However, some people are still struggling with the process for implementing the option to release the funds from your SMSF. So here is a quick guide.

Firstly, Don’t ignore the notice or leave it aside to deal with later. You have 60 days to respond and if paying from your super then you must allow time to submit that election and have the ATO write to your fund with instructions to release the payment.

Complete election form online via MyGov

To complete an election form online you need to have registered for myGov and linked to the ATO Online Services.

If you are not already registered for myGov or your account is not linked to the ATO, go to online services.

If you are correctly linked to the ATO you should see the Australian Taxation Office listed under Your services when you log in to myGov. This is your starting point to make an election.

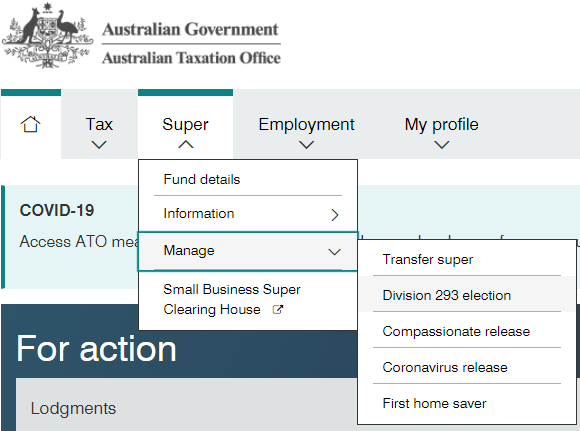

To make your election:

Login to myGov here myGov (make sure you have your mobile phone handy)

Click on the ATO image to access our ATO Online Services.

Select the Super tab from the top menu. (usually the second tab)

Scroll down to Manage and click on that to get sub-menu.

Click on Division 293 election (you may have other elections available – it is essential that you select Division 293 election).

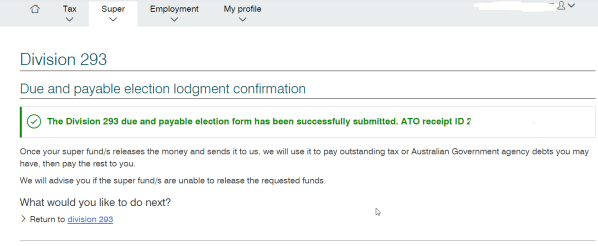

View your available elections. You may have elections for a due and payable account and/or a deferred account. You may also have elections available for different years.

Choose which super fund you want to pay the Div 293 Tax from (Your SMSF should be listed, if not contact your SMSF administrator).

Select your SMSF and complete the declaration and Lodge for the election that you would like to complete.

Then wait for the ATO to send you as trustee of your superfund a Notice to pay and remember this may go to your SMSF tax agent or administrator so drop them a quick email to let them know to expect it as you are still on a 60 day deadline!. Do not use the BPAY details on the form that came to you in your personal name

P.S. If you have suddenly discovered you have some other superannuation accounts DO NOT CONSOLIDATE. Check with your advisor first as you may lose insurances, tax deductions, or other benefits you were not aware of that cannot be replaced. Get the full details from the fund first.

Alternative – Complete paper form

If you are unable to complete your election online

Using ATO online services is the easiest and quickest way to make your election and will ensure there is no delay.

However, if you are unable to complete your election online, you have two options:

Speak to your tax agent, who can complete your Division 293 election for you using their Online services for agents.

Looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Please consider passing on this article to family or friends or your tax agent! Pay it forward!

Castle Hill: 40/8 Victoria Ave, Castle Hill NSW 2154

Windsor: Suite 4, 1 Dight St, Windsor NSW 2756

Corporate Authorised Representative of Viridian Advisory Pty Ltd ABN 34 605 438 042, AFSL 476223

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

OK, so here we are with only a few weeks left to the end of the financial year to get our SMSF in order and ensure we are making the most of the strategies available to us. Here is a checklist of the most important issues that you should address with your advisers before the year-end.

Its been a busy year and I have not had as much time as usual to put this together so if you find an error or have a strategy to add then please let me know. Links were working at the time of writing.

Warning before we begin,

Before we start, just a warning as in the rush to take advantage of new strategies you may have forgotten about how good you have it already Be careful not to allow your accountant, administrator or financial planner to reset any pension that has been grandfathered under the pension deeming rules that came in on Jan 1st 2015 without getting advice on the current and possible future consequences resulting in the pension being subject to current deeming rates if you lose the grandfathering. Point them to this document

It’s all about timing!

If you are making a contribution the funds must hit the Superfund’s bank account by the close of business on the 30th June. Careful of making contributions through Clearing houses as they often hold on to funds before presenting them to the individual’s superannuation fund for 7-30 days and it’s when the fund receives the payment that the contribution is counted except if paid via the government’s Small Business Clearing House. Pension payments must leave the account by the close of business unless paid by cheque in which case the cheques must be presented within a few days of the EOFY and there must have been sufficient funds in the bank account to support the payment of the cheques on June 30th. Get you payments in by Friday 26th or earlier to be sure (yes I’m Irish).

Review Your Concessional Contributions options – 25K per year up to 65 this year but work test from 1 July 2020 will apply to 67.

The big news is the government have changed the contribution rules from 1 July 2020 to extend the ability to make contributions from age 65 up to age 67. Read more here. Maximise contributions up to concessional contribution cap but do not exceed your Concession Limit. The sting has been taken out of Excess contributions tax but you don’t need additional paperwork to sort out the problem. So check employer contributions on normal pay and bonuses, salary sacrifice and premiums for insurance in super as they may all be included in the limit.

3. If your Super balance on 1 July 2019 was under $500,000 Review your previous Concessional Contributions (CC) and consider using the ‘Carry forward’ concessional contributions cap

Broadly, the carry forward rule allows individuals to make additional CC in a financial year by utilising unused CC cap amounts from up to five previous financial years, providing their total superannuation balance just before the start of that financial year was less than $500,000.

This measure applies from 2018-19 so effectively, this means an individual can make up to $50,000 of CC in a single financial year by utilising unapplied unused CC caps since 1 July 2018 and going forward from up to five previous financial years.

Prior to these amendments, if an individual did not fully utilise their annual CC cap in a financial year, they could not carry forward the unused cap to a later year. But please note the balance refers to $500,000 across all of your Superannuation accounts.

Review plans for Non-Concessional Contributions (NCC) options

From 1 July 2020 the new age limit of 67 will apply to Non-Concessional Contributions (NCC) without meeting the work test so you have the option of making $100,000 NCC per year up to turning 67.

Hopefully this month (tabled for 18th June 2020 sitting) the Parliament will also pass legislation allowing you to also use the “3 year bring forward rule” up to age 67.

So people who turned 64 0r 65 this year and who planned to use the “3 year bring forward rule” may want to review that strategy if they wish to get more money in to super

Current Option if turned 65 in 2019-20 FY: NCC of $100,000 or $300,000

Have you considered making non-concessional contributions to move investments in to super and out of your personal, company or trust name. Maybe you have proceeds from and inheritance or sale of a property sitting in cash.

