Totally surprised and humbled to have taken out this award as key influencer in the Social Media space in what was a great competition among some of the best and most innovative financial services professionals in the country.

Liam Shorte aka @SMSFcoach winner of Scholar of the Year top in the Social Media Influence Leadership + Excellence Scholarship Award (SMILEYS)

Congratulations also to Sam Henderson and Kimberly Middlemis

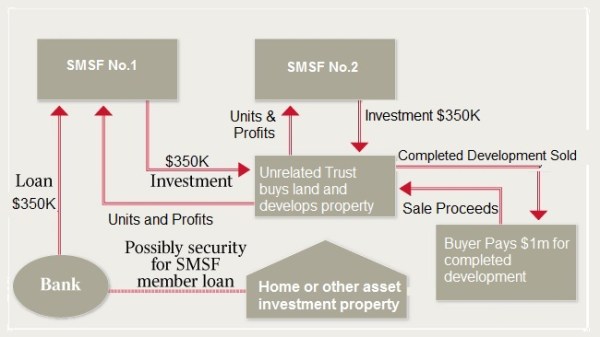

Following on from my previous article How a SMSF can Purchase a Property with a Related Party – Using a 13.22c Trust , another strategy for those wishing to engage in property development with their SMSF involvement is for the fund trustee to invest in a unit trust that holds the development land / existing property by subscribing for units in the unit trust with partners so that no related entity group owns more than 50% of the units in the trust.

Where the fund trustee invests in an unrelated trust the trustee for the unit trust is not required to comply with the requirements of regulation 13.22C of the SIS Regulations. This means that the trustee for the unit trust can borrow to fund the land development without the fund trustee breaching the in-house asset rules in s71 of the SIS Act.

To make it very clear the unit trust will be unrelated if the fund trustee and its associates do not:

exercise Sufficient Influence; or

have a fixed entitlement to more than 50% of the income and capital of the unit trust; or

have the power to remove or appoint the trustee for the unit trust.

So each SMSF or related group of investors can own exactly 50% in combination between them and still maintain an unrelated trust and meet the above requirements.

Keep it simple as it is important that the units in the unit trust carry equal rights to income and capital so that you do not also trigger the non arm’s length income provisions under s295-550 of the Income Tax Assessment Act 1997 (1997 Act).

The diagram below shows 2 unrelated Self Managed Superannuation Funds investing in a unit trust equally (50/50) to carry out a property development. One of the SMSFs uses as related party loan to fund their purchase of the units. Remember it is only the units that are offered as security not the property in the trust.

Each SMSF contributes $350,000 and the property is developed for a total cost of $700,000 and sold for $1m. The$300,000 profit flow back through the Unit Trust to the unit holders equally.

Sufficient Influence

Where two unrelated SMSFs each hold 50% of the units in the unit trust, it is important that the trust management decisions are decided on a 50/50 basis. It should be very clear from documentation and minutes of the trust that decisions are made jointly.

How to avoid distributions to the SMSF being treated as non-arm’s length income?

Where the SMSF invests by way of a unit trust structure, any income received by the fund trustee may be treated as non arm’s length income and taxed at 47% under s295-550(5) of the Income Tax Assessment Act 1997 (1997 Act), where:

the parties are not dealing at arm’s length terms; and

the fund trustee receives an amount it would not otherwise have received if the parties were dealing on arm’s length terms.

Similarly, income the SMSF derives as a beneficiary of the trust, other than because of a fixed entitlement to income, will be treated as non arm’s length income and taxed at 47%.

Therefore, it is important to ensure that the unit trust is a fixed trust, meaning that the entitlement of unit holders to receive income and/or capital from the unit trust is fixed and indefeasible. However, even with a fixed trust it is necessary for the income to be no more than the income that would have been derived if the parties were dealing with each other at arms-length (s295-550(5)).

Managing powers of trustee appointment or removal

Again to avoid falling foul of the legislation, the constitution of the trustee company of the unit trust should be designed to ensure that the SMSF trustee and/or its associates do not have the power to control the trustee by effectively having the power to appoint and remove the trustee for the unit trust by reason that they hold a majority of the shares in the trustee. One trap is a constitution that allows the chairperson to have a casting vote where the chairperson is a SMSF Trustee or representative of the SMSF trustee.

