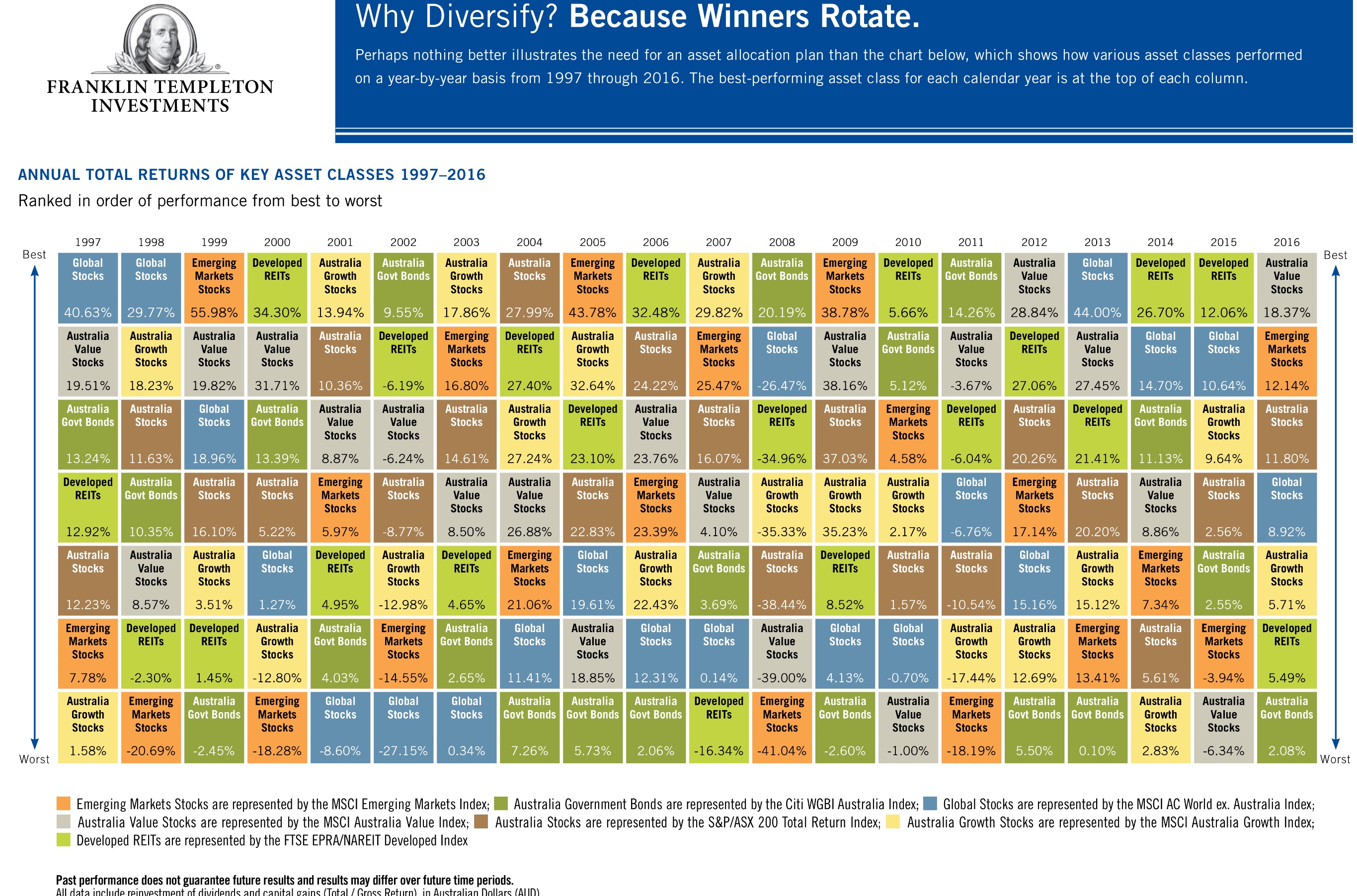

Do you know which asset sector performed best last year, the year before? Do you think those results will guide you for next year? Think again. I don’t think many SMSF Investors would have guessed Global Listed Property would have been the top performers in the last 6 years but in 2016 was a disappointing under performer. Many burnt in the property sector in the GFC had avoided it like the plague and missed some of the upside.

Franklin Templeton Austalia’s annual asset class ladder for 2018 is a great tool to visualise how each asset class/sector has performed over the last 20 years and pour water on ideas that we can reliably predict next years winners.

Click on this picture to access the larger version in PDF pormat

What becomes glaringly obvious after scrutinising the table is that no single asset class consistently outperforms the others. Just in case you subscribe to the ‘last years greyhound is this years dog” or that cycles are predictable, the table shows no clues or discernible pattern into how the previous year’s winners or losers will perform in the following year as the pattern appears totally random.

We coach clients to build a diversified strategy with some tactical allocations when sectors or assets appear oversold or opportunities arise like when the Aussie dollar was getting USD $1.10 a few years back and the opportunity came to overweight international stocks.

I hope this information has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

This is part of series on the necessary changes to strategies and opportunities that have resulted from the pending 1 July 2017 changes which will see earnings on transition to retirement (TTR) pensions subject to 15% tax in the fund.

I know this has created concerns with many trustees and advisers around the question of should you access the relief and if so how to actually access the CGT relief provisions. People want to know what factors they must take in to consideration.

Some of the concerns have been clarified by the ATO. One concern was that trustees would need to commute their TTR pensions and roll back into accumulation before 1 July to access the CGT relief provisions. Those relief provisions would allow the cost base of all or selected eligible assets to be reset to the current market value on a date chosen by the trustees between now and 30 June. This CGT relief allows trustees to in effect, retain the tax-free status of unrealised capital gains accumulated prior to 30 June 2017.

The newly issued ATO issued Law Companion Guideline (LCG) 2016/8 has provided some excellent clarification. If your SMSF is operating as an unsegregated fund, the LCG states that member will not need to commute back to accumulation phase to be able to elect to reset the cost base of assets the wish to elect to apply the CGT relief.

It is intended that the same basis should be available for segregated funds, but the ATO has indicated is still reviewing options for how to make this work in practice. I will try to keep this blog updated with any guidance from the ATO on this matter but please make sure you adviser/administrator is on top of these matters. An SMSF that only has TTR or account-based pensions (and no accumulation phase) is automatically classified as a segregated fund. However if you put in a new contribution, as many are, this year then that money goes in to accumulation and the fund becomes automatically unsegregated. So look at your contribution intentions.

All is not lost as the fund would still have been segregated until that contribution was made and you may elect for that date to be the new CGT cost base valuation date.