As shares and cash have been hit by the Covod-19 crisis value you may find that it is opportune for personal tax reasons to take this time to move some assets to super may help control your tax bill.

Co-Contribution

Check your eligibility for the co-contribution and if you are eligible take advantage. Note that the limits have changed and it is “free incentive money to save for your retirement” – grab it if you are eligible.

To calculate the super co-contribution you could be eligible to receive based on your income and personal super contributions, use the Super co-contribution calculator.

Spouse Contribution

If your spouse has assessable income plus reportable fringe benefits totalling less than $37,000 for the full $540 tax offset and up to $40,000 for a partial offset, then consider making a spouse contribution. Check out the ATO guidance here

Over 65 and soon up to 67? Do you meet the work test? (The 40 hours in any 30 days rule)

You should review your ability to make contributions as if you if you have reached age 65 you must pass the work test of 40 hours in any 30 day period during the financial year, in order to continue to make contributions to super. Check out ATO superannuation contribution guidance . Keep an eye later this month for new of the age limit rising form 65 to 67 before needing to meet the work test from 1 July 2020.

Check any payments you may have made on behalf of the fund.

It is important that you check for amounts that may form a superannuation contribution in accordance with TR 2010/1 (ask your advisor), such as expenses paid for on behalf of the fund, debt forgiveness or in-specie contributions, insurance premiums for cover via super paid from outside the fund.

Notice of intent to claim a deduction for contributions

If you intend to start a pension this notice must be made before you commence the pension. Many like to start pension in June and avoid having to take a minimum pension but make sure you have claimed your tax deduction first. The same applies if you plan to take a lump sum withdrawal from your fund. GET THE NOTICE OF INTENT IN FIRST

Contributions Splitting to your spouse

Consider splitting contributions with your spouse, especially if:

your family has one main income earner with a substantially higher balance or

• if there is an age difference where you can get funds into pension phase earlier or

• If you can improve your eligibility for concession cards or age pension by retaining funds in superannuation in the younger spouse’s name.

This is a simple no-cost strategy I recommend everyone look at. See my blog about this strategy here.

Off Market Share Transfers (selling shares from your own name to your fund)

If you want to move any personal shareholdings into super you should act early. The contract is only valid once the broker receives a fully valid transfer form not before so timing in June is critical.

Pension Payments – so many more options this year 2019-2020 and in 2020-2021

If you are in pension phase, the government have brought in the Temporary Reduction in Minimum Pensions as part of the Covid-19 response. So please ensure you take the new minimum pension of at least 50% of your age-based rate below. For transition to retirement pensions, ensure you have not taken more than 10% of your opening account balance this financial year.

The following table shows the minimum percentage factor (indicative only) for each age group.

Minimum annual payments for super income streams for 2019/20 and 2020/21 Financial years.

Age at 1 July

Standard

Minimum % withdrawal

50% reduced

minimum pension

Under 65

4%

2%

65–74

5%

2.5%

75–79

6%

3%

80–84

7%

3.5%

85–89

9%

4.5%

90–94

11%

5.5%

95 or older

14%

7%

FINER DETAILS with TIPS and TRAPS

Here is some of the finer detail on how these measures will work, along with some tips and traps to consider when taking withdrawals for the rest of this financial year and the full 2020-21 financial year:

The measures are forward looking so if a pension member has already taken your minimum pension for the year then they cannot change the payment for this year but they can get organised for 2020/21. So, no you can’t try to sneak a payment back in to the SMSF bank account!

If a pension member has already taken pensions payments of equal to or greater than the 50% reduced minimum amount, they are not required to take any further pension payments before 30 June 2020. For example, many would have taken quarterly or half yearly payments. If they add up to the 50% reduced minimum then you do not need to take anymore payments this financial year.

If you still need your pension payments for living expenses but have already taken the 50% reduced minimum then, it may be a good strategy for amounts above the 50% reduced minimum to be treated as either:

a partial lump commutation sum rather than as a pension payment. This would create a debit against the pension members transfer balance account (TBA). Please discuss this with your accountant and adviser asap as some funds will have to report this quarterly and others on an annual basis. OR

for those with both pension and accumulation accounts to take the excess as a lump sum from the accumulation account balance to preserve as much in tax exempt pension phase as possible going forward to future years.

Think about having a sacrificial lamb, a second lower value pension that can sacrificed if minimum not taken. In this way if you pay only a small amount less than the minimum you only have to lose the smaller pensions concession rather than the concession on your full balance. When combined with the ATO relief discussed in the following article “What-happens-if-i-don’t-take-the-minimum-pension” you will have a buffer for mistakes.

Before reading the above: Be careful not to reset a pension that has been grandfathered under the new deeming of pension rules that came in on Jan 1st 2015 without getting advice.

Reversionary Pension is often the preferred option to pass funds to a spouse or dependent child. Review your options

A reversionary pension to you spouse will provide them with up to 12 months to get their financials affairs organised before having to make a final decision on how to manage your death benefit.

You should review your pension documentation and check if you have nominated a reversionary pension. If not, consider your family situation and options to have a reversionary pension.

This is especially important with blended families and children from previous marriages that may contest your current spouse’s rights to your assets. Also consider reversionary pensions for dependent disabled children. T

The reversionary pension has become more important with the application of the $1.6m Transfer Balance Cap limit to pension phase.

Review Capital Gains Tax Position of each investment

Review any capital gains made during the year and over the term you have held the asset and consider disposing of investments with unrealised losses to offset the gains made. If in pension phase then consider triggering some capital gains regularly to avoid building up an unrealised gain that may be at risk to government changes in legislation like those proposed this year.

Review and Update the Investment Strategy not forgetting to include Insurance of Members

Review your investment strategy and ensure all investments have been made in accordance with it, and the SMSF trust deed. Also, make sure your investment strategy has been updated to include consideration of insurances for members. See my article of this subject here. Don’t know what to do…..call us.

Collate and Document records of all asset movements and decisions

Ensure all the funds activities have been appropriately documented with minutes, and that all copies of all statements and schedules are on file for your accountant/administrator and auditor.

Double Dipping! June Contributions Deductible this year but can be allocated across 2 years.

For those who may have a large taxable income this year (large bonus or property sale) and are expecting a lower taxable next year you should consider a contribution allocation strategy to maximise deductions for the current financial year. This strategy is also known as a “Contributions Reserving” strategy but the ATO are not fans of Reserves so best to avoid that wording! Just call is an Allocated Contributions Holding Account.

Market Valuations – Now required annually

Regulations now require assets to be valued at market value each year, ensure that you have re-valued assets such as property and collectibles. Here is my article on valuations of SMSF investments in Private Trusts and Private Companies. For more information refer to ATO’s publication Valuation guidelines for SMSFs.

In-House Assets

If your fund has any investments in in-house assets you must make sure that at all times the market value of these investments is less than 5% of the value of the fund. Do not take this rule lightly as the new SMSF penalty powers will make it easier for the ATO to apply administrative penalties (fines) for smaller misdemeanours ranging from $820 to $10,200 per breach pere trustee.