Documentation

When the transaction is structured by way of an unrelated unit trust arrangement, the following documents should be prepared by an experienced legal expert (not off the shelf):

purpose specific unit trust deed and accompanying minutes of meeting; and

unit holders’ agreement all ensuring none of the requirements breached..

Gradual acquisitions of more units by the SMSF

Where a fund trustee invests in an unrelated unit trust the fund trustee may acquire the units held by the other party over time, subject to complying with the provisions of the SIS Act and keeping their related entity group to less than 50% of the overall trust units. Keep in mind that where the unit trust is land rich, there may be a corresponding stamp duty liability and there may be capital gains tax implications for the initial owner as well as valuation fees at each transaction date.

Remember the Sole Purpose Test

In the zest for undertaking any strategy I always remind clients about the reason for undertaking any investment. Your aim should be to provide for a better retirement. If that is not the core purpose then you are breaching the sole purpose test and should reconsider the whole strategy. Also you must review or amend your fund’s investment strategy to ensure this investment falsl within it’s guidelines..

Important information (emphasised for use of this material):

The information in this article is provided for illustrative purposes only and does not take into consideration your personal circumstances. You are encouraged to seek financial, tax and legal advice suitable to your circumstances to avoid a decision that is not appropriate. Any reference to your actual circumstances is coincidental. Magnitude, Verante and its representatives receive fees from the provision of financial advice.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Magnitude Group Pty Ltd ABN 54 086 266 202, AFSL 221557

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of hywards at FreeDigitalPhotos.net

The Australian Tax Office (ATO) has launched a great selection of short educational videos dealing on all matters to do with self-managed superannuation funds (SMSFs). The short animated videos are only 2 -3 minutes each and cover topical subjects as well as key responsibilities for SMSF trustees in an easy to understand format.

The headline for each video contains a link that will take you to the appropriate Tax Office web page, which also publishes the full transcript of the contents of each video if you prefer reading.

This video deals with how SMSFs (or as they used to be known, “do-it-yourself” or DIY super funds) are not really very DIY at all. The video introduces the different people an SMSF trustee will have to work with, or who can help trustees meet their obligations.

SMSF trustees – individual or corporate

Deciding on the type of SMSF trustee is important. This video will help explain the difference between individual trustees and corporate trustees.

SMSF – trustee declaration

A trustee declaration must be completed and kept on file by SMSF trustees. Find out more about it here.

Video currently being updated by ATO

Learn more about the sole purpose test and what it means to your SMSF investments.

Your SMSF needs to meet the sole purpose test to be eligible for the tax concessions normally available to super funds. This means your fund needs to be maintained for the sole purpose of providing retirement benefits to your members, or to their dependants if a member dies before retirement.

Contravening the sole purpose test is very serious. In addition to the fund losing its concessional tax treatment, trustees could face civil and criminal penalties.

It’s likely your fund will not meet the sole purpose test if you or anyone else, directly or indirectly, obtains a financial benefit when making investment decisions and arrangements (other than increasing the return to your fund).

When investing in collectables such as art or wine, you need to make sure that SMSF members don’t have use of, or access to, the assets of the SMSF.

Your fund fails the sole purpose test if it provides a pre-retirement benefit to someone – for example, personal use of a fund asset.

What are super contribution caps? Learn about the types and limits on super contributions and SMSF trustee responsibilities.

Click here for written version while video unavailable

SMSF investment strategy

Your SMSF’s investment strategy is the framework that guides your investment decisions. It pays to have a good investment strategy that is regularly reviewed. Learn what factors your SMSF’s investment strategy needs to take into account.

Watch this video to learn how tax applies when you pay benefits from your SMSF.

Being updated by ATO

SMSF – arm’s length

All SMSF transactions must be on an arm’s-length basis. This means that fund assets must be bought and sold at market value, and income on the assets should show a true market rate of return.

Here the ATO have focused on SMSF loans and early access, with the perceived problem being that people mistakenly think that an SMSF can provide them with a loan, or that they can access their super savings whenever they like.