Conversations need to start with YOUR advisers and administrators to check whether:

you should to continue a TTR pension after 1 July 2017 or to commute back to accumulation phase.

you may have already or can trigger a further condition of release such as leaving any one employment position after age 60. To move from Accumulation or TTR to Account Based Pension

Why are TTR pensions still relevant and for whom

The tax advantages of a TTR pension will reduce when the earnings in the fund start to be taxed on 1 July, but advantages may still arise for members who:

Are over age 60 and can draw tax-free income from the TTR

Wish to start accessing super to top-up income or increase income to pay off debts

Want to be able to nominate an automatic reversionary for estate planning purposes

Can use salary sacrifice or personal deductions to contribute a higher net amount into super than they need to withdraw.

If the TTR pension is no longer required, care should be taken with the commutation and timing of the commutation to ensure the CGT relief provisions can be accessed on any assets they wish to claim the relief for.

Looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make 2016 the year to get organised or it will be 2026 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such

I knew with all the recent changes to Superannuation that many of my clients would need to update their SMSF Trust Deeds and started doing my research for a blog. Then I came across a recent blog from Dr.Brett Davies at Legal Consolidated today and I could not really improve on it. So with his permission, I am re-blogging his content here.

Self-Managed Super Fund (SMSF) Deeds previously required updates in:

– 1999 – ‘Excluded Funds’ became ‘Self-Managed Super Funds’, preservation & in-house assets

– 2007 – ‘Simpler Super’

– 2017 – Legislation passed in 2016, requires the changes below

The 15 changes to SMSF Deeds required after the 2016 Budget are to:

Internally ‘rollback’ pensions to accumulation;

Segregate assets between accumulation and pension phases;

Reject contributions;

Refund contributions;

Deal with excess transfer balance tax and excess non-concessional contributions;

Allow income streams and Account Based Pension (grandfathered);

Specify guardians for incapacity and death;

Identify the Power of Attorney when living overseas for more than 2 years;

Resettle pensions with flexible timing without mingling with accumulation account;

Allow reversionary beneficiary nominations;

Provide for CGT relief;

Deal with segregated and unsegregated assets;

Cease or keep Transition to Retirement Income Streams;

Calculate member balances, across different funds; and

Calculate internal pension rollbacks to accumulation.

These SMSF updates are all required to give maximum flexibility to your accountant and adviser.

Why does my SMSF Specialist Advisor / Accountant want to apply these SMSF updates?

Pre-2012 SMSF Deeds fail to deal with these 10 issues:

Removing clauses requiring the Trustee to do something that is no longer legal or beneficial;

Changing the sections that are ‘regimented’ with unnecessary rules vs being ‘permissive’. There is no point stating mandatory SIS requirements. In fact, it is dangerous to re-state legislation. This is because it dates your deed;

Accounting for an increased concessional contribution cap;

Removing insurance cover where the conditions are out of date;

Incorporating clauses about losing the pension at death or when the minimum payment has not been made;

Allowing for excess concessional contributions taxed at member’s marginal rate (-15% offset);

Updating the Investment Strategy to incorporate the ATO’s new Audit approach;

Changing market valuation clauses to leave the mechanism for the Accountant;

Allowing remuneration for non-trustee duties; and

Allowing non-lapsing Death Benefit Nominations.

Update your Deed to ensure your SMSF is compliant. Then you get the most out of your SMSF.

There is no risk of resettlement

‘Resettlement’ is when you create a new ‘trust estate’ out of an old trust. This applies to SMSFs and causes significant tax implications. However, there is no risk of resettlement under the High Court authority of Commercial Nominees (2010).

Updating your SMSF Deed through Legal Consolidated does not result in the resettlement of your SMSF. We retain the parts of the old Deed that are required by legislation and previous court decisions. But this does not affect a resettlement.

Make sure to check your with your own current deed provider or ask your adviser to check out Legal Consolidated’s offer.

Looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make 2016 the year to get organised or it will be 2026 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

OK, It has happened. I always worried that British pride and fear of immigration would lead to this outcome. So where to from here? What does it mean for SMSF Investors?

The situation is unprecedented and there is no verified or tested procedure for EU exit. This means there is uncertainty as to what happens next. You can expect that:

Article 50 of the EU constitution – the law governing the process of the UK’s divorce from the EU – will be triggered

This will kick-start the formal two-year process determining the terms of the UK’s EU exit, including the shape of its future access to the EU Single Market

There will be significant pressure on Prime Minister David Cameron to resign (Update: that has happened) and for Scotland to review its position within the UK

In the short run, Self Managed Superannuation Fund investors can expect:

Shock to investor confidence and increased asset price volatility primarily in the EU but also with Aussie companies who have exposure to that region especially the UK (BTT, CYBG, Henderson, HVN, IRESS)

This vote combined with global economic conditions, high asset valuations, our election next month and the progress towards the U.S. election in November will all likely contribute to volatility through the second half of the year.

Further strength in the Aussie Dollar short-term and declines in the pound (time to pay in advance for the UK trip of a lifetime!)

Downward pressure on equities, especially financial sector stocks and companies with overseas earnings. Time to buy the world at a discount. If not confident then look to great proven managers like Magellan and Platinum to pick the opportunities and ETFs from Vanguard, Ishares, State Street and Betashares for core or sector specific exposure.

Flight to safety will see USD and GOLD seen as safe havens. We can point you to the right people if interested in Bullion

Upward pressure on corporate bond yields owing to increased uncertainty and the worsening short term growth outlook – as with equities, the financial sector is most

exposed. Look to proven managers in this fixed interest and credit space like Vimal Gor at BT Investment Management to guide you.

Modest declines in-house prices are possible, as our banks may find it harder to raise overseas debt and therefore pass on increased costs to borrowers and hence curtail new purchases.

The leave vote will create short-term volatility and hurt growth prospects as markets deal with increased uncertainty. Inevitably however, the increased volatility should open up potential opportunities to benefit tactically through buying of those companies and assets that show solid traits of being well capitalised and with good management that should be able to best withstand the uncertainty. In a nutshell you will get a one-off opportunity to buy quality assets as a discount but you must search for quality among the chaff.

From time to time, as with the Greek debt Crisis, equity markets experience heightened, event-related volatility. A good adviser will ensure that you focus on your long-term goals and understand:

Volatility is a normal part of long-term investing and equity returns premium revolve around getting higher than cash returns for accepting that volatility.

Avoid being swayed by media hype and overly negative sentiment.

SMSF trustees and other long-term investors are usually rewarded for taking additional equity risk when there is “blood on the streets”

Market corrections can create attractive opportunities to buy quality assets at a discount. Afraid to pick sectors then use a multi-manager like Russell Investments to spread the risk

Some active investment can help navigation in periods of increased volatility. That is why we at Verante believe in passive/active blended portfolio design

So what to do?