Covid-Relief – The ATO has responded to current market conditions, and has announced it will not take compliance action against SMSFs where:

at 30 June 2020 the market value of an SMSF’s in-house assets is over 5% because of the downturn in the share market

the trustee of the SMSF prepares a rectification plan

by 30 June 2021, the rectification plan either:

cannot be effectively implemented because of market conditions

does not need to be implemented because the market recovers and the 5% test is again satisfied at 30 June 2021.

Is your fund providing Covid-19 Rent Relief to a property tenant whether a related party or not? Get your documentation in place.

If you have provided Rent Relief to a tenant, related or not, then get it documented now before June 30 that you have considered, managed and documented the request, the reasoning behind the Trustee’s decision and the details of the relief provided

The ATO have thankfully provided a non-binding practical approach of broadly not applying resources to this issue for FY2020 and FY2021. However, this announcement, while positive, should not be relied on given the considerable downside risks.

Careful if replacing TPD Insurance (Total Permanent Disability – basically “never work again” insurance)

Have you reviewed your insurances inside and outside of super? Don’t forget to check your current TPD policies owned by the fund with an own occupation definition as the rules changed a few years ago so be careful about replacing an existing policy as you may not be able to obtain this same cover inside super again.

Check the ownership details of all SMSF Investments

Make sure the assets of the fund are held in the name of the trustees on behalf of the fund and that means all of them. Check carefully any online accounts you may have set up without checking the exact ownership details. You have to ensure all SMSF assets are kept separate from your other assets.

Review Estate Planning and Loss of Mental Capacity Strategies.

Review any Binding Death Benefit Nominations (BDBN) to ensure they are valid (check the wording matches that required by the Trust Deed) and still in accordance with your wishes. Also ensure you have appropriate Enduring Power of Attorney’s (EPOA) in place allow someone to step in to your place as Trustee in the event of illness, mental incapacity or death. Do you know what your Deed says on the subject? Did you know you cannot leave money to Step-Children via a BDBN if their birth-parent has pre-deceased you?

Review any SMSF Loans

Have you provided special terms (low or no interest rates , capitalisation of interest etc.) on a related party loan? Then you need to review your loan agreement and get advice to see if you need to amend your loan. Have you made all the payments on your internal or third-party loans, have you looked at options on prepaying interest or fixing the rates while low. Have you made sure all payments in regards to Limited Recourse Borrowing Arrangements (LRBA) for the year were made through the SMSF Trustee? If you bought a property using borrowing, has the Holding Trust been stamped by your state’s Office of State Revenue. Please review my blog on the ATO’s Safe Harbour rules for Related Party Loans here

Still have Collectibles in your fund?

Play by the new rules that came into place on the 1st of July 2016 or get them out of your SMSF. More on these rules and what you must do in a good blog from SuperFund Partners here.

SuperStream obligations must be met

For super funds that receive employer contributions it’s important to take note that since 2014 the ATO has been gradually introducing SuperStream, a system whereby super contributions data is received and made electronically.

All funds should be able to receive contributions electronically and you should obtain an Electronic Service Address (ESA) to receive contribution information. If you are not sure if your fund has an ESA, contact your fund’s administrator, accountant or your bank for assistance.

If you change jobs your new employers may ask SMSF members for their ESA, ABN and bank account details. Some employers may also ask for your Unique Superfund Identifier (USI) – for SMSFs this is the ABN of the fund.

Don’t leave it until after 30 June, review your Self Managed Super Fund now and seek advice if in doubt about any matter.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Even the most seasoned SMSF Trustees and members realise that they need to be on top of their game over the coming 12 months. If you are running your own SMSF or your better half is doing so, then drag yourself and them along to the SMSF Association’s SMSF & Investor Event. Let the experts guide you.

Full disclosure, I am a board member of the SMSF Association and I do want as many people as possible to come along and boost their knowledge and be prepared for what the budget and possible new future government will throw at us. I have also bargained for a deal for you and if you use the coupon code “SMSFCoach” when registering you will be able to attend for FREE

So what is on the agenda:

Following the Federal Budget and leading up to the end of the financial year, hear from key SMSF and investment experts on crucial factors you as a trustee or your clients if you’re a n SMSF professional,, should be thinking about in regards to your fund/your clients’ funds. The program will feature:

A Special Address on the impact of the removal of franking credit refunds on SMSFs

Your SMSF Update – what’s new in self managed super

End of Financial Year – review your investment portfolio in light of political and investment markets

Peter Hogan our SMSF Education expert will discuss Everything you need to know about starting and receiving pensions – whether you are starting to think about moving into retirement or already earning a pension this session will cover everything you need to know especially as it relates to the Transfer Balance Cap.

And more to be announced soon…

WHERE & WHEN

Date: Tuesday 9 April 2019

Time: 8:15am – 3:30pm (including lunch and morning tea)

Register here using the coupon code ‘SMSFCoach’ for Free

(I confirm that I receive no commissions, fees or incentives for promoting this event and will not receive any of your private information)

SHOUT OUT TO SMSF PROFESSIONALS

If you are a SMSF Accountant, Auditor or Financial Planner then please pass on this opportunity to your clients as we need SMSF Trustees to be more knowledgeable than ever. Understand that ASIC now expects you to be providing education to your clients and you must find cost effective ways of doing this. Why not leverage of your association membership and provide your clients with access to this event or maybe even come along with a group of them.

If you are in Victoria don’t feel left out we will be coming to Melbourne too in June!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

The ATO has recently redesigned the Division 293 notice to provide information clearly and concisely. This includes providing the full assessment calculation to make it easier for people to understand how their tax has been calculated. This will also make it easier to identify any erroneous assessments due to incorrect reporting of information

Julie Steed, Senior Technical Services Manager of Australian Executor Trustees Part of the IOOF group, has kindly provided a refresher on the Division 293 tax and a review of the newly redesigned ATO notice that can be seen here: Div 293 notice of assessment

Division 293 tax

From 1 July 2017, the income threshold above which individuals pay an additional 15% tax on certain superannuation contributions reduced from $300,000 to $250,000. In December 2018 the ATO began issuing over 90,000 Division 293 notices for the 2017/18 income year. It is estimated that approximately 125,000 individuals will receive a Division 293 notice in the 2025FY.

Importantly, there are no strategies that can be used to reduce an individual’s liability for Division 293 tax. However, understanding the options that are available and how the Division 293 notice process works will assist individuals who receive a notice.

Overview

People with Division 293 income greater than $250,000 will pay 15 per cent additional tax on certain superannuation contributions. The tax is a personal tax rather than a tax deducted from super contributions by a fund. However, individuals may elect to release funds from super to pay the tax (see the Choices section below).

Division 293 income

Division 293 income includes:

taxable income

reportable fringe benefits

total net investment losses.

Ad-hoc income

Individuals who are not generally high income earners may still be liable for Division 293 tax if they receive certain one-off payments during a year. Such payments include eligible termination payments, the taxable component of a superannuation death benefit and capital gains.