Thinking about winding up your SMSF? Here are some common reasons for winding up and the steps to follow to get it done.

I will keep this list updated as more videos are released

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Here are some ways to salvage a decent retirement:

Get back in control of your finances now. The first step is to actually sit down (with your partner if you have one) and list out your assets and liabilities and work out what you are actually saving *or not) at present. Understand how you are financing your current lifestyle and then think about what sort of lifestyle you want in the future. If you are borrowing for todays lifestyle then you have little chance of funding the same standards in retirement.

Get out of debt. One of the hardest things about debt is that it feels so overwhelming. The reality is you can’t ignore it and you know deep down that delaying the inevitable only piles on more trouble. Better just to take on your debt and get through it often starting with the high interest rated debt first. A great place to start is the Managing Debt section of the Money Smart government website.

Look to transition to retirement rather than pulling the plug. See if you can extend your savings by working part-time or doing some contract work during the year. Every dollar you earn means a dollar saved from your retirement fund. More and more people are opting to cut back to 4 then 3 days before finally retiring rather than the traditional retirement strategy of working full-time until the day you retire. ask about using a combined Transition to retirement and Salary Sacrificing strategy to boost your retirement savings.

Find a trusted financial adviser. A fee for service financial planner who is recommended to you by someone you know and trust can help you plan for retirement and make the most of your resources in ways you might not have anticipated. Often using the superannuation , tax and social security systems can add as much value as the return on the investments. you may look at consolidating your superannuation, moving investments in to a lower-income earner’s name, leveraging the equity in your home or investments or taking more control of your future using a Self Managed Super fund or a Member Directed Option in your industry or retail fund.

Don’t dip in to your super.Just because you reach preservation age you should not be tempted to dip into your retirement savings. You can use strategies like Transition to Retirement pensions combined with Salary Sacrifice to actually receive the same take home income but in a more tax effective way and also better after tax returns on your savings.

Think twice before indulging the kids.High property prices , unemployment and career breaks to start a family have made it hard for many in their 20s and 30s to get an independent head start, and many families are getting through tough times by living together. But too many parents are giving adult children financial support for house deposits, new cars, medical and school bills and worse still spending money. This is teaching them nothing about saving and parents need to teach life lessons not be their children’s best mate! This financial assistance without teaching about saving and budgeting may be undermining their children’s ability to ever become independent. It also may be dooming parents’ retirement. The kids have more time than you do to make up financial losses. Get your own retirement funding in order before splashing out on the children. Set rules, limits and targets for them and make a loving, firm plan teaching them how to budget and reduce the siphoning from the bank of Mum and Dad while giving wholehearted support in non-financial ways.

Save more and save smarter. Follow the basic rules for retirement savings, including minimising taxes, working longer, investing regularly and keeping on top of your investments. Boost savings by every cent you can and pre-tax if possible Keep increasing your salary sacrifice contributions to meet your retirement goal. Don’t have a goal? Use the Money Smart retirement planner calculators to decide how much you’ll need and what to save to get there.

Don’t touch the equity in your home unless it is adding income. If your retirement is looking shaky, don’t even consider using home equity for non-essentials like renovations or as new car. Use the equity to build wealth rather than destroying it. Talk to a financial planner for strategies and then your accountant to confirm tax consequences when using the equity in your home to work for your retirement. Educate yourself on the pros and cons of any investment so you are comfortable with the strategies as that provides the Sleep factor!.

Plan for the unforeseen and protect your greatest asset.Plan for the unexpected and don’t wait until you’re in trouble to take action. Insurances are an essential part of any long-term plan and your earning capacity is your biggest asset so protect it. See the warning lights. If you’re struggling with mortgage repayments and debt now, even if you want badly to stay in your home, start right away to figure out a fall back plan if you cannot. Pride can prevent you from taking needed action when you’re in trouble. Don’t spend retirement savings or home equity trying to repay unmanageable debt.

what about number 10? Well that’s up to you , let me know what are you doing to rescue your retirement? Just comment blow, you never know who or how many people your idea may help.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98993693, Mobile: 0413 936 299

PO Box 6002 NORWEST NSW 2153

Suite 40, 8 Victoria Ave. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Advisory Pty Ltd ABN 34 605 438 042, AFSL 476223

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Regardless how old you are now, it’s likely you will have a tougher time managing a financially secure retirement than your parents. There is an old saying that “the best time to plant a tree was 20 years ago, the second best time is now!” .