Make sure you have some cash ready for purchases

Review your portfolio for any stocks or assets over exposed to Europe and seek research or comment on them

Wait for some sign of the market bottoming and take small and targeted purchases in discounted sectors without getting carried away.

Research , research and more research or outsource / work with SMSF specialist advisors like us who have made the contacts and done the leg work in portfolio design.

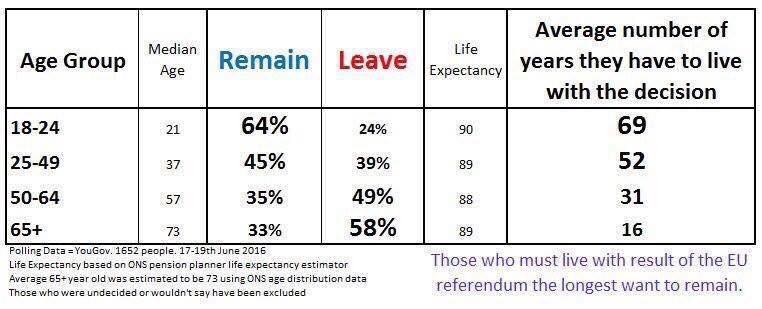

Finally a table that sums up the fact that those who have to live with this decision were against it.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Rate for 2025-26 Related Property LRBA is 8.95%and Listed Shares 10.95%

Old Rate for 2024-25 Related Property LRBA was 9.35% and Listed Shares 11.35%

The ATO have issued long-awaited guidelines providing SMSF trustees with suggested ‘Safe Harbour’ loan terms on which trustees may use to structure a related party Limited Recourse Borrowing Arrangement (LRBA) consistent with dealing at arm’s length with that related party.

By implementing these “Safe Harbour” loan terms, SMSF trustees are assured by the ATO Commissioner that

..for income tax purposes, the Commissioner accepts that an LRBA structured in accordance with this Guideline is consistent with an arm’s length dealing and that the NALI provisions do not apply purelybecause of the terms of the borrowing arrangement.

It is absolutely essential that all non-bank SMSF borrowing arrangements (LRBAs) be reviewed prior now extended to 1 Jan 2017

Where has this come from?

The ATO first released and then re-issued ATO Interpretative Decisions in 2015 (ATO ID 2015/27 and ATO ID 2015/28), dealing with Non-Arm’s Length Income(NALI) derived from listed shares and real property purchased by an SMSF under an LRBA involving a related party lender – where the terms of the loan were not deemed to be on commercial terms.

These ATOIDs state that the use of a non-arm’s length LRBA gives rise to NALI in the SMSF. Broadly, the rationale for this view is that the income derived from an investment that was purchased using a related party LRBA, where the terms of the loan are more favorable to the SMSF, is more than the income the fund would have derived if it had otherwise being dealing on an arm’s length basis.

NALI is taxed at the top marginal tax rate, currently 47% – regardless of whether the income is derived while the fund is in accumulation phase where tax is normally 15% or in pension phase when the income would usually be tax exempt.

After that bombshell, the ATO announced that it would not take proactive compliance action from a NALI perspective against an SMSF trustee where an existing non-commercial related party LRBA was already in place, as long as such an LRBA was brought onto commercial terms or wound up by 30 June 2016.

The Nitty Gritty Details of the Safe Harbour Steps

The ATO has issued Practical Compliance Guideline PCG 2016/5. As a result, provided an SMSF trustee follows these guidelines in good faith, they can be assured that (for income tax compliance purposes) their arrangement will be taken to be consistent with an arm’s length dealing.

The ‘Safe Harbour’ provisions are for any non-bank LRBA entered into before 30 June 2016, and also those that will be entered into after 30 June 2016.

Broadly, this PCG outlines two ‘Safe Harbours’. These Safe Harbours provide the terms on which SMSF trustees may structure their LRBAs. An LRBA structured in accordance with the relevant Safe Harbour will be deemed to be consistent with an arm’s length dealing and the NALI provisions will not apply due merely to of the terms of the borrowing arrangement.

The terms of the borrowing under the LRBA must be established and maintained throughout the duration of the LRBA in accordance with the guidelines provided.

Safe Harbour 1

Safe Harbour 2

Asset Type

Investment in Real Property

Investment in a collection of Listed Shares or Units

Interest RateNote: as of 10 Jan 2019: The RBA no longer round the rates to the nearest 5 basis points.

RBA Indicator Lending Rates for banks providing standard variable housing loans for investors. Use the May rate immediately preceding the tax year. (2015/16 year = 5.75%)(2016-17 year = 5.65%)(2017-18 year = 5.8%)(2018-19 year = 5.8%)(2019-2020 year = 5.94%)(2020-2021 year = 5.1%) (2021-2022 year = 5.1%)(2022-2023 year = 5.35%)2024 FY = 8.85% (2024-25 year = 9.35%) (2025-26 year 8.95%)

Same as Real Property + a margin of 2%

Fixed / Variable

Interest rate may be fixed or variable.

Interest rate may be fixed or variable.

Term of Loan

Variable interest rate loans:Original loan – 15 year maximum loan term (both residential and commercial).Re-financing – maximum loan term is 15 years less the duration(s) of any previous loan(s) in respect of the asset (for both residential and commercial).Fixed interest rate loan:

Rate may be fixed for a maximum period of 5 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 5.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 5 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

Variable interest rate loans:Original loan – 7 year maximum loan term.Re-financing – maximum loan term is 7 years less the duration(s) of any previous loan(s) in respect of the collection of assets.Fixed interest rate loan:

Rate may be fixed up to for a maximum period of 3 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 7 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 7.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 3 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan cannot exceed 7 years.

Loan-Value –RatioLVR

Maximum 70% LVR for both commercial & residential property. Total LVR of 70% if more than one loan.

Maximum 50% LVR.Total LVR of 50% if more than one loan.

Security

A registered mortgage over the property.

A registered charge/mortgage or similar security (that provides security for loans for such assets).

Personal Guarantee

Not required

Not required

Nature & frequency of repayments

Each repayment is to be both principal and interest.Repayments to be made monthly.

Each repayment is to be both principal and interest.Repayments to be made monthly.

Loan Agreement

A written and executed loan agreement is required.

A written and executed loan agreement is required.

Information sourced from Practical Compliance Guidelines PCG 2016/5.

Potential Trap to be aware of: Importantly, as part of this announcement, the ATO also indicated that the amount of principal and interest payments actually made with respect to a borrowing under an LRBA for the year ended 30 June 2016 must be in accordance with terms that are consistent with an arm’s length dealing.Information sourced from Practical Compliance Guidelines PCG 2016/5.