However, the taxable component of a super lump sum benefit (other than a death benefit) is not included where:

it is received by individuals from preservation age to age 59

it is up to the current low rate cap of $205,000.

Division 293 contributions

Division 293 contributions include:

employer contributions

personal deductible contributions

contributions for a defined benefit interest (valued by an actuary)

employer contributions (including salary sacrifice) to a constitutionally protected fund.

The additional tax does not apply to:

excess concessional contributions

non-concessional contributions

contributions to certain Government funds for senior personnel, unless they are salary sacrifice contributions

contributions for certain Judges to defined benefit funds.

Calculation of Division 293 tax

Division 293 tax is 15% of the lesser of:

the amount of the Division 293 contributions

the amount of Division 293 income and Division 293 contributions above the $250,000 threshold.

Case study

Ryan has the following Division 293 details:

Division 293 income

$240,000

Division 293 contributions

$20,000

Total

$260,000

Division 293 tax is payable on $10,000, being the lesser of:

$20,000

$260,000 – $250,000 = $10,000

The Division 293 tax amount is 15% x $10,000 = $1,500

Division 293 notice

The ATO issues an Additional tax on concessional contributions (Division 293) notice to individuals which specifies the additional amount of tax that is payable and the due date for payment.

The ATO has recently redesigned the Division 293 notice to provide information clearly and concisely. This includes providing the full assessment calculation to make it easier for people to understand how their tax has been calculated. This will also make it easier to identify any erroneous assessments due to incorrect reporting of information.

The notice will also explain how to avoid interest charges, view statements of accounts online and the process for disagreeing with the assessment.

Choices

When an individual receives a Division 293 assessment they can choose to pay the tax from their personal resources. Alternatively, they can elect to have the amount released from their super fund to pay the tax. The time frame for making the election is 60 days. However, this may be a greater time frame than the date upon which payment of the tax is due.

The election can be made to release the tax amount from any super fund (other than some defined benefit funds). There is no requirement for the release to be made from the fund that received the contributions.

Release authority

If an election to have the amount released from super is made, the ATO will send the super fund a release authority and the fund will make the payment to the ATO. Funds are required to make the payment within 10 business days from the date the release authority is issued by the ATO.

Importantly a fund must not release an amount until they have received the ATO release authority. This requirement is sometimes misunderstood by SMSF trustees.

Conclusion

Understanding the choices available and the process involved in paying Division 293 tax can assist in ensuring that any tax payable is completed in a manner most appropriate to an individual’s circumstances.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why not contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Corporate Authorised Representative of Viridian Advisory Pty Ltd ABN 34 605 438 042, AFSL 476223

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Over this last week I have read so many politically biased responses to Bill Shorten’s proposed strategy to stop the refunds of franking credits that I despaired and I know it is going to be a political football rather than part of comprehensive tax reform. Then I came across a really well explained and positioned argument from Scott Phillips of The Motley Fool fame that takes the politics out of the analysis. I immediately reached out to Scott and asked him could I re-post it for my readers who may be finding the debate confusing or hard to explain to others. So here goes:

Why Bill Shorten is wrong — and right — on dividends

Scott Phillips

What’s that? Bill Shorten has announced a new policy on the refund of franking credits?

I hadn’t noticed.

Okay, that’s not true. I noticed. And, based on feedback on Twitter over the last week, many of you noticed, too.

If Shorten wanted to stir a hornet’s nest, he got just that. Maybe it’s clever politics. Maybe the focus groups told the pollsters this was a smart political strategy.

It sure as heck isn’t good policy, in my view.

Before you fire off an email to either abuse me or suggest I be knighted, let me explain.

I’m going to start with three premises that I think most people can agree on:

The tax system should be fair

You shouldn’t have to pay tax twice on dividend income; and

The tax system, as it stands, is broken.

That last point seems to be Shorten’s main thrust. And it’s a battle cry taken up by many partisans:

“We have a problem, and I have a solution. If you don’t like my solution, you’re saying we don’t have a problem.”

To which I reply:

“We absolutely have a problem. But your solution is a poor one. There are better ways to skin this cat.”

And before we go any further, please leave your political affiliations at the door. This week, on Twitter, I have bagged and praised Labor for different policies. I’ve done the same in the past to the Libs. If you can’t put aside your team jersey and engage in a discussion of ideas, then there’s not much for you in what follows.

But if you’re interested in good policy, read on.

Bill Shorten’s policy, as announced, goes something like this:

“We’re happy for you to reduce your tax using franking credits, but we’re not going to give you a refund.”

There are a few problems with that approach:

First, it implies that if you pay tax, you’re welcome to use the credits to reduce your tax burden to zero.

Second, those credits somehow magically are worthless once you hit zero, meaning that to me they’re worth something, but to a retiree in a 0% tax bracket, they’re worth nothing.

How can franking credits be worth different amounts to different people in different circumstances? Search me… I’m buggered if I know.

And third, and this is what’s stirred up most heat among those who have gone into bat for the policy:

“I pay tax and my taxes shouldn’t go to give a refund/handout to people who already have a lot of money.”

Now, don’t get me wrong. I think the current situation — regarding the ability to pay exactly zero tax on certain income in retirement that might be up to $80,000 — is crackers.

But, Shorten’s policy doesn’t fix that problem. Here’s why:

Consider three people, all of whom have SMSFs in pension phase, and who — according to the current tax rules — pay 0% tax: Banking Betty, Rental Richard and Dividend Davina.

Banking Betty deposits $100,000, and earns $2,000 each year in interest. Betty doesn’t pay any tax.

Rental Richard has a $100,000 property that pays him $2,000 each year in rent. Richard doesn’t pay any tax.

Dividend Davina buys $100,000 worth of shares that earned a profit of $2,000. The company paid tax of $600, so Davina gets $1,400. Davina doesn’t pay any tax.

See the difference here? Because Davina’s investment is in the form of shares in a company, she gets less than the other two. Even though she’s not supposed to pay any tax, the company paid tax, so she gets less.

Under current rules, she’d get the $600 back, delivering on the current government policy of a 0% tax rate, and equalising the return for each of those investors.

Bill Shorten, in effect, is penalising people for owning shares.

Now, let’s address the elephant in the room. Yes, because the company has already paid tax on that $2,000, Davina does officially get a refund. And the optics of that are bad: it looks like somehow the taxpayer is subsidising Davina.

But it’s all a question of cash flows and timing. The ATO just gives Davina back the money the company paid in tax.

And remember, a company is just a legal structure to organise your ownership interest in an asset. Shares in a company aren’t all that different in effect to accounts at a bank. Your bank account is evidence that you have a claim to a share of that bank’s assets, even if you don’t know specifically which notes you deposited.

Imagine a scenario under which Banking Betty’s bank withholds 30% of her interest and sends it to the government as tax. And where Rental Richard’s property manager is obligated to send 30% of his rental income to the ATO.

