The ATO have released the analysis of the SMSF sector based on the financial returns for 30 June 2015 and some 2016 figures from their records. It’s always good to understand how the sector is developing and how your SMSF compares in the overall scheme of things. In this article I cherry-pick some of the stats that may be of interest to you.

Number of new SMSFs setup each year rising again.

The SMSF sector continues to grow with another up tick in 2015-6 after a slow down in 2014 and 2015.

One of the stats that still defies the belief of most SMSF Specialist Advisors is the number of funds being set up with Individual Trustees. In all our interaction with professional advisors over 90% recommend Corporate Trustees but the ATO stats on new setups show continued preference, over 90%, for Individual Trustees. When you are finished this blog I would urge readers to look at my earlier blog Why Self Managed Super Funds Should Have A Corporate Trustee (click now an it will open in another tab for reading later)

SMSF trustee type

This table shows the trustee structure (either corporate or individual trustees) of the SMSF population as at 30 June 2016, plus new registrations for the years 30 June 2014 to 30 June 2016.

SMSF trustee type

Trustee

type |

% of all SMSFs (at 30/06/16) |

2014 registrations |

2015 registrations |

2016 registrations |

| Corporate |

23.23% |

2,813 (7.70%) |

1,781 (5.45%) |

2,433 (7.24%) |

| Individual |

76.77% |

33,718 (92.30%) |

30,916 (94.55%) |

31,183 (92.76%) |

| Total |

100% |

36,531 (100%) |

32,697 (100%) |

33,616 (100%) |

Size of SMSF sector

SMSFs make up 99.6% of the number of funds and 29% of the $2.1 trillion total superannuation assets as at 30 June 2016.

SMSFs make up 99.6% of the number of funds and 29% of the $2.1 trillion total superannuation assets as at 30 June 2016.

There were 577,000 SMSFs holding $622 billion in assets, with more than one million SMSF members.

Over the five years to 30 June 2016, growth in the number of SMSFs averaged almost 6% annually.

45% of SMSFs have been established for more than 10 years, and 17% have been established for three years or less.

Growth of SMSF assets

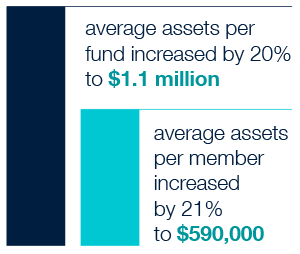

In 2015, the average assets of SMSFs reached $1.1 million, a growth of 20% over five years. Average assets per member were $590,000, the highest over five years.

In 2015, the average assets of SMSFs reached $1.1 million, a growth of 20% over five years.

Average assets per member were $590,000, the highest over five years.

For SMSFs established in 2015, the average fund assets were $392,000, an increase of 15% compared to average assets of funds established in 2011.

48% of SMSFs had assets between $200,000 and $1 million, accounting for 23% of all SMSF assets.

The majority of SMSF assets were held by funds with assets between $1 million and $5 million, representing 54% of total SMSF assets.

Contributions

Total contributions to SMSFs increased by 38% over the five years to 2015. This is 6% higher than the growth of total contributions to all superannuation funds (32%) over the same period.

Member contributions increased to more than $26 billion or by 54% over the five-year period.

Employer contributions made to SMSFs fell by 0.5% over the five years to 2015.

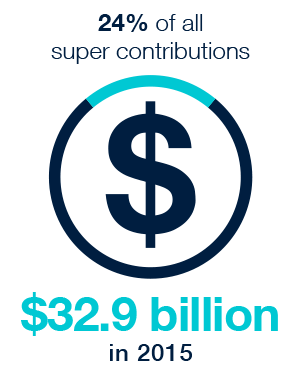

The Graph below compares contributions to SMSFs as a proportion of all super fund contributions for the years ended 30 June 2011 to 30 June 2015.

At 30 June 2015, contributions to SMSFs represented 24% of all super fund contributions. Member contributions into SMSFs, accounted for 51% of all member contributions across all super funds in 2015, an increase of 2% over the five-year period. In contrast, the proportion of employer contributions to SMSFs has dropped over the period to only 8% of all employer contributions across all super funds in 2015.

Graph 3: Contributions to SMSFs as a percentage of total Australian super contributions (for member, employer, and total) 2011–2015

SMSF benefit payments

Benefit payments have increased from $19.2 billion in 2011 to $35 billion in 2015. The proportion of SMSF members receiving a benefit payment also increased by 24% in 2015.

In 2015 the average benefit payment per fund was $126,000, and the median payment $62,900.

In 2015, 94% of all benefit payments were in the form of income stream (including transition to retirement income streams).

Transition to retirement income streams have remained steady representing 12% of total benefit payments in 2015.

SMSF payment phase

The majority of SMSFs continued to be solely in the accumulation phase (52%) with the remaining 48% making pension payments to some of or all members.

The majority of SMSFs continued to be solely in the accumulation phase (52%) with the remaining 48% making pension payments to some of or all members.