Struggle to Save

Most people just are not putting away enough to fund their retirement or aren’t saving regularly. However the goal posts are also moving and that makes it a bigger task for pre-retirees to plan for and achieve a comfortable lifestyle once they retire

1. We’re living longer.

The proportion of the population aged 65 years or more will increase from around one in seven Australians in 2012 to one in four Australians by 2060, and close to 1 in 3.5 at the turn of the next century[i]

In 1960, a 65-year-old male would live on average another 12 years. Today, according to the Australian Bureau of Statistics (ABS) the average man at 65 can expect to live another 19 years. The average woman will get 22 more years.[ii]

Living an extra 7 years without working takes a lot more savings and better budgeting. Remember these are averages so If there is a history of longevity in your family your retirement savings may need to stretch 30 years or more.

2. Older workers lost out in the GFC. While Australia escaped most of the hurt in the GFC, many companies cut back staff and let go older employees who have failed to find new work opportunities and therefore the earning power from men and women in their late 50s and 60s has been stifled.

Investment savings also plummeted, affecting people of all ages but older Australians have less time to make up those losses by making additional savings or share portfolios recovering over time. The ASX 200 is still below 5400 having dropped during the GFC from 6840

3. Age Pensions are coming under pressure. The increase of the pension access age and the change to the indexing of pensions by CPI rather than average wages as well as the reduction in asset test of thresholds mean that access to the part-pension will be tougher in future years meaning using up more of your own capital earlier.

4. Interest rates are low and look to be lower for longer. Retirees in previous generations earned fairly consistent higher interest on savings and low-risk investments. Today’s retirees must take risks in search of income or endure historically 40 year low fixed-income returns. Five years ago you could get Term Deposits paying 7.5% and now you are lucky to get more than 2.5%

5. People are carrying more debt in to retirement. The standard Aussie family always tried to enter retirement without a mortgage on their home. That’s harder to achieve today. It is common now to see older Australian’s dipping into their superannuation to pay off the mortgage on retirement and more are finding they are increasingly accessing credit card debt and personal loans to fund one-off purchases.

6.We’re working longer. Australians’ average age at retirement is creeping up. The ABS advise that the average retirement age for those who retired within the past five years was 63 for men and 59 for women.[iii].

The upward trend in retirement ages is confirmed in the figures measuring the expectations of those aged 45 and older – around two-thirds intend to retire at or over 65 years of age, with 17 per cent expecting to work until they are 70 or older.

A quarter of workers expect to finish work between 60 and 64 years of age, while only 9 per cent expect to retire before they are 60. But poor health, job loss and the need to care for older parents, grandchildren and ill spouses can cut that short.

7. Rise in Grey Divorce means more retirees are single. Divorce is rising among older Australians, and women tend to outlive their husbands. More than half of retired women in Australia are living in households where the annual income is less than $30,000 with divorced and widowed women among the worst off, according to 2011 research – conducted by the Australian Institute of Superannuation Trustees (AIST). It costs more for a single person to support a household than to share overhead.

Have I shattered your dream or jolted you back to reality? there is no use in pointing our the problems without offering some solutions so check out this post where I outline 10tips for salvaging that retirement dream.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

Have you recently or are you currently looking at setting up an SMSF. There will be loads of paperwork to sign and sometimes the importance of some documents are not stressed enough in the process.

The ATO Trustee Declaration is one of those key documents not to be taken lightly:

The declaration aims to ensure that new trustees understand their obligations and responsibilities.

The declaration lists key matters that you must understand in order to effectively manage an SMSF, including information about:

the sole purpose test

trustee duties

investment restrictions

record-keeping, reporting and lodgement obligations

Watch this video from the ATO for a little more detail then read on below.

I recommend that all new Self Managed Superannuation Fund Trustees complete a short FREE online course about their duties before signing this document. the course is available here at www.smsftrustee.com and yes it is really free with no obligations.