Both of these investors would have to fill out a tax return and the ATO would send them a refund — because tax was paid on their income, even though the tax rate should have been 0%.

Would Bill Shorten stop Betty and Richard getting their money back?

I doubt it.

But somehow, because Labor has (unfortunately, disingenuously) used extreme examples to make their point, and because they’ve dressed it up as a handout, they’ve mischaracterised the situation.

Somehow Dividend Davina is a fatcat living high on the hog, while Betty and Richard are perfectly entitled to pay no tax.

Essentially, because of the asset class they decide to invest in, our three protagonists are being treated differently.

Sound fair to you?

No, me neither.

Yes, the idea of a ‘refund’ for someone who has paid no tax feels, somehow, deeply wrong. But it’s because tax was paid by the company, on behalf of a shareholder who shouldn’t be paying tax, so the ATO is essentially just righting that wrong.

Still with me? Excellent!

Still fuming that well-off people pay no tax? Me too.

What? Didn’t I just spend 984 words (don’t waste time counting them. I checked) defending those people?

Well, yes. And no.

Here’s where both parties are engaging in a phony war of words. And we’re poorer for it.

Having an essentially uncapped income at a 0% tax rate is madness.

Yes, yes, it’s not technically uncapped, for a host of reasons. So let’s say $80,000 among friends.

You and I pay a decent slug of tax on an $80,000 income. And there’s no reason that a well-off retiree should be able to draw a completely untaxed income of a similar amount, when they likely have a very decent asset base — say a home and a seven-figure superannuation balance.

It’s simply not sustainable, especially as more boomers retire, to have that slice of the economic income pie remain completely untaxed.

But — and this is important — that doesn’t mean we should simply ban franking credit refunds and assume that fixes the problem.

Let’s go back to our alliterative actors, Betty, Richard and Davina.

If Betty was earning $80,000 in interest, should that be untaxed? Should Richard’s $80,000 in rent be untouched by the taxman? Should Davina’s $80,000 in dividends remain completely unscathed?

I don’t think so. But again, it’s not a question of the source of the income; it’s the size.

Under Bill Shorten’s plan, Davina would be worse off, but Betty and Richard laugh all the way to the bank. Does anyone, seriously, think that’s a good basis for a tax plan?

I didn’t think so.

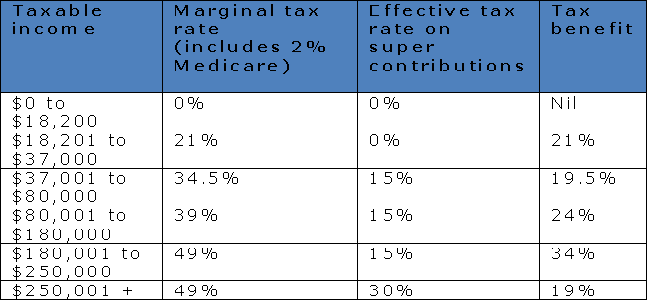

Here’s what I’d do: I’d have a generous tax-free threshold for income from superannuation, maybe $10,000 or so above the pension level. It’s not unreasonable that you’re allowed a little extra, given the sacrifice you made to save for your retirement.

But above that level, I’d implement a progressive tax scale not unlike the one that applies to regular income: The more you earn, the higher your marginal tax rate.

Simple, no?

Fair, yes?

That way, the tax code doesn’t discriminate on the basis of the asset class. There are no free lunches. And the unsustainable tax situation that currently applies to Super is fixed.

So Bill Shorten, and Chris Bowen, it’s time to admit defeat and go back to the drawing board. Feel free to use my template, above.

And Scott Morrison and Malcolm Turnbull, please stop with the emotive and negative language and grandstanding.

Politics should be a battle of ideas, not soundbites The best idea, well explained, should win, regardless of political party or ideological affiliation.

And, ladies and gentlemen of the Parliament, the Australian people will give you bonus points for explaining it clearly and for anything that reduces the complexity of our tax affairs, while ensuring fairness.

Indeed, Turnbull and Morrison’s political forebear, John Howard spoke to the National Press Club in 2014 when he shared the stage with former Labor PM, Bob Hawke. At that event, according to the Sydney Morning Herald , Howard said

“We have sometimes lost the capacity to respect the ability of the Australian people to absorb a detailed argument. They will respond to an argument for change and reform [but] they want two requirements. They want to be satisfied it’s in the national interest, because they have a deep sense of nationalism and patriotism. They also want to be satisfied it’s fundamentally fair.”

I’d like to think that’s still true.

I agree with Bill Shorten’s characterisation of the problem. I disagree completely with his solution.

I imagine I lost the most partisan readers — of both stripes — a few minutes ago. If you’re still reading, thank you for engaging in a discussion of ideas.

I hope I’ve convinced some of you. Of those I haven’t convinced, I hope I’ve at least done a decent job of addressing the issue, without bias, grandstanding or misdirection. Thanks for reading.

At the very least, I hope I’ve productively added to the conversation. It’s the least each of us can do.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

1 July 2017 was a major date when it comes to SMSF changes and accurate valuations are key to compliance with many of the changes. Unsure of what the valuation guidelines are for your self-managed superannuation fund (SMSF)? I have compiled a guide on what you need to know about asset valuation as SMSFs are now required to use market value reporting for all their financial accounts and statements. For Financial Year 2019, getting the value right is more important than ever, especially with the impact of the new super changes. Getting it wrong may impact on the fund’s compliance and whether you can make non-concessional contributions or commence a pension.

What is the market value of an asset?

“Market value” means the amount that a willing buyer of the asset could reasonably be expected to pay to acquire the asset from a willing seller if the following assumptions were made:

• the buyer and the seller dealt with each other at arm’s length in relation to the sale

• the sale occurred after proper marketing of the asset, and

• the buyer and the seller acted knowledgeably and prudentially in relation to the sale.

How do I go about determining market value?

For assets such as cash, term deposits, widely-held managed funds, ETFs and listed securities, these can be valued easily each year and should be valued at the end of each financial year. It is typically easy for trustees to value shares, managed funds and other listed investments because they can obtain daily valuations online. Here are a few links that may be helpful for historic share prices or for companies that have been delisted from the exchange.

DeListed carries historical share prices for many listed and delisted companies at this website, including prices for the former names of such companies. The prices go back as far as 1986 in some cases and include to mid-year 2009.

SMSFs with real estate, exotic assets or investments in private companies or trusts will require additional work from auditors. from an appropriately qualified person, such as an independent registered valuer or real estate agent.

The following guide provides an outline of what is required to help in valuing fund investments where market values are not readily available.

Real estate / Property valuations

Property needs to be valued at market value every year at 30 June, but the ATO does not require SMSF trustees to undertake an external valuation for all assets each year but is recommended at least every 3 years. For instance, assets such as real property may not need an annual valuation unless a significant event (i.e. natural disaster, market volatility, macroeconomic events or changes to the character of the asset) occurred that has created the need to review the most recent valuation.. Valuation of real estate can be undertaken by anyone, including the trustee(s), if suitably qualified, as long as it is based on objective and supportable data.