Over the five years to 2015, there was a shift of funds moving into the pension phase (7%).

Of SMSFs that started to make pension payments in 2015, 50% were more than five years old, while 23% were less than two years old.

Of funds established over the last 10 years to 2015, 69% have not started making pension payments.

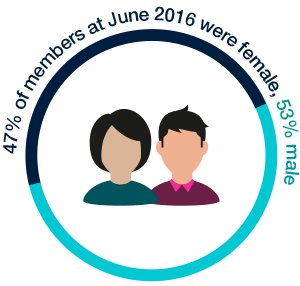

SMSF member demographics

SMSF member demographics

At 30 June 2016 there were almost 1.1 million SMSF members, of whom 53% were male and 47% female

The trend continued for members of new SMSFs to be from younger age groups. With the median age of SMSF members of newly established funds in 2015 decreased to 48 years, compared to 59 years for all SMSF members as at 30 June 2016.

In 2015, SMSF members tended to be older than members of APRA funds and had both higher average balances and higher average taxable incomes.

The proportion of members receiving pension payments from an SMSF continued to trend upwards. In 2015, 41% of members were fully or partially in pension phase, compared to 34% in 2011

SMSF member balances

At 30 June 2015 the average SMSF member balance was $590,000 and the median balance was $355,000, an increase of 21% and 26% respectively over the five years to 2015.

The average member balances for female and male members were $498,000 and $633,000 respectively. The female average member balance increased by 24% over the five-year period, while the male average member balance increased by 17% over the same period.

Over the five years to 2015, the proportion of members with balances of $200,000 or less decreased to 31% of all members.

Graph : Asset size SMSF and SMSF member 2011–2015

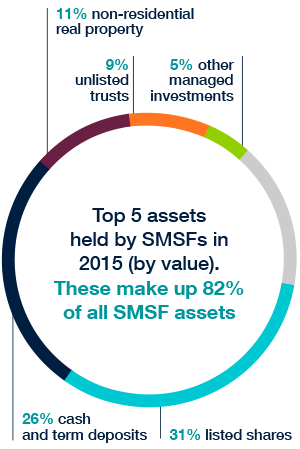

SMSF asset allocation

SMSFs directly invested 81% of their assets, mainly in cash and term deposits and Australian-listed shares (a total of 57%).

For the third consecutive year the proportion of total assets held in cash and term deposits decreased slightly (by 2%).

As fund asset size increased, the proportion of assets held in cash and term deposits decreased significantly while the proportion of assets held in trusts and other managed investments increased.

SMSFs in the pension phase had similar assets to SMSFs in the accumulation phase. The only noticeable differences are that SMSFs in pension phase tend to slightly favour listed shares and managed investments more, while those in accumulation phase favoured property assets more.

Limited recourse borrowing arrangement (LRBA) assets

In 2015, 6% of SMSFs reported assets held under LRBAs, which is consistent with the prior year (5.7%). The majority of these funds held LRBA investments in residential real property and non-residential real property. In terms of value, real property assets held under LRBAs collectively made up 91% or $18.5 billion of all SMSF LRBA asset holdings in 2015.

SMSF borrowing

At 30 June 2015, SMSFs held total borrowings of $16.9 billion representing 2.8% of total SMSF assets. The average amount borrowed increased from $346,000 in 2011 to $378,000 in 2015.

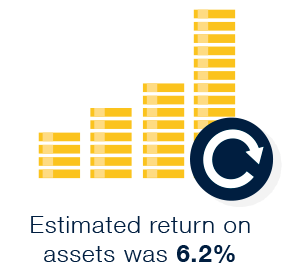

Investment performance

Investment performance

In 2014–15, estimated average return on assets for SMSFs was positive (6.2%), a decrease from the estimated returns in 2014 (of 9.7%), but remains in positive terms and is consistent with the trend of investment performance for APRA funds of more than four members over the five years to 2015.

SMSF expenses

The estimated average total expense ratio of SMSFs in 2015 was 1.1% and the average total expenses value was $12,200.

The average ‘investment expense’ and ‘administration and operating expense’ ratios were consistent at 0.60% and 0.50% respectively.

SMSFs in pension phase incurred higher average total expenses than funds solely in accumulation phase.

The average expense ratios for SMSFs declined in direct proportion to the increased size of the fund.

SMSF auditors

In 2015, there continued to be a trend towards SMSF Auditors performing audits for a larger number of SMSFs, with most (53%) performing between five and 50 SMSF audits, and 28% of auditors performing between 51 and 250 SMSF audits.

There were 5% of SMSF auditors conducting more than 250 audits, representing 44% of total SMSF audits in 2015

To see the full report in more detail click here https://www.ato.gov.au/about-ato/research-and-statistics/in-detail/super-statistics/smsf/self-managed-superannuation-funds–a-statistical-overview-2014-2015/?page=1#Introduction

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.