggest!.

And how about just getting general health check on your super and how it is performing.

Like many people you have accumulated lots of accounts over the years from various jobs ( I recently consolidated 12 accounts for a couple). It may be beneficial to consolidate them all together in one account (wait don’t rush in, review insurance and fees first).

Identify poor performing superannuation funds and move them to investments that have greater potential for growth or a more consistent return.

You may have an SMSF or Superannuation account sitting in cash and just don’t know what to do as you have lost confidence.

You may have multiple/duplicate insurance arrangements across many funds and be paying premiums for cover that may never pay out.

How a superannuation review works

You are likely to have one or more personal accounts and they could be an industry fund, an employer group plan, a personal retail account, or even a transition to retirement pension .

The first step is to complete a Risk Profiling Questionnaire; this is designed to help identify what your attitude to risk is and your comfort with different classes of investment.

The second step it to complete a Fact Find about your personal circumstances so that we have a full understanding of you current situation, your future goals and objectives.

The third step is to obtain full details of all of your current superannuation and insurance arrangements. We ask superannuation companies more than 15 questions, so that we get a full and complete picture of your current situation.

The fourth step is to complete a full and comprehensive analysis of your current arrangements, to identify if your super accounts are working as they should be, that insurance cover is valid and will protect you and your family and fees are under control.

Step five is to recommend a suitable investment strategy to move your Superannuation balance forward, should the review reveal that your existing accounts are not working as well as they should be.

Step six is to implement the recommendations, which may mean re-organising and consolidating your accounts into one super or even a pension fund.

And finally step seven is to keep your arrangements under regular review to ensure that it continues to perform and meet your objectives.

Want a Superannuation Review or are you just looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make this the year to get organised or it will be 2028 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

OK so here we are with only a few weeks left to the end of the financial year to get our SMSF in order and ensure we are making the most of the strategies available to us. Here is a check-list of the most important issues that you should address with your advisers before the year-end. But before we start, one warning:

Be careful not to allow your accountant, administrator or financial planner to reset any pension that has been grandfathered under the new pension deeming rules that came in on Jan 1st 2015 without getting advice on the current and possible future consequences at the current and higher deeming rates.

1. It’s all about timing!

First thing to note is that June 30th falls on a Thirsday this year so be careful about doing anything for your fund after the 27th as funds transferred risk not reaching the destination account before the deadline. Remember it is when the funds are received by the Superannuation fund that counts.

2. Review Your Concessional Contributions – 30K under 49 and $35K if you were 49-64 this year and then work test applies for 65+.

Maximise contributions up to concessional contribution cap but do not exceed your Concession Limit. The sting has been taken out of Excess contributions tax but you don’t need additional paperwork to sort out the problem. So check employer contributions on normal pay and bonuses, salary sacrifice and premiums for insurance in super as they may all be included in the limit.

3. Review your Non-Concessional Contributions (consider before May 3rd – budget night)

Have you considered making non-concessional contributions to move investments in to super and out of your personal, company or trust name. Maybe you have proceeds from and inheritance or sale of a property sitting in cash. As shares and cash have increased in value you may find that personal tax provisions are increasing and moving some assets to super may help control your tax bill. Are you nearing 65? then consider your contribution timing strategy to take advantage of the “bring forward” provisions before turning age 65 to contribute up to $540,000 this year or $180K this year and up to $540,000 next year before you turn 65.

4. Co-Contribution

Check your eligibility for the co-contribution and if you are eligible take advantage. Note that the rules have changed and it is not as attractive as previously but it is free money – grab it if you are eligible.

To calculate the super co-contribution you could be eligible to receive based on your income and personal super contributions, use the Super co-contribution calculator.