The following would generally be considered adequate audit evidence:

Real estate agent valuation (appraisal letter which they back up with comparable sales or listed properties)

Formal valuation from a qualified and independent valuer (compulsory if for commercial properties leased to related parties)

Valuation from trustees (with evidence of market valuation such as recent sales or online valuations). We recommend at least a comparison with values of 4-6 comparable properties if doing it yourself.

The latest cost-effective option is valuations from online real estate services like RPData can be used so ask your Administrator if they have access to this service.

Is the rent at commercial terms?

The fund’s auditor may also request evidence to show the rental income received by the fund is paid on commercial terms, such as

Annual Rental Income & Expenses Schedule from your real estate management agent covering the lease of the property during the year. Some charge $30-$50 for this but if you say it is offered free on your other properties you can squeeze them!

Rental appraisal by an independent real estate agent (for related party transactions)

Supporting evidence such as For Rent listing or tenants notice to end contract and an explanation from the trustees if no rental income was received during the year

Units in unlisted trusts or shares in unlisted companies

It can sometimes be tricky to obtain reliable audit evidence to support the value of unlisted investments. The company or trust may not be required to value their assets at market value and trustees must consider the value of the assets held by the entity. For example, where the trust or company holds property, any value should be based on the guidelines for real estate outlined above. Sometimes the other owners (individuals. companies or family trusts) in the trust do not require the same degree of scrutiny and can refuse to incur the extra costs to to suit the SMSF requirements. You will need to work around this issue with your fund sometimes picking up the expense.

Another consideration is that unlisted entities may not be required to get their financial statements independently audited, which make them less reliable from an audit perspective.

The following would generally be considered adequate audit evidence:

Audited financial statements of the entity

A share/unit price based on recent sales or purchases of the shares or units

Financial statements of the entity, with evidence that the underlying asset is valued at market value recently.

Independent valuation of the underlying assets of the entity

Loans to related and non-related parties

Firstly your fund is not meant to lend money to a fund member or relative of the member under any circumstances. Read here for more detail. Is your SMSF lending money to someone?

When your fund makes a loan to another entity or individual not related to a member then the loan agreement will specify the terms and conditions of the loan, including payment terms, interest on the loan and whether the loan it is secured or unsecured.

The market value of a loan is determined by its recoverability which could be:

Evidence of repayment of the loan (if applicable)

Details on the financial position of the borrower confirming their ability to repay (e.g. net asset position, sources of cash)

Details and value of security held as collateral for the loan (if applicable)

Collectables and personal use assets

In the case of collectables and personal use assets, the valuer should be a current member of a relevant professional body or trade association such as the Australian Antique and Art Dealers Association, the Auctioneers and Valuers Association of Australia and the National Council of Jewellery Valuers. Collectable and personal use assets cover items such as artwork, memorabilia, collectable coins and bank notes, wine and vintage cars. Metals such as gold and silver are only considered collectable items if their value exceeds the value of the metal based on its weight.

Bullion

If a trustee holds bullion at a storage facility or at the mint the documentation provided by these places will act as proof of the holding to the auditor.

If trustees choose to store their bullion at home or their business premises the auditor will require a resolution as at 30 June of each year which confirms the following;

• Inventory listing of the type(s) and quantities of metal held.

• Confirmation the asset is stored securely and not available for personal use by the members.

• Confirmation that the metal(s) are insured for the correct value.

Valuation in this format is less costly than holding in the form of a collectible. The market value can easily be verified to live spot prices which are readily available on a number of Bullion dealers’ websites.

Who needs this information

Your administrator or accountants needs this information to complete the annual accounts. Apart from preparing your annual accounts, you will also need to value assets:

if your fund has investment dealings with, or sells assets to, a related party

if you need to determine the percentage of in-house assets in your fund

on the commencement day of a pension

if your fund transfers a collectable or personal use asset to a related party – in this case the valuation must be done by a qualified independent valuer.

So who’s watching me?

Your fund’s independent auditor (your accountant may hide this person fairly well in the background but you should make yourself know to them and make it a team relationship not an adversary one). It is their responsibility to be making checks as to whether the annual financial statements properly reflect the market value based on objective and supportable evidence. they may request you get further evidence if not satisfied and they can issue a qualified audit opinion. Any qualified opinion will be reported by the auditor to the ATO.

On assessing the auditor’s report if the ATO is not satisfied that the assets are not recorded at market value in the fund’s financial accounts a fine of 10 penalty units (currently $2,100) per trustee can be imposed.

ATO Valuation guidelines for self-managed superannuation funds

The ATO provides guidelines here on their website to assist SMSF trustees when valuing assets for superannuation purposes.

For SMSF members affected by the $1.6m transfer balance cap, an appropriate valuation is also essential for FY 2016/17 to determine whether the member’s pension balance(s) may exceed the cap and for purposes of the CGT cost base reset.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

With all the talk about Total Super Balance caps and where people will invest money going forward if they can’t get it in to superannuation, the spotlight is being shone on “trusts” at present. This has also brought with it the claims of tax avoidance or tax minimisation, so what exactly are trusts and are there differences between Family Trusts, Units Trusts, Discretionary Trusts and Testamentary Trusts to name a few.

Trusts are a common strategy and this article aims to aid a better understanding of how a trust works, the role and obligations of a trustee, the accounting and income tax implications and some of the advantages and pitfalls. Of course, there is no substitute for specialist legal, tax and accounting advice when a specific trust issue arises and the general information in this article needs to be understood within that context.

Introduction

Trusts are a fundamental element in the planning of business, investment and family financial affairs. There are many examples of how trusts figure in everyday transactions:

Cash management trusts and property trusts are used by many people for investment purposes

Joint ventures are frequently conducted via unit trusts

Money held in accounts for children may involve trust arrangements

Superannuation funds are trusts

Many businesses are operated through a trust structure

Executors of deceased estates act as trustees

There are charitable trusts, research trusts and trusts for animal welfare

Solicitors, real estate agents and accountants operate trust accounts

There are trustees in bankruptcy and trustees for debenture holders

Trusts are frequently used in family situations to protect assets and assist in tax planning.

Although trusts are common, they are often poorly understood.

What is a trust?

A frequently held, but erroneous view, is that a trust is a legal entity or person, like a company or an individual. But this is not true and is possibly the most misunderstood aspect of trusts.

A trust is not a separate legal entity. It is essentially a relationship that is recognised and enforced by the courts in the context of their “equitable” jurisdiction. Not all countries recognise the concept of a trust, which is an English invention. While the trust concept can trace its roots back centuries in England, many European countries have no natural concept of a trust, however, as a result of trade with countries which do recognise trusts their legal systems have had to devise ways of recognising them.

The nature of the relationship is critical to an understanding of the trust concept. In English law the common law courts recognised only the legal owner and their property, however, the equity courts were willing to recognise the rights of persons for whose benefit the legal holder may be holding the property.