You even get a nice little certificate to put on file once completed. It’s not rocket science but it will clarify how important it is to be aware of your obligations as Trustee of your own fund.

Remember you must complete this compulsory declaration if you become a new trustee (or director of a corporate trustee) of:

a new self-managed super fund (SMSF)

an existing SMSF.

You must sign this declaration within 21 days of becoming a trustee or director of a corporate trustee of an SMSF.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Not sure who to trust for information about setting up and running an SMSF. Well I hope after following my blog for a while you will trust me but I know that takes time so your first port of call might be the regulator for self managed super funds , the ATO.

They have lots of webinars that you can attend live, download a recording to listen at your pleasure or if you prefer to read you can download the transcript.

SMSF trustees

Note: there are no live sessions currently scheduled for these webinars.

However, recordings of past webinars are now available here.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

Most of us who run SMSFs are optimistic as far as our own capabilities and relationships are concerned and that is why we take control of our own finances and plan for the future of our own family. But life can throw curve balls at us (damn I hate using American euphemisms) and we need to be prepared for many of those factors we cannot control.

Foreseeable but unexpected issues such as a relationship breakdown, incapacity or an untimely death all too often catch us by surprise. for SMSF Trustees these are risks that needs to be managed, planned for and reviewed regularly to ensure our funds can be maintained in the short to medium term allowing for our wealth to go where we want it and tax effectively if possible and without disposing of assets in a fire sale.

The ATO have provided yet another little cracker of an educational video for SMSF trustees on planning for the unexpected (relationship breakdown, incapacity, death).

There are a few things to consider when making your plans.

You need to have a plan for what will happen to the fund if a member leaves. It may mean adding a new SMSF member, changing the type of fund or winding up the fund.

Payments from your SMSF must meet the rules in the SMSF trust deed so make sure it covers situations like incapacity, terminal illness or death of a member.

Payments must also meet tax and super laws. In some cases, you may have to withhold tax before paying a super benefit.

You need to consider the insurance needs of members when you set up your investment strategy.

You should consider making a binding death benefit nomination if you want to say who will get your super benefits when you die. An SMSF adviser or estate planner can help you get this right.

It’s also a good idea to consider what will happen if you become incapable of looking after yourself and your affairs.

You may want to appoint an enduring power of attorney who can act as trustee of your SMSF if it’s ever needed.

If relationships in an SMSF break down, you must be prepared to sort out any issues that arise. You can’t force another member to leave or stay in the SMSF or exclude them from the decision-making process.

It pays to make sure your plans including exit strategies are set from the start so that you are prepared for the unexpected. START THE CONVERSATION NOW!

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Our copy of our Financial Services guide can be obtained by clicking here or visiting our main www.verante.com.au website.

So you have reached that point where you want to access your superannuation or your advisor has told you about the tax effectiveness of starting an income stream or more commonly called a pension. So what are the steps involved?

Once an SMSF moves from the accumulation stage to paying an income stream, there are tax benefits available! Watch this ATO video and learn about the conditions that have to be met in order for you to benefit.

When an SMSF moves from the accumulation stage into paying an income stream to a member — there are tax benefits to be had! But — to be eligible the fund must meet certain conditions.

Steps involved in starting a pension or income stream:

A member needs to make a written request to the trustee to start an income stream including some details on what they require and if the pension is to be reversionary to their spouse or partner.

The member receiving the income stream payment must have met a condition of release, for example turning 65. More details here

The type of income stream being paid must be allowed under the law and your fund’s trust deed. Always check your Deed, it’s the instruction manual for your fund

The Trustees of the fund should acknowledge the request and minute the decision to allow the pension based on a condition of release and provide the member with a Pension Agreement and Product disclosure Statement. (this can often be all processed as part of a Pension Kit so just ask your adviser or administrator)

You need to value fund assets when the income stream starts and on one July each year you continue to make payments.

Make sure the minimum income stream payment is paid to the member each year.

You may have to withhold tax from some income stream payments for members aged 55-59. To do this, you’ll need to register for Pay As You Go withholding and complete some forms which you can get from the ATO website here.