For the 2017-18 and 2018-19 years the rate is 5.8%

For the 2019-20 year the rate is 5.94%

For the 2020-21 year the rate is 5.1%

For the 2021-22 year the rate is 5.1%

For the 2022-23 year the rate is 5.35%

For the 2023-24 year the rate is 8.85%

For the 2024-25 year the rate is 9.35% until 30 June 2025

For the 2025-26 year the rate is 8.95%

For 2019-20 and later years, the rate published for May (the rate for the month of May immediately prior to the start of the relevant financial year)

It is the applicable rate under Column H of the above spreadsheet (click on link). The rate seems to have started in August 2015 but I assume we must use the May rate from now on.

In referencing the Indicator Rate you can use: Ref: Title: Lending rates; Housing loans; Banks; Variable; Standard; Investor Lending rates; Housing loans; Banks; Variable; Standard; Investor Frequency: Monthly Units: Per cent per annum Source RBA Publication Date 04-Apr-2016 Series ID: FILRHLBVSI

A complying SMSF borrowed money under an LRBA, using the funds to acquire commercial property valued at $500,000 on 1 July 2011.

The borrower is the SMSF trustee.

The lender is an SMSF member’s father (a related party).

A holding trust has been established, and the holding trust trustee is the legal owner of the property until the borrowing is repaid.

The loan has the following features:

the total amount borrowed is $500,000

the SMSF met all the costs associated with purchasing the property from existing fund assets.

the loan is interest free

the principal is repayable at the end of the term of the loan, but may be repaid earlier if the SMSF chooses to do so

the term of the loan is 25 years

the lender’s recourse against the SMSF is limited to the rights relating to the property held in the holding trust, and

the loan agreement is in writing.

We do not consider that this LRBA has been established or maintained on arm’s length terms. The income earned from the property, which is rented to an unrelated party, may give rise to NALI.

At 1 July 2015, the property was valued at $643,000, and the SMSF has not repaid any of the principal since the loan commenced.

If after considering TD 2016/16, it is determined that the income earned from the property is in fact NALI, to avoid having to report NALI for the 2015-16 year (and prior years) the Fund has a number of options.

Option 1 – Alter the terms of the loan to meet guidelines

The SMSF and the lender could alter the terms of the loan arrangement to meet Safe Harbour 1 (for real property).

To bring the terms of the loan into line with this Safe Harbour, the trustees of the SMSF must ensure that:

The 70% LVR is met (in this case, the value of the property at 1 July 2015 may be used).

Based on a property valuation of $643,000 at 1 July 2015, the maximum the SMSF can borrow is $450,100. The SMSF needs to repay $49,900 of principal as soon as practical before 30 June 2016.

The loan term cannot exceed 11 years from 1 July 2015.

The SMSF must recognise that the loan commenced 4 years earlier. An additional 11 years would not exceed the maximum 15 year term.

The SMSF can use a variable interest rate. Alternatively, it can alter the terms of the loan to use a fixed rate of interest for a period that ensures the total period for which the rate of interest is fixed does not exceed 5 years. The loan must convert to a variable interest rate loan at the end of the nominated period.

The interest rate of 5.75% applies for 2015-16 and 5.65% p.a. applies from 1 July 2016 to 30 June 2017. The SMSF trustee must determine and pay the appropriate amount of principal and interest payable for the year. This calculation must take the opening balance of $500,000, the remaining term of 11 years, and the timing of the capital repayment, into account.

After 1 July 2016, the new LRBA must continue under terms complying with the ATO’s guidelines relating to real property at all times.

For example, the SMSF must ensure that it updates the interest rate used for the loan on 1 July each year (if variable) or as appropriate (if fixed), and make monthly principal and interest repayments accordingly.

Option 2 – Refinance through a commercial lender

The fund could refinance the LRBA with a commercial lender, extinguish the original arrangement and pay the associated costs.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant part of the 2015-16 year.

Option 3 – Payout the LRBA

The SMSF may decide to repay the loan to the related party, and bring the LRBA to an end before 30 January 2017.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and the relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant period.

Each option will have many advantages and disadvantages – so it is important to understand what the practical implications of each option are, and how physically you will approach each option. Seek specialised advice on this matter as it is not a strategy suitable for DIY implementation

Important Note to 13.22C or Unrelated Unit Trust Investors

The guidelines provided in this PCG are not applicable to an SMSF LRBA involving an investment in an unlisted company or unit trust (e.g. where a related party LRBA has been entered into to acquire a collection of units in an unrelated private trust or a 13.22C compliant trust). As such, trustees who have entered into such an arrangement will have no option but to benchmark their particular loan arrangement based on commercial loan terms, or to bring the LRBA to an end.

Please visit out SMSF Property page to get details on all available strategies for SMSF property investors.

UPDATE (Relief for those caught by Budget measures)

In a letter to an industry association, the Treasurer, Scott Morrison, has outlined transitional arrangements to allow additional non-concessional contributions above the proposed lifetime limit in certain limited circumstances. Contributions made in the following circumstances may be permitted without causing a breach of the lifetime cap:

where the trustees of a self managed superannuation fund (SMSF) have entered into a contract to purchase an asset prior to 3 May 2016 that completes after this date and non-concessional contributions were planned to be made to complete the contract of sale. Non-concessional contributions will be permitted only to allow the contract to complete provided they are within the relevant non-concessional cap that was applicable prior to Budget night, and

where additional contributions are made in order to comply with the Australian Taxation Office’s (ATO) Practical Compliance Guideline (PCG) 2016/5 related to limited recourse borrowing arrangements, provided they are made prior to 31 January 2017.

Additional non-concessional contributions made under these proposed transitional arrangements will count towards the lifetime cap, but will not result in an excess.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Click here for appointment options.

Liam Shorte B.Bus FSSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 9899 3693, Mobile: 0413 936 299

PO Box 6002, Norwest NSW 2153

U40, 8 Victoria Ave., Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Recent swings in global currencies have brought exchange-rate risk back to the forefront for investors with overseas exposure in different currencies. Currency risks are risks that arise from changes in the relative valuation of different currencies. These changes can create unpredictable gains and losses when the profits or dividends from an investment are converted from a foreign currency back into Australian dollars.

Any investor who holds stocks, ETFs with the likes of iShares, Vanguard or SPDR or managed funds such as Magellan Global Fund in their SMSF portfolio that invest outside Australia will have some exposure to foreign currency, and where the Aussie dollar exchange rate goes will have an effect on these SMSF portfolios. For instance, a strengthening dollar could negatively impact foreign stock market returns and you should consider this risk in portfolio design.

Interest rates are critical, because when a country’s rate rises, in many cases, so does its currency. Or in our case if the US interest rate rises or at the moment is being held unexpectedly lower by the Us Federal Reserve, our currency’s exchange rate can fluctuate wildly in response to another government’s actions.

Up until recently, this wasn’t much of a worry for Australian investors. Rates were low, the Aussie dollar was getting weaker coming down fro its peak near $1.10 to the US$, and people made money by investing in foreign assets.