Put simply, then, a trust is a relationship which exists where A holds property for the benefit of B. A is known as the trustee and is the legal owner of the property which is held on trust for the beneficiary B. The trustee can be an individual, group of individuals or a company. There can be more than one trustee and there can be more than one beneficiary. Where there is only one beneficiary the trustee and beneficiary must be different if the trust is to be valid.

The courts will very strictly enforce the nature of the trustee’s obligations to the beneficiaries so that, while the trustee is the legal owner of the relevant property, the property must be used only for the benefit of the beneficiaries. Trustees have what is known as a fiduciary duty towards beneficiaries and the courts will always enforce this duty rigorously.

The nature of the trustee’s duty is often misunderstood in the context of family trusts where the trustees and beneficiaries are not at arm’s length. For instance, one or more of the parents may be trustees and the children beneficiaries. The children have rights under the trust which can be enforced at law, although it is rare for this to occur.

Types of trusts

In general terms the following types of trusts are most frequently encountered in asset protection and investment contexts:

Fixed trusts

Unit trusts

Discretionary trusts – Family Trusts

Bare trusts

Hybrid trusts

Testamentary trusts

Superannuation trusts

Special Disability Trusts

Charitable Trusts

Trusts for Accommodation – Life Interests and Rights of Residence

A common issue with all trusts is access to income and capital. Depending on the type of trust that is used, a beneficiary may have different rights to income and capital. In a discretionary trust the rights to income and capital are usually completely at the discretion of the trustee who may decide to give one beneficiary capital and another income. This means that the beneficiary of such a trust cannot simply demand payment of income or capital. In a fixed trust the beneficiary may have fixed rights to income, capital or both.

Fixed trusts

In essence these are trusts where the trustee holds the trust assets for the benefit of specific beneficiaries in certain fixed proportions. In such a case the trustee does not have to exercise a discretion since each beneficiary is automatically entitled to his or her fixed share of the capital and income of the trust.

Unit trusts

These are generally fixed trusts where the beneficiaries and their respective interests are identified by their holding “units” much in the same way as shares are issued to shareholders of a company.

The beneficiaries are usually called unitholders. It is common for property, investment trusts (eg managed funds) and joint ventures to be structured as unit trusts. Beneficiaries can transfer their interests in the trust by transferring their units to a buyer.

There are no limits in terms of trust law on the number of units/unitholders, however, for tax purposes the tax treatment can vary depending on the size and activities of the trust.

Discretionary trusts – Family Trusts

These are often called “family trusts” because they are usually associated with tax planning and asset protection for a family group. In a discretionary trust the beneficiaries do not have any fixed interests in the trust income or its property but the trustee has a discretion to decide whether anyone will receive income and/or capital and, if so, how much.

For the purposes of trust law, a trustee of a discretionary trust could theoretically decide not to distribute any income or capital to a beneficiary, however, there are tax reasons why this course of action is usually not taken.

The attraction of a discretionary trust is that the trustee has greater control and flexibility over the disposition of assets and income since the nature of a beneficiary’s interest is that they only have a right to be considered by the trustee in the exercise of his or her discretion.

Bare trusts

A bare trust exists when there is only one trustee, one legally competent beneficiary, no specified obligations and the beneficiary has complete control of the trustee (or “nominee”). A common example of a bare trust is used within a self-managed fund to hold assets under a limited recourse borrowing arrangement.

Hybrid trusts

These are trusts which have both discretionary and fixed characteristics. The fixed entitlements to capital or income are dealt with via “special units” which the trustee has power to issue.

Testamentary trusts

As the name implies, these are trusts which only take effect upon the death of the testator. Normally, the terms of the trust are set out in the testator’s will and are often used when the testator wishes to provide for their children who have yet to reach adulthood or are handicapped.

Superannuation trusts

All superannuation funds in Australia operate as trusts. This includes self-managed superannuation funds.

The deed (or in some cases, specific acts of Parliament) establishes the basis of calculating each member’s entitlement, while the trustee will usually retain discretion concerning such matters as the fund’s investments and the selection of a death benefit beneficiary.

The Federal Government has legislated to establish certain standards that all complying superannuation funds must meet. For instance, the “preservation” conditions, under which a member’s benefit cannot be paid until a certain qualification has been reached (such as reaching age 65), are a notable example.

Special Disability Trusts

Special Disability Trusts allow a person to plan for the future care and accommodation needs of a loved one with a severe disability. Find out more in this Q & A about Special Disability Trusts.

Charitable Trusts

You may wish to provide long term income benefit to a charity by providing tax free income from your estate, rather than giving an immediate gift. This type of trust is effective if large amounts of money are involved and the purpose of the gift suits a long term benefit e.g. scholarships or medical research.

Trusts for Accommodation – Life Interests and Right of Residence

A Life Interest or Right of Residence can be set up to provide for accommodation for your beneficiary. They are often used so that a family member can have the right to live in the family home for as long as they wish. These trusts can be restrictive so it is particularly important to get professional advice in deciding whether such a trust is right for your situation.

Establishing a trust

Although a trust can be established without a written document, it is preferable to have a formal deed known as a declaration of trust or a deed of settlement. The declaration of trust involves an owner of property declaring themselves as trustee of that property for the benefit of the beneficiaries. The deed of settlement involves an owner of property transferring that property to a third person on condition that they hold the property on trust for the beneficiaries.

The person who transfers the property in a settlement is said to “settle” the property on the trustee and is called the “settlor”.

In practical terms, the original amount used to establish the trust is relatively small, often only $10 or so. More substantial assets or amounts of money are transferred or loaned to the trust after it has been established. The reason for this is to minimise stamp duty which is usually payable on the value of the property initially affected by the establishing deed.

The identity of the settlor is critical from a tax point of view and it should not generally be a person who is able to benefit under the trust, nor be a parent of a young beneficiary. Special rules in the tax law can affect such situations.

Also critical to the efficient operation of a trust is the role of the “appointor”. This role allows the named person or entity to appoint (and usually remove) the trustee, and for that reason, they are seen as the real controller of the trust. This role is generally unnecessary for small superannuation funds (those with fewer than five members) since legislation generally ensures that all members have to be trustees.

The trust fund

In principle, the trust fund can include any property at all – from cash to a huge factory, from shares to one contract, from operating a business to a single debt. Trust deeds usually have wide powers of investment, however, some deeds may prohibit certain forms of investment.

The critical point is that whatever the nature of the underlying assets, the trustee must deal with the assets having regard to the best interests of the beneficiaries. Failure to act in the best interests of the beneficiaries would result in a breach of trust which can give rise to an award of damages against the trustee.

A trustee must keep trust assets separate from the trustee’s own assets.

The trustee’s liabilities

A trustee is personally liable for the debts of the trust as the trust assets and liabilities are legally those of the trustee. For this reason if there are significant liabilities that could arise a limited liability (private) company is often used as trustee.

However, the trustee is entitled to use the trust assets to satisfy those liabilities as the trustee has a right of indemnity and a lien over them for this purpose.