At the end of each tax year if more than one member has a share in the fund assets supporting the income stream — you will need an actuarial certificate to work out the tax implications for your fund which is organised by your accountant or administrator.

Even if all members are receiving an income stream, you still have to meet all of your fund’s obligations including arranging the annual audit and lodging the SMSF annual return.

Planning ahead before you start an income stream — and staying on top of the administrative tasks and record keeping will make it easier for your fund to meet all the conditions and enjoy the tax benefits.

Remember — this is a big step for your fund so if you need help you should contact an SMSF professional to help you get it right!

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I try to stress with clients that they will be far more successful in reaching their goals if they take a balanced approach to living , saving and building wealth as they move through life.

Here is a great story that helps put that advice into perspective.

A professor stood before his philosophy class and when the class began, he wordlessly picked up a very large and empty mayonnaise jar and proceeded to fill it with golf balls.

He then asked the students if the jar was full.

They agreed that it was…

The professor then picked up a box of pebbles and poured them into the jar. He shook the jar lightly.

The pebbles rolled into the open areas between the golf balls.

He then asked the students again if the jar was full.

They agreed it was…

The professor next picked up a box of sand and poured it into the jar.

Of course, the sand filled up everything else.

He asked once more if the jar was full.

The students responded with a unanimous ‘yes.’

The professor then produced two Beers from under the table and poured the entire contents into the jar effectively filling the empty space between the sand.

The students laughed…

‘Now,’ said the professor as the laughter subsided, ‘I want you to recognize that this jar represents your life.

The golf balls are the important things–your family, your children, your health, your friends and your favorite passions–and if everything else was lost and only they remained, your life would still be full.

The pebbles are the other things that matter like your job, your house and your savings.

The sand is everything else–the small stuff.

‘If you put the sand into the jar first,’ he continued, ‘there is no room for the pebbles or the golf balls.

The same goes for life.

If you spend all your time and energy on the small stuff you will never have room for the things that are important to you.

So pay attention to the things that are critical to your happiness.

Spend time with your children.

Spend time with your parents.

Visit with grandparents.

Take time to get medical checkups.

Take your spouse out to dinner.

Read a book and stimulate your imagination

Put some money away for tomorrow and some for the long term

Then play another 18…

There will always be time to clean the house and do the filing.

Take care of the golf balls first—the things that really matter.

Set your priorities.

The rest is just sand.

One of the students raised her hand and inquired what the Beer represented.

The professor smiled and said, ‘I’m glad you asked.’

The beer just shows you that no matter how full your life may seem, there’s always room for a couple of beers with a friend.

CHEERS!

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I am delighted to have a guest post from Donal Griffin of Legacy Law on the evolution of the dependency and interdependency rules surrounding receipt of superannuation death benefits. Here is Donal’s summary of a an ATO decision from 2014:

On 18 July 2014, the ATO released ATO Interpretive Decision 2014/22 which confirmed their view that a child who cared for an elderly parent was a dependant and in an inter-dependant relationship.

The writer suggests that it is a sign of the times. 10 years ago, people were keen to show that grandparents’ support for their children by paying school fees meant that the grandchildren were financially dependant with the result that superannuation could be paid to them tax free. The ATO have issued rulings to discourage attempts to contrive dependency.

In February 2014, the ATO showed that certain adult children could be dependants. In ATO ID 2014/6, the Commissioner found that “The Youth Allowance payments the taxpayer received were calculated at a lower ‘at home’ rate as opposed to the higher ‘independent’ rate. This indicates that the taxpayer was substantially financially dependent. A comparison of the level of financial support provided by the taxpayer’s parent with that provided by the Youth Allowance payments also indicates that the taxpayer was financially dependent.”

Private Binding Ruling 67744 dealt with a situation where the parent died. The Commissioner found that all of the requirements of inter-dependency were met.

Previously, it was made clear that support and care must be significant and a link to being unwell or suffering emotionally. This was to be beyond the support one would hope to get from a friend or flatmate who prepares an occasional meal.