Going forward that may not be so easy so its is important for Self Managed Super Fund investors to understand currency exchange risk.

Here is a good video from Blackrock iShares explaining how currency exposure affects returns on international investments.

Now you should note you can also find Currency Hedged ETFs and Hedged Managed funds (as opposed to a Hedge Fund which is totally different) that can help you easily manage the effect of currency on your investments and can be paired with their unhedged counterparts to tailor currency risk while maintaining consistent equity exposure. Of course there is a cost to implementing this protection but that is what good portfolio risk management is all about.

Do you want some more education on why you should consider international investments as part of your SMSF portfolio? then please check out this previous blog about investing internationally via your SMSF.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Do you know which asset sector performed best last year, the year before? Do you think those results will guide you for next year? Think again. I don’t think many SMSF Investors would have guessed Australian Listed Property would have been the strongest in 3 out of the last 4 years but in 2016 was a disappointing underperformer. Many burnt in the property sector in the GFC had avoided it like the plague and missed some of the upside.

Franklin Templeton Austalia’s annual asset class ladder for 2016 is a great tool to visualise how each asset class/sector has performed over the last 20 years and pour water on ideas that we can reliably predict next years winners.

What becomes glaringly obvious after scrutinising the table is that no single asset class consistently outperforms the others. Just in case you subscribe to the ‘last years greyhound is this years dog” or that cycles are predictable, the table shows no clues or discernible pattern into how the previous year’s winners or losers will perform in the following year as the pattern appears totally random.

We coach clients to build a diversified strategy with some tactical allocations when sectors or assets appear oversold or opportunities arise like when the Aussie dollar was getting USD $1.10 a few years back and the opportunity came to overweight international stocks.

I hope this information has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

This guide has been requested by a number of our younger clients under 50 who are now taking an interest in retirement savings and tax planning but applies to all working SMSF members especially those who can combine Salary Sacrifice with a Transition to Retirement Pension. Please view this short ATO video on super contributions first and then we will go in to detail:

So what is salary sacrifice?

Salary sacrifice is an arrangement between an employer and an employee, whereby the employee agrees to forgo part of their future entitlement to salary or wages in return for the employer providing them with benefits of a similar value.

Contributions made through a Salary Sacrifice Arrangement (SSA) into super are made with pre-tax dollars, meaning they are not taxed at the member’s marginal tax rate.

They are treated as Concessional Contributions (CCs) and tax of up to 15% will usually be payable, so long as the member does not exceed their CC cap. Higher income earners may have CCs within the cap taxed at 30% (refer to our article Will you be paying the new top up tax on your SMSF contributions? )

The difference between your marginal tax rate and the tax rate on contributions is what makes up the benefit of salary sacrifice for the member of your fund. This has nothing to do with investments, it is just income planning and using the tax system legally to your advantage.

Unlike Superannuation Guarantee (SG) or other employer contributions required under an award or workplace agreement, there is no legislative time-frame specifying when salary sacrifice contributions must be made to superannuation. It’s recommended that a time-frame be specified in the SSA. This could be, for example:

at the same time as SG is paid, or

within three business days of being withheld from salary.

An SSA is only valid until the person turns age 75. Salary sacrifice contributions generally cannot be accepted by a super fund after 28 days from the end of the month in which the member turns 75. Only mandated employer contributions can be made for an employee age 75 or older (SIS Reg 7.04).

What makes a Salary Sacrifice Arrangement (SSA) valid?

There is no legal obligation for employers to offer salary sacrifice to employees. To be effective, only prospective earnings can be sacrificed. This means an SSA will only be valid if there is a prospective agreement in place before the employee has earned the entitlement to receive the relevant amount as salary and wages.

Remember, there is no requirement for an SSA to be in writing, nor is there a standard SSA. It is strongly recommended that a written agreement be in place which states the terms and conditions of that agreement. The ATO provides a detailed explanation in tax ruling TR 2001/10.

What forms of income can be salary sacrificed?

Salary or wages are the most common types of payments that are sacrificed into super. As only future entitlements can be sacrificed, an effective arrangement can’t be made for salary or wages that have already been earned.

This means payments to which an employee is already entitled to (such as earned salary and wages, accrued leave and bonuses or commissions already earned), cannot be salary sacrificed into super unless an effective arrangement was in place prior to the employee becoming entitled to that remuneration. For example, annual and long service leave paid on termination of employment can’t be sacrificed.

If an employee has entered into an SSA and takes leave during employment, the SSA is still effective and salary sacrifice amounts can still be directed to superannuation.

What are the tax implications?

Amounts salary sacrificed into super under an effective SSA are not ‘salary and wages’ in the hands of the employee. Accordingly, employers have no PAYG withholding liabilities in relation to the payment.

Although the super contributions are a benefit derived due to employment, it is specifically exempt from Fringe Benefits Tax (FBT). However, this doesn’t extend to salary sacrifice amounts into another person’s super account (eg a spouse).

Super contributions made under an effective SSA are considered employer contributions for the purposes of the Income Tax Assessment Act 1997 and are deductible to the employer.

Usually, an SSA favours taxpayers subject to the higher marginal tax rates, as they pay just 15% contributions tax on the amount sacrificed into super (or 30% for high income earners). See this ATO video below for a short explanation of the Division 293 Tax

However, for taxpayers with incomes under the 19%( + 2% Medicare) tax rate threshold (currently $37,000), the marginal rate is not markedly different to the 15% tax payable on contributions by the receiving super fund for the sacrificed contribution.

A minor saving can still be made of almost 6% as Medicare Levy (of up to 2%) is not payable on the amount sacrificed to super.

An alternative strategy for lower-income earners is to make personal after-tax contributions to obtain a Government co-contribution of up to $500. Note: Salary sacrificed employer contributions do not qualify for the Government’s co-contribution.

What are the Centrelink implications?

An amount of salary voluntarily sacrificed into super is still counted as income for Centrelink / social security purposes. Contributions are assessed as income where a person voluntarily sacrifices income into super and has the capacity to influence the size of the amount contributed or the way in which the contribution is made reduces their assessable income.

Super contributions that an employer is required to make under the SG Act, an award, a collective workplace agreement or the super fund’s rules are not assessed as income for the member.

What issues should be considered?

Employer or other limitations

It is not compulsory for an employer to allow salary sacrificing, including amounts to superannuation. The first step is for the member to know is if their employer permits salary sacrificing.

Also, even where allowed, the arrangement under which the person is employed may impose limitations. This could be terms in a workplace agreement or award.

For example, some awards specify that a certain level of an employee’s package must be paid as salary. This would effectively place a limit on the amount that could be sacrificed to superannuation

Super Guarantee payments

Salary sacrifice amounts are treated as employer contributions. An employer may decrease an employee’s SG contributions when taxable income is reduced through salary sacrifice.