5. Spouse Contribution

If your spouse has assessable income plus reportable fringe benefits totaling less than $13,800 then consider making a spouse contribution. Check out the ATO guidance here

6. Over 65? Do you meet the work test? (The 40 hours in any 30 days rule)

You should review your ability to make contributions as if you if you have reached age 65 you must pass the work test of 40 hours in any 30 day period during the financial year, in order to continue to make contributions to super. Check out ATO superannuation contribution guidance

7. Check any payments you may have made on behalf of the fund.

It is important that you check for amounts that may form a superannuation contribution in accordance with TR 2010/1 (ask your advisor), such as expenses paid for on behalf of the fund, debt forgiveness or in-specie contributions, insurance premiums for cover via super paid from outside the fund. See here for more discussion on this topic

8. Notice of intent to claim a deduction for contributions

If you are planning on claiming a tax deduction for personal concessional contributions you must have a valid ‘notice of intent to claim or vary a deduction’ (NAT 71121). If you intend to start a pension this notice must be made before you commence the pension. Many like to start pension in June and avoid having to take a minimum pension but make sure you have claimed your tax deduction first.

9. Contributions Splitting

Consider splitting contributions with your spouse, especially if:

• your family has one main income earner with a substantially higher balance or

• if there is an age difference where you can get funds into pension phase earlier or

• If you can improve your eligibility for concession cards or pension by retaining funds in superannuation in younger spouse’s name.

This is a simple no/low-cost strategy I recommend everyone look at especially with the Government moving on taxing higher balance accounts. See my blog about this strategy here.

10. Off Market Share Transfers (selling shares from your own name to your fund)

If you want to move any personal shareholdings into super you should act early. Here are the links to the Standard Forms for Computershare and here is the Link Market Services Form

11. Pension Payments

If you are in pension phase, ensure the minimum pension has been taken. For transition to retirement pensions, ensure you have not taken more than 10% of your opening account balance this financial year.

The minimum payment amounts have been by 25% for the 2012-13 years. The following table shows the minimum percentage factor (indicative only) for each age group.

Age Minimum % withdrawal (in all other cases)

Under 65 4%

65-74 5%

75-79 6%

80-84 7%

85-89 9%

90-94 11%

95 or more 14%

Sacrificial Lamb

Think about having a sacrificial lamb, a second lower value pension that can sacrificed if minimum not taken. In this way if you pay only a small amount less than the minimum you only have to lose the smaller pensions concession rather than the concession on your full balance. When combined with the ATO relief discussed in the following article “What-happens-if-i-don’t-take-the-minimum-pension” you will have a buffer for mistakes.

Before reading the following:Be careful not to reset a pension that has been grandfathered under the new deeming of pension rules that came in on Jan 1st 2015 without getting advice.

12. Reversionary Pension is often the preferred option to pass funds to a spouse or dependent child.

You should review your pension documentation and check if you have nominated a reversionary pension. If not, consider your family situation and options to have a reversionary pension. This is especially important with blended families and children from previous marriages that may contest your current spouse’s rights to your assets. Also consider reversionary pensions for dependent disabled children

13. Review Capital Gains Tax Position of each investment

Review any capital gains made during the year and over the term you have held the asset and consider disposing of investments with unrealised losses to offset the gains made. If in pension phase then consider triggering some capital gains regularly to avoid building up an unrealised gain that may be at risk to government changes in legislation like those proposed this year. Remember if you plan to sell an asset for the next 2 years the Temporary Budget Repair Levy may mean 2% extra tax

14. Review and Update the Investment Strategy not forgetting to include Insurance of Members

Review your investment strategy and ensure all investments have been made in accordance with it, and the SMSF trust deed. Also, make sure your investment strategy has been updated to include consideration of insurances for members. See my article of this subject here. Don’t know what to do…..call us.

15. Collate and Document records of all asset movements and decisions

Ensure all the funds activities have been appropriately documented with minutes, and that all copies of all statements and schedules are on file for your accountant/administrator and auditor.

16. Double Dipping! June Contributions Deductible this year but can be allocated across 2 years.

For those who may have a large taxable income this year (large bonus or property sale) and are expecting a lower taxable next year you should consider a contribution allocation strategy to maximise deductions for the current financial year. This strategy is also known as a “Contributions Reserving” strategy but the ATO are not fans of Reserves so best to avoid that wording!

17. Market Valuations – Now required annually

Regulations now require assets to be valued at market value each year, ensure that you have re-valued assets such as property and collectibles. Here is my article on valuations of SMSF investments in Private Trusts and Private Companies. For more information refer to ATO’s publication Valuation guidelines for SMSFs.