The AAT in Malek’s case considered whether the support was necessary. In the later Private Binding Ruling 91657, the above authorities were considered and the net question was whether the person would be able to meet their daily basic necessities (shelter, food, clothing etc) without the additional financial support.

Where a parent needs support, most people would consider it part of the usual familial relationship to support them. However, the facts need to demonstrate that what might be termed a normal familial relationship has changed so that there is a demonstrable mutual commitment to a shared life.

It seems that moving in with a parent and supporting them with a commitment to continue to look after them for the rest of their life is sufficient to establish interdependency. The writer suggests that this relationship can helpfully be confirmed in writing by the parent in the course of their estate planning.

Donal Griffin is a Director of Legacy Law Pty Limited and can be contacted at 02 918803980 or at dgriffin@legacylaw.com.au.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why not contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I get calls from people frequently who mistakenly believe that their SMSF can provide them with a loan or they can access their super whenever they like. This is not the case!

I have seen people with small businesses who get in short-term cash flow problems and think they can dip in to their SMSF to fund the business over the hard time. This is the most common breach of SMSF rules and the ATO is clamping down very hard on those who contravene the rules.

Your SMSF can’t lend money or provide financial assistance to a member or a member’s relative.

Investments by the trustees in arrangements which involve the members themselves, or related parties, are restricted, and more often than not, are NOT ALLOWED.

Watch this video from the ATO for more information.

Superannuation is meant to be the sole Purpose of providing Retirement Income to the members not support for their business. Too often that initial dip leads to larger withdrawals and a downward spiral. Remember if your business is in trouble then your Superannuation maybe the only asset actually protected in the event of Bankruptcy so don’t dip in!

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Your SMSF’s investment strategy is the framework that guides your investment decisions. It pays to have a good investment strategy that is regularly reviewed. Watch this video to learn what factors your SMSF’s investment strategy needs to take into account.

The following warning list should be considered for every investment . If the answer is yes to any of these then seek advice before committing to the investment. They may be possible but there are usually processes and limitations you must be aware of in advance.

Does the proposed investment involve any arrangement or transaction that involves the trustees acquiring an asset from a member or any person that is related, either personally or by business, to a member?

Does the proposed investment involve any arrangement or transaction that involves lending money to a member, relative or a member or related party? (includes companies and trusts).

Does the proposed investment involve any form of borrowing or future obligation to repay money? Check your Trust Deed and the Limited Recourse Borrowing Rules

Does the proposed investment involve any arrangement or transaction that would allow a member or any person or business entity that is related either personally or by business to a member to receive a financial or personal benefit from the asset?

So many people want basic ideas on what they can invest in with their SMSF. Just read my previous blog What can my SMSF invest in? for some details

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Well my jaw really dropped this morning when I saw a distribution statement from Perpetual Wholesale Industrial Share fund for a client with a distribution amounting to over 20% of the fund’s value. Perpetual had flagged a higher than usual distribution in their May – “Investing Matters” newsletter but the large distribution still caught most people by surprise.

Perpetual Wholesale Industrial Share Unit Price

Following the distributions hitting the bank accounts to-day I was one of the callers searching for an explanation from Perpetual. Well they got their act together and this afternoon (15th May 2014) they issued a statement and while I am a bit annoyed about how it was processed I think the Fund Managers have hit the nail on the head and are doing what we pay them to do i.e. Manage the risk in the portfolio and take strategic positions.

Their explanation of the reasons for the huge capital gain component of the distribution was clear and unambiguous.

What factors have driven the high distributions? The Australian sharemarket has performed strongly over the past year, with the S&P/ASX 300 market up 10.1% over the 12 months to 30 April 2014. Both funds have performed exceptionally well over this period – the Perpetual Wholesale Industrial Share Fund has returned 12.9% over the past 12 months, and the Perpetual Wholesale Australian Share Fund has returned 14.9%.

Within this environment, we have adhered to our strong selling discipline of rotating into stocks with more attractive valuations and have realised profits in many of the largest overweight positions in the two funds.

Where have we realised capital gains? Perpetual believes that the major Australian banks are now some of the most expensive banks in the world, and have reduced our exposure in these stocks over the past year accordingly.