This is because the minimum amount of SG an employer is required to pay is based on the employee’s Ordinary Time Earnings (OTE). As entering into an SSA reduces an employee’s OTE, it will reduce the amount of SG that an employer is required to pay.

It is also the case that a salary sacrificed amount, being an employer contribution, could meet some or all of employers SG obligations. SMSF members should negotiate with their employer that SG payments are maintained at pre-salary sacrifice levels and include this in the SSA.

Example

Malcolm’s salary and OTE is $105,000 pa. He enters into an effective SSA to forego $20,000 of his salary for additional employer super contributions. Malcolm’s salary/OTE reduces to $85,000 for SG purposes and his employer is only legally required to pay 9.5% on this amount.

Malcolm should have negotiated with his employer to maintain the SG based on his original salary and the salary sacrifice amounts are made in addition.

Entitlements upon ceasing employment

As outlined above, an SSA reduces the salary component of a person’s package. This may also reduce other entitlements when ceasing employment (through resignation or redundancy) such as:

leave loading

calculation of leave entitlements, and

calculation of redundancy payments.

Members of your SMSF should ensure that they understand the impact of entering into an SSA. Where possible, the agreement should ensure no reduction in benefits. However confirmation from the employer is necessary.

Timing of employer contributions

There are clear rules governing an employers’ legal obligation to pay its contributions to a complying super fund either monthly or quarterly.

There are no such rules governing an employer to make a pre-tax voluntary contribution/salary sacrifice contribution into an employee’s super fund when the employee requests it. This means an employer can pay this contribution whenever they want.

SMSF members should include in the SSA the frequency of salary sacrifice contributions to super (eg the same frequency as salary payments).

Reportable employer contributions

Reportable employer super contributions (RESC) including salary sacrifice, are counted as ‘income’ for many Government benefits and concessions, such as:

Government co-contributions

Senior Australians tax offset

Spouse contribution tax offset

10% rule for making personal deductible super contributions

Medicare Levy Surcharge

Family assistance benefits, and

Centrelink and DVA income tests.

RESCs are not added back when calculating the low-income tax offset and Medicare levy.

Termination payments

Long service leave and annual leave paid on termination cannot be salary sacrificed, unless an effective SSA was put in place prior to the leave being accrued.

If termination payments are based on a definition of salary that excludes employer superannuation contributions, the employer can effectively exclude the salary sacrifice amount from the total salary on which these entitlements would be calculated.

As a result, the employee’s termination package would be reduced. SMSF members should ensure that the SSA does not impact on other benefits and entitlements.

Contribution caps

An employer is eligible for a tax deduction for super contributions made on behalf of employees, regardless of the amount.

There is also no limit on the amount that an employee can sacrifice into super. However, salary sacrifice amounts are counted towards the employee’s CC cap. Excess CCs are taxed at the person’s marginal tax rate plus a charge. See the ATO video below for more details

This effectively limits the tax-effectiveness of salary sacrifice to superannuation to the employee’s annual CC cap.

At the beginning of the financial year, it’s critical to review your SMSF member’s existing SSA to ensure they won’t exceed their CC cap.

For example, if a member has received a pay rise, they may now be getting higher SG contributions from their employer. They may therefore need to reduce their salary sacrifice contributions to ensure they don’t breach their CC cap.

Ongoing reviews may also be necessary as the member may receive a pay rise during the financial year or elect to salary sacrifice a bonus which impacts on the total CCs. As well as if the concessional contribution cap increases in future years or the client becomes eligible to use the transitional higher CC cap. We recommend a April or May review of contributions to make sure your SMSF members are under their caps and will stay so up to June 30th.

Checklist

While salary sacrifice can be a tax-effective way for people to save for retirement, there are a number of steps that should be taken to ensure it is properly implemented. The following checklist could be used to help ensure all the key issues are addressed.

1.

Check that the employer permits salary sacrifice

2.

Check on limitations placed on an agreement by employment conditions (eg award, workplace agreement, etc)

3.

Ensure agreement is for future earnings and valid

4.

Ensure other employment entitlements are not impacted by agreement (eg SG,

5.

Check available concessional contribution cap and ensure client will not exceed the cap

6.

Establish the agreement in writing (including timing of contributions)

7.

Review agreement and level of contributions at least on an annual basis (around

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click on the Schedule now link to see some options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Information sourced and valid as of February 2015 from ATO, BT, MLC, Challenger, SIS Act.

There are many reasons to get a superannuation review especially if you are within 15 years of using your super funds more tax effectively (hint over age 45). A lot can be done to dramatically improve your retirement prospects given time. However if you leave it too late, the chances of making significant improvements are limited. Getting good financial advice can make all the difference to the quality of your retirement. You may not want a full advice service but you can just have a Superannuation and Insurance review. So here are a few reasons why a review could be one of the best decisions you make.

You’ve being putting money in to Super for over 20 years and not sure what it’s doing for you. You have more than one superannuation account and cannot keep a track of how them or how they are performing. Consolidating your accounts together could make keeping track of your savings much easier and moving house less of a hassle!

You may be considering adding funds or your tax agent may have recommended some salary sacrifice and you are suddenly more interested in getting value for money.

You may be interested and want to explore the use of a Self Managed Superannuation Fund known as a SMSF (its only one option but we can help you assess if it is right for you).

You may not be satisfied with the level of service and advice you are receiving from your superannuation company and/or your adviser if you are getting any at all. Many people receive no service at all but continue paying fees year after year. Is it time for you to step-up and demand advice, we invite clients for a review at least twice per year.

You are concerned that your super or multiple accounts may not be performing very well. Sadly, most people in superannuation schemes have little or no idea how their funds are invested or performing from one year to the next. Reports get thrown in a drawer because the jargon is mind bending!

You may be unsure how much risk you are taking with your superannuation investments. It is undeniable that in order to increase your nest egg value, some risk will need to be taken. However the risk you are taking may not be suitable for you and categories like “Balanced or Core” don’t actually mean what they suggest!.

And how about just getting general health check on your super and how it is performing.

Like many people you have accumulated lots of accounts over the years from various jobs ( I recently consolidated 12 accounts for a couple). It may be beneficial to consolidate them all together in one account (wait don’t rush in, review insurance and fees first).

Identify poor performing superannuation funds and move them to investments that have greater potential for growth or a more consistent return.

You may have an SMSF or Superannuation account sitting in cash and just don’t know what to do as you have lost confidence.

You may have multiple/duplicate insurance arrangements across many funds and be paying premiums for cover that may never pay out.

How a superannuation review works

You are likely to have one or more personal accounts and they could be an industry fund, an employer group plan, a personal retail account, or even a transition to retirement pension .