18. In-House Assets

If your fund has any investments in in-house assets you must make sure that at all times the market value of these investments is less than 5% of the value of the fund. Do not take this rule lightly as the new SMSF penalty powers will make it easier for the ATO to apply administrative penalties (fines) for smaller misdemeanors ranging from $820 to $10,200 per breach.

21. Check the ownership details of all SMSF Investments

Make sure the assets of the fund are held in the name of the trustees on behalf of the fund and that means all of them. Check carefully any online accounts you may have set up without checking the exact ownership details. You have to ensure all SMSF assets are kept separate from your other assets.

22. Review Estate Planning and Loss of Mental Capacity Strategies.

Review any Binding Death Benefit Nominations (BDBN) to ensure they are valid (check the wording matches that required by the Trust Deed) and still in accordance with your wishes. Also ensure you have appropriate Enduring Power of Attorney’s (EPOA) in place allow someone to step in to your place as Trustee in the event of illness, mental incapacity or death. Do you know what your Deed says on the subject? Did you know you cannot leave money to Step-Children via a BDBN if their birth-parent has pre-deceased you?

23. Review any SMSF Loans

Have you provided special terms (low or no interest rates , capitalisation of interest etc.) on a related party loan? Then you need to review your loan agreement and get advice to see if you need to amend your loan. Have you made all the payments on your internal or third-party loans, have you looked at options on prepaying interest or fixing the rates while low. Have you made sure all payments in regards to Limited Recourse Borrowing Arrangements (LRBA) for the year were made through the SMSF Trustee? If you bought a property using borrowing, has the Holding Trust been stamped by your state’s Office of State Revenue.

Don’t leave it until June, review your Self Managed Super Fund now and seek advice if in doubt about any matter.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Happy EOFYS!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

The Government has announced that from 20 March 2015, Centrelink will reduce the deeming rates applicable to allowances and pensions. The lower deeming rate will be reduced from 2 per cent to 1.75 per cent for pensioner and single allowees for financial investments of up to $48,000 and for pensioner couples with investments of up to $79,600.

The higher deeming rate will fall from 3.5 per cent to 3.25 per cent for amounts over the deeming threshold.

This is estimated to affect 770,000 pensioner and allowee recipients according to the Minister for Social Services, Scott Morrison. In the media alert, the Minister suggests that part-pensioners will receive an average increase of $3.20 per fortnight or $83.20 per annum.

In summary the new deeming rates will be as follows:

Deeming Rates from March 2015

This will be received as welcome news to those pension, aged care users and Commonwealth Seniors Health Card recipients who, from 1 January 2015, have been caught by the extension of the deeming rules to account-based pensions.

It may also allow some people who were previously in receipt of the Low Income Health Card to become eligible for it again.

Future changes

The lower deeming rates may not be the end of Centrelink changes with respect to deeming. The Social Services and Other Legislation Amendment (2014 Budget Measures No. 5) Bill 2014 was introduced into the House of Representatives on 2 October 2014. One of the measures contained within this bill was to reset the deeming thresholds to $30,000 for singles and $50,000 combined for pensioner couples from 20 September 2017. This was part of the measures proposed in the May 2014 Federal Budget. To date, the Government hasn’t had any success in moving this Bill through the House and on to the Senate.

Does it make a difference?

Overall, the changes to the deeming rates are a welcome measure for all pensioners and allowees who are not in receipt of the full allowance or age pension. This is especially so for those who own direct shares and/or who are not beneficiaries of the grandfathering of account-based pensions. What will be interesting looking forward is whether there are any interest rate cuts in the near future which affect the deeming rates.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

We are finally seeing the SMSF sector being recognised as the retirement option of preference for engaged investors. Fees and costs are constantly being addressed but what trustees and members need is more confidence in running their funds and that comes through informative content and education.

The industry and the regulator have stepped up a notch in terms of engagement and producing news and educational content for people who want to be active in controlling their future and open to learning more about managing their finances.

Just look at the new content provided by the ATO this year:

For Trustees :

The ATO released 22 short, educational, and entertaining videos, to help you navigate a wide range of events including retirement planning, investment decisions and running an SMSF. We will release more videos next year, covering new topics to help you run your SMSF smoothly and better understand your obligations.