Telstra has been a large and successful investment in the funds over the past five years. Over this period, the stock has gone from being one of the cheapest telecommunications stock in the world to being one of the most expensive. Earnings and dividends have remained relatively stagnant throughout and we have reduced our exposure in the stock.

Fox, previously part of News Corporation, was another large weighting which has performed strongly (+100%) and has subsequently been de-listed in Australia. We have deemed it prudent to reduce exposure to Fox as it leaves the Australia Stock Exchange. Large selling of Crown and Resmed driven by valuations of these stocks also saw large capital gains in the funds.

Perpetual’s move has mirrored my own feelings on some of the Top 20 stocks over the last 6 months and I am pleased they have been pro-active in their funds management.

My one concern for Perpetual is that while many have distribution reinvestment plans in place, others don’t and I can foresee that many will not reinvest cash distributions back to this manager and will look to use the distributions to add diversity to their portfolios via international or mid-cap stocks. It’s a shame that a positive move by the fund manager may result in negative funds flow.

I am happy to disclose that this fund has been a core part of many of my clients portfolios for more than 15 years and their track record has been excellent.

I also wonder if the sell down by Perpetual and others has masked the effect of the huge move from term deposits to direct shares by retail and SMSF clients in search of yield. There could be pain ahead for those late on the bandwagon.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Client Question : My next question is about the threshold income level at which my wife and I will start to pay personal tax in 2024-5 due to an inheritance. I read “about $31,888 tax-free” in the paper the other day for my situation (age >67), but my wife does not turn 67 until late 2025, so her level may be different. It would be useful to know these numbers in case we decide to take some lump sums out of super because of the new limits, and invest that money tax-free and also free of SMSF red tape.

Image courtesy of Stuart Miles /FreeDigitalPhotos.net

Personal Tax-free Thresholds

The amount you can earn before you have to pay tax, actually depends on your age.

Under 67

For those people under age 67, the effective tax-free threshold from 1 July 2025 is $22,575. How do we calculate this amount? Well, if you look at the ATO’s current Individual income tax rate table, you pay no tax on the first $18,200 you earn in a year.

However, you also get the benefit of the full low income tax offset if you earn below $37,500. That means the tax office will offset up to $700 from the tax you would normally have to pay. So you can earn another couple of thousand dollars before you have to pay tax.

How much can I earn before paying taxes after age 67

For those who have reached age pension age, they can earn even more without paying tax. If you are over 67, you get access to the Seniors and Pensioners Tax Offset (SAPTO). This reduces or eliminates the tax that would normally be liable to pay on some additional income

Using the SAPTO benefit, the amount you can earn each year as a pensioner before having to pay tax, is:

$35,813 for single people,

$31,888 each for members of a couple or $63,776 combined.

The beauty of this benefit is that for clients in the SMSF Pension phase any income drawn from a super fund income stream once over 60 is tax-free and non-assessable, meaning it doesn’t count towards the above thresholds.

Based on an earnings rate of 5% this means that a couple could have over $637,500 in each of their names and not pay any tax. But be careful as if you are investing in growth assets then triggering capital gains in the future may mean exceeding these thresholds whereas within the SMSF the CGT on pension assets is NIL and 10-15% in accumulation.

Also, consider the tax position if you are likely:

to receive an inheritance

large capital gain on an asset he’d outside super

to have one partner live significantly longer (they may end up with large amounts outside the super system)

WARNING

Please note that the SAPTO rate is based on the rebate income (rather than taxable income), which includes adjusted fringe benefits, total net investment loss and reportable super contributions.

The effective tax-free thresholds listed above for SAPTO recipients assume that the individual has no reportable super contributions, net investment losses or adjusted fringe benefits. However, this will not be the case where an individual has made salary sacrifice contributions or personal tax-deductible contributions (for example to reduce their taxable income to their effective tax-free threshold). Where they have, their rebate income will further reduce their SAPTO, and therefore their effective tax-free threshold will be lower.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in north west Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Corporate Authorised Representative of Viridian Advisory Pty Ltd ABN 34 605 438 042, AFSL 476223

This information has been prepared without taking into account your objectives, financial situation, or needs. Because of this, you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation, and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.