The first step is to complete a Risk Profiling Questionnaire; this is designed to help identify what your attitude to risk is and your comfort with different classes of investment.

The second step it to complete a Fact Find about your personal circumstances so that we have a full understanding of you current situation, your future goals and objectives.

The third step is to obtain full details of all of your current superannuation and insurance arrangements. We ask superannuation companies more than 15 questions, so that we get a full and complete picture of your current situation.

The fourth step is to complete a full and comprehensive analysis of your current arrangements, to identify if your super accounts are working as they should be, that insurance cover is valid and will protect you and your family and fees are under control.

Step five is to recommend a suitable investment strategy to move your Superannuation balance forward, should the review reveal that your existing accounts are not working as well as they should be.

Step six is to implement the recommendations, which may mean re-organising and consolidating your accounts into one super or even a pension fund.

And finally step seven is to keep your arrangements under regular review to ensure that it continues to perform and meet your objectives.

Want a Superannuation Review or are you just looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make this the year to get organised or it will be 2028 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

So you have a great idea to move some assets to your SMSF but you want to stay within the rules and keep your fund compliant. Then you hit the jargon associated with Superannuation rules and regulations.

You need to understand who are “related parties” of your SMSF for two reasons, to ensure compliance with the acquisition from a related party rules and to determine the in-house assets.

A related party is defined in the Superannuation Industry Supervision) Act 1993 known as the SIS Act. This is the bible when it comes to Superannuation so you should save that link above. Anyway in the SIS Act sec 10(1) a related party is defined as:

Fund member

Standard employer-sponsor of the fund or

Part 8 associate of a fund member or a part 8 associate of a standard employer-sponsor of the fund.

Ok the first one is easy. Any member including you yourself is a related party.

Standard Employer

A standard employer sponsor of a fund is an employer who contributes to the fund due to an agreement between the employer and the trustee of the fund. These were common in the early days of SMSFs but largely non-existent now.

Where an employer only contributes to a fund due to an agreement between the member and the employer such as under a salary sacrifice arrangement, they will not be considered a standard employer sponsor.

If an SMSF has a standard employer sponsor, which would be uncommon, the relationship will be noted either in the trust deed or in an attached schedule to the deed.

Part 8 associate

Now prepare for a headache to hit you hard after reading this one.

Part 8 associates are broken down in the legislation to Part 8 associates of individuals, companies and partnerships. However, if there is no standard employer sponsor, we only need to examine the part 8 associates of the members who will always be individuals.

The part 8 associates of a member are:

a relative of the member (parent, grandparent, brother, sister, uncle, aunt, nephew, niece, linear descendant or adopted child of the member or their spouse or a spouse of the aforementioned)

other members of the SMSF (a person who is not a member but acting as individual trustee or director under an Enduring Power of Attorney is not necessarily a Part 8 associate)

a partner of the member (legal partnership, not ‘business partners’ i.e. company directors) and their spouses and children

the trustee of a trust the member controls and

a company sufficiently influenced by, or in which majority voting interest is held by the member and their Part 8 associates either individually or together.

A member of the fund will be deemed to control a trust where the member and/or their part 8 associates are:

entitled to a fixed entitlement of more than 50 per cent of the capital of the trust,

entitled to a fixed entitlement of more than 50 per cent of the income of the trust,

able or accustomed (formally or informally) to direct the trustees to act in accordance with their directions or

able to appoint or remove trustees.

A company will be deemed to be controlled by a member where the directors are accustomed or under an obligation to act under the instructions of the member and/ or their Part 8 associates or the member and/ or their part 8 associates have more than 50 per cent of the voting rights.

OK, so I warned you to beware of the headache inducing nature of dealing with “Part 8 Associates”. Was I right or was I RIGHT!

The best advice I can give you is to get advice before transferring assets and ask for the advice and get that advice in writing so all parties are sure of the scenario and no mistakes are made.

Are you looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Whether you are a long-term investor or an opportunist, many investors find comfort in knowing that many others are investing the same way they are and they get caught up in the media hype on a certain sector. Think of the Dot Com craze in the late 90’s when many invested in this sector even though they did not understand it well and as prices rose even the hesitant among investors poured more money in for fear of missing out or FOMO as I prefer to term it. A good adviser should help you identify the risk of these fads and keep you well diversified.

Here is a good educational video from Franklin Templeton Investments on the subject.

I believe that you always need to do your own research on an investment and then cross check that with others. Be prepared to listen to those who may seem wacky, over optimistic or pessimistic before making your decisions. A good Self Managed Super Fund advisor should be able to get you a selection of research from different sources to stress test any investment.

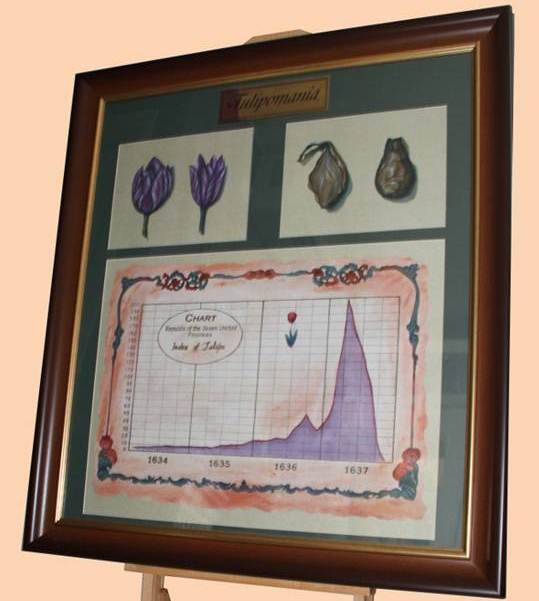

Bubble’s go back a long time, even centuries and while we are weary of each investment that crashes we rarely learn enough to avoid the next one. From my personal collection is one of my favourite prints called Gekko’s Tulip Mania which you may have seen in the movie Wall Street 2. I have it hanging on my office wall as a constant reminder! You can read more on this bubble at Wikipedia – Tulip Mania

“This is the greatest bubble story of all time… they call it the Tulip Mania.” – Gordon Gekko

For those looking for a truly Australian history of bubbles I would recommend reading a 2003 paper by the John Simon and published by the RBA available free online called Three Australian Asset-price Bubbles

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Years after the 2008 financial crisis and some people have been slow to regain confidence in the share markets and low cash and term deposit interest rates leave them cold. A growing number of people have considered shifting their superannuation to the more self- directed option of a self-managed superannuation fund (SMSF).

Small to Medium Business owners have always been at the forefront of adopting SMSFs and they have been particularly interested in this rapidly growing area for greater control of their superannuation savings and the flexibility of investments allowed in a SMSF structure. However the ability to either transfer their business premises into their SMSF via a contribution or sale, depending on their cash flow circumstances, has been attractive to many business owners.