To help people search their website for relevant SMSF information they launched SMSF assist External Link . To use SMSF assist, type in a question or select a topic to get specific information in an instant. SMSF assist and other SMSF services have been added to the ATO app.

News articles, practical case studies and Q&As are now published as they become available and can be accessed anytime through ‘News’ on the left-hand side menu of the SMSF home page.

The ATO quarterly FREE subscription service ‘SMSF News’ has a fresh look and feel, and from 2015 will be issued on a bi-monthly basis.

They will run webinars in 2015 covering different topics for trustees and professionals.

For professionals (in addition to the above services):

The ATO began engaging with SMSF professionals through a live LinkedIn question and answer event hosted by Deputy Commissioner Alison Lendon. The event created dialogue with participants, and we answered SMSF-related questions during the forum.

Building on the success of the LinkedIn forum, they embarked on a series of webinars aimed at SMSF professionals. The webinars highlighted current issues facing the industry and provided an opportunity for participants to ask questions.

To help you better understand your role as a SMSF trustee the SMSF Association has launched a free online resource.

By completing this course, you will have learnt;

The basic facts about Superannuation and Self-Managed Superannuation Funds

How an SMSF works

The investment rules for SMSFs

The administration process to keep your SMSF healthy.

If want a source of constantly updated new on what is relevant to SMSFs then you can get subscribe free to The #SMSF News which picks up most relevant SMSF articles across the web daily. Also if you are on Twitter make sure to follow us as @SMSFCoach and subscribe to this blog up on the left hand column.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

SMSF Specialist Advisor™ & Financial Planner

Tel: 02 8853 6833, Mobile: 0413 936 299

liam@verante.com.au

PO Box 6002 BHBC, Baulkham Hills NSW 2153

Liam Shorte is a partner in VERANTE Financial Planning, Corporate Authorised Representative of Genesys Wealth Advisers Limited, Licence No 232686, Genesys Wealth Advisers Limited ABN 20 060 778 216 • AFSL No.232686

Important information :

The information in this article is provided for illustrative purposes only and does not take into consideration your personal circumstances. You are encouraged to seek financial advice suitable to your circumstances to avoid a decision that is not appropriate. Any reference to your actual circumstances is coincidental. Genesys and its representatives receive fees and brokerage from the provision of financial advice or placement of financial products.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of cooldesign at FreeDigitalPhotos.net

Many SMSF investors are confident with shares, property and term deposits but when it comes to bonds they are feel like they hit a brick wall when they look for solid reasons to consider this sector.

I found this series of articles from Elizabeth Moran that looks at some of the myths around bonds and addresses them in detail. The series addresses the key concerns that SMSF investors mention to me when suggest a potential investment in a bond issue or bond fund. Most of the concerns are based on misinformation on the web and false rules of thumb. So, if you would like to learn more about bonds, this series of articles which looks at the “Seven Key Myths” is a good starting point.

Subscribe to the SMSF Coach blog on the left hand column so that you don’t miss out educational articles like this.

As a thank you to FIIG I will also add a link to their SMSF Solutions page (Not a paid endorsement just a recognition of a good effort)

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Join Us Image courtesy of Stuart Miles at FreeDigitalPhotos.net

The full pricing and allocation details for Australian public applicants has been indicated in a Government Press Release. Applicants will be able to get confirmation of their individual allocation from Tuesday, 25 November 2014 by visiting medibankprivateshareoffer.com.au or calling 1800 998 778. Applicants will need to have their Application Reference Number available.

Transaction confirmation statements will be sent to successful applicants from Thursday, 4 December 2014.

The Government has also exercised its right to claw back a further 20 per cent of the shares previously allocated to the Broker Firm Offer which will no doubt annoy the Broking community even further after a huge scale back in their offer. I cannot help feel there will be a huge amount of shareholders with mediocre holdings and headaches for their accountants and advisers trying to track applications, allocations, scale backs and refunds of excess funds.

Medibank Private will list on the ASX at 12.00pm AEDT on Tuesday, 25 November 2014. Its ASX code will be MPL.