This explains why the balance sheet of a corporate trustee will show the trust liabilities on the credit side and the right of indemnity as a company asset on the debit side. In the case of a discretionary trust it is usually thought that the trust liabilities cannot generally be pursued against the beneficiaries’ personal assets, but this may not be the case with a fixed or unit trust.

Powers and duties of a trustee

A trustee must act in the best interests of beneficiaries and must avoid conflicts of interest. The trustee deed will set out in detail what the trustee can invest in, the businesses the trustee can carry on and so on. The trustee must exercise powers in accordance with the deed and this is why deeds tend to be lengthy and complex so that the trustee has maximum flexibility.

Who can be a trustee?

Any legally competent person, including a company, can act as a trustee. Two or more entities can be trustees of the same trust.

A company can act as trustee (provided that its constitution allows it) and can therefore assist with limited liability, perpetual succession (the company does not “die”) and other advantages. The company’s directors control the activities of the trust. Trustees’ decisions should be the subject of formal minutes, especially in the case of important matters such as beneficiaries’ entitlements under a discretionary trust.

Trust legislation

All states and territories of Australia have their own legislation which provides for the basic powers and responsibilities of trustees. This legislation does not apply to complying superannuation funds (since the Federal legislation overrides state legislation in that area), nor will it apply to any other trust to the extent the trust deed is intended to exclude the operation of that legislation. It will usually apply to bare trusts, for example, since there is no trust deed, and it will apply where a trust deed is silent on specific matters which are relevant to the trust – for example, the legislation will prescribe certain investment powers and limits for the trustee if the deed does not exclude them.

Income tax and capital gains tax issues

Because a trust is not a person, its income is not taxed like that of an individual or company unless it is a corporate, public or trading trusts as defined in the Income Tax Assessment Act 1936. In essence the tax treatment of the trust income depends on who is and is not entitled to the income as at midnight on 30 June each year.

If all or part of the trust’s net income for tax purposes is paid or belongs to an ordinary beneficiary, it will be taxed in their hands like any other income. If a beneficiary who is entitled to the net income is under a “legal disability” (such as an infant), the income will be taxed to the trustee at the relevant individual rates.

Income to which no beneficiary is “presently entitled” will generally be taxed at highest marginal tax rate and for this reason it is important to ensure that the relevant decisions are made as soon as possible after 30 June each year and certainly within 2 months of the end of the year. The two month “period of grace” is particularly relevant for trusts which operate businesses as they will not have finalised their accounts by 30 June. In the case of discretionary trusts, if this is done the overall amount of tax can be minimised by allocating income to beneficiaries who pay a relatively low rate of tax.

The concept of “present entitlement” involves the idea that the beneficiary could demand immediate payment of their entitlement.

It is important to note that a company which is a trustee of a trust is not subject to company tax on the trust income it has responsibility for administering.

In relation to capital gains tax (CGT), a trust which holds an asset for at least 12 months is generally eligible for the 50% capital gains tax concession on capital gains that are made. This discount effectively “flows” through to beneficiaries who are individuals. A corporate beneficiary does not get the benefit of the 50% discount. Trusts that are used in a business rather than an investment context may also be entitled to additional tax concessions under the small business CGT concessions.

Since the late 1990s discretionary trusts and small unit trusts have been affected by a number of highly technical measures which affect the treatment of franking credits and tax losses. This is an area where specialist tax advice is essential.

Why a trust and which kind?

Apart from any tax benefits that might be associated with a trust, there are also benefits that can arise from the flexibility that a trust affords in responding to changed circumstances.

A trust can give some protection from creditors and is able to accommodate an employer/employee relationship. In family matters, the flexibility, control and limited liability aspects combined with potential tax savings, make discretionary trusts very popular.

In arm’s length commercial ventures, however, the parties prefer fixed proportions to flexibility and generally opt for a unit trust structure, but the possible loss of limited liability through this structure commonly warrants the use of a corporate entity as unitholder ie a company or a corporate trustee of a discretionary trust.

There are strengths and weaknesses associated with trusts and it is important for clients to understand what they are and how the trust will evolve with changed circumstances.

Trusts which incur losses

One of the most fundamental things to understand about trusts is that losses are “trapped” in the trust. This means that the trust cannot distribute the loss to a beneficiary to use at a personal level. This is an important issue for businesses operated through discretionary or unit trusts.

Establishment procedures

The following procedures apply to a trust established by settlement (the most common form of trust):

Decide on Appointors and back-up Appointors as they are the ultimate controllers of the trust. They appoint and change Trustees.

Settlor determined to establish a trust (should never be anyone who could become a beneficiary)

Select the trustee. If the trustee is a company, form the company.

Settlor makes a gift of money or other property to the trustee and executes the trust deed. (Pin $10 to the front of the register is the most common way of doing this)

Apply for ABN and TFN to allow you open a trust bank account

Establish books of account and statutory records and comply with relevant stamp duty requirements (Hint: Get your Accountant to do this)

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Client Question : My next question is about the threshold income level at which my wife and I will start to pay personal tax in 2017-18. I read “about $28,000” in the paper the other day for my situation (age >65), but my wife does not turn 65 until 2018, so her tax-free level may be different. It would be useful to know these numbers in the case we decide to take some lump sums out of super because of the new limits. We are considering investing some money tax-free in our personal names, free of SMSF red tape.

Personal Tax-free Thresholds

The amount you can earn before you have to pay tax, actually depends on your age.

Under 65

For those people under age 65, the effective tax-free threshold is currently $20,542. How do we calculate this amount? Well, if you look at the ATO’s current Individual income tax rate table, you pay no tax on the first $18,200 you earn in a year.

However, you also get the benefit of the full low income tax offset if you earn below $37,000. That means the tax office will offset up to $445 from the tax you would normally have to pay. So you can earn another couple of thousand dollars before you have to pay tax.

How much can I earn before paying taxes after age 65

For those who have reached age pension age, they can earn even more without paying tax. If you are over 65, you get access to the Seniors and Pensioners Tax Offset (SAPTO). This reduces or eliminates the tax that would normally be liable to pay on some additional income

Using the SAPTO benefit, the amount you can earn each year as a pensioner before having to pay tax, is:

$32,279 for single people,

$28,974 each for members of a couple or $57,948 combined.

The beauty of this benefit is that for clients in SMSF Pension phase any income drawn from a super fund income stream once over 60 is tax-free and non-assessable, meaning it doesn’t count towards the above thresholds.

Based on an earnings rate of 5% this means that a couple could have over $500,000 in each of their names and not pay any tax. But be careful as if you are investing in growth assets then triggering capital gains in the future may mean exceeding these thresholds where as within the SMSF the CGT on pension assets is NIL and 10-15% in accumulation.

Also consider the tax position if you are likely:

to receive an inheritance

large capital gain on an asset he’d outside super

to have one parter live significantly longer (they may end up with large amounts outside the super system)

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Tax free Image courtesy of Stuart Miles /FreeDigitalPhotos.net

I found this excellent article on LinkedIn and and re-blogging it here for your guidance.