Current legislation governing SMSFs, the SIS Act, allows a SMSF to acquire only three types of assets from the members or a related party. These assets are business real property, widely held managed funds and listed securities (shares).

Business real property is best defined as “any freehold or leasehold interest of the entity in real property where the real property is used wholly and exclusively in one or more businesses (whether carried on by the business or not).” This definition does not allow much leeway so you should seek professional advice to ensure that your property satisfies the requirements of the “wholly and exclusively” business use test and meets the definition of business real property prior to implementing this strategy

Benefits:

Release equity to build the business – you can access superannuation funds to help fund business growth prior to retirement by way of a cash purchase by the SMSF.

Tax minimisation – the property moves in to the concessionally taxed superannuation environment; 15% tax rate while members are in accumulation phase or exempt from tax when members are in pension phase.,

Asset Protection – to protect the value of the business real property in the event of bankruptcy, litigation or changes to your industry destroying your market.

Build funds for retirement – you have a bricks and mortar investment to boost your retirement funds earning market rent at concessional rates with the ability to avoid any CGT if sold later.

If you are seeking new premises then buying in your super fund allows you the security of tenure that comes with being your own landlord.

Helps in preparing a business for transfer or sale. If the new owner or family members cannot afford to buy the business and the property, you can sell the business premises and lease them the property.

Risks:

You should always ensure the strategy meets the Sole Purpose test of providing for your retirement. It should stack up as a stand-alone investment in its own right.

If your business should fail and you can no longer lease the premises the you are hit with a double whammy with no income in your personal name and possibly an asset that is hard to lease to a new third-party

While it may be a sound investment now, things may change and your company may outgrow the premises leaving you again with a commercial property that may be hard to sell to extract equity for your next move.

Commercial, retail and industrial property is often a good income orientated investment with income well above that available from residential property but rarely sees the same degree of capital growth. You need to be aware of the trade-off and a diversified portfolio should be considered.

Once you are in pension phase you will need to fund pensions so you need to ensure liquidity in the fund. This is fine while rented or you can make contributions but remember if not working after age 65 you cannot make further contributions to help with liquidity.

Transfers of business real property purchased from related parties must be transferred at current market value as if the transaction was to occur on an arm’s length basis. This requirement allows for very little manipulation of the market value and heavy penalties could apply if any transfer value didn’t stand up to audit and ATO scrutiny.

So you have three or more options when it comes to the strategy. Your SMSF can buy the property utilising cash currently within the SMSF as a normal purchase. If your fund does not have enough cash then you can look at using a Limited Recourse Borrowing Arrangement to borrow the shortfall. More details on that strategy can be found here.

Alternatively, you can structure the deal as an in-specie transfer (a contribution of an asset, in this case property, instead of cash). You are still subject to member contribution caps but we have moved properties worth up to $500,000 in for couples and $1,000,000 where the SMSF had 4 members using a combination of concessional contributions limits and the 3-year bring forward rule on non-concessional limits.

You may also be able to use the Small Business CGT concessions in conjunction with a short term LRBA to move a property of up to $1.445,000 in to the fund with careful planning.

The whole deal has been sweetened by the fact that a number of the State Revenue Offices including NSW OSR have allowed concessional stamp duty stamp ($500) on in-specie property transfers whereby no cash has changed hands. This stamp duty saving can make transferring the business premises into a SMSF much more attractive. It should be noted that stamp duty is a state tax with no uniformity between states. Please seek legal advice always when dealing with stamp duty on property transfers and tax advice when moving assets between entities.

Remember the core philosophy behind Superannuation is that they must adhere to the Sole Purpose Test. While a strategy may help your business currently, its primary goal should be to provide for your retirement so the investment should always stand up as a viable investment regardless of your internal lease arrangements. Check out the most common mistakes people make when dealing with property, borrowing and a SMSF here:

Keep updated by putting an email address in on the left hand column and pressing the “Sign me up!” button.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I trained in General Insurance in the UK after my Graduation and much of that time was in the complaints, claims and product design departments. So I know how things go wrong when people take out unsuitable policies or under-insure their properties. 24 years later and nothing has changed, so I have been recommending people use a General Insurance Broker if they are inexperienced, lack confidence or want help and advice about insuring their business, liability or property assets.

That brings me to the title of this blog and I asked my preferred Insurance Broker here in the Hills District of Sydney, who operates countrywide, to explain the insurance requirements for an SMSF buying property

Don’t skimp on your insurances because when the time comes and you have a claim, you won’t be congratulating yourself on how much money you saved on your insurance premiums.

If you have purchased property in your SMSF it is important for you to take the correct steps to insure your investment.

If you borrow against the assets in your SMSF the mortgagor will require you to have adequate cover for the asset and for the Liability obligations of the SMSF. If the assets of the fund cover the purchase in full however you are still required as Trustee of the fund to correctly insure the funds interests. The fund is not permitted to “self-insure” any assets or property. The ATO has strict guidelines regarding the duties and obligations of SMSF trustees so it is important to get your insurance program right.

The question arises: who takes out the property insurance and landlord’s protection insurance, the SMSF Trustee or the Holding Trustee? I refer to this content from Towsends Law on the matter

SMSF Trustee The SMSF Trustee is entitled to take out insurances for the property as the Fund is liable under the loan and is also absolutely entitled to the benefit of the Property.

As the Fund is ultimately the party that is detrimentally affected should anything happen to the Property, the SMSF Trustee should ensure that the Fund is able to claim for any damage that might occur.

Holding Trustee The Holding Trustee is the legal owner of the land and is entitled to insure the property against damage, and likewise for landlord insurance. Some lenders may also insist that the registered proprietor of the property holds an insurance policy for the property.

But it is important to keep in mind the nature of the arrangement between the SMSF Trustee and Holding Trustee should insurance be taken out by the Holding Trustee.

As the Holding Trustee is a bare trustee it must make sure that it does not take any action unless it is directed to do so by the Fund Trustee, who is absolutely entitled to the Property. This direction by the Fund Trustee should be done formally and in writing and confirmed by the Holding Trustee executing minutes to confirm this action. Final Decision The final answer is that both the Holding Trustee and the SMSF Trustee have an insurable interest in the land and that both are eligible to be the owner of the property insurance and landlord’s protection insurance over the property.

In both instances all amounts payable in respect of the insurance should be paid by the Fund Trustee. Obviously the Holding Trustee must hold any policy proceeds on trust for the SMSF.

From a purely administrative position it would be easier for the SMSF to hold the insurances to avoid the constant but mandatory interplay between the SMSF and its bare trustee the Holding Trustee. But the insurance company may have its own requirements as might the Fund’s Lender.

So our preference is to have all insurances for the SMSF in the name of the fund. You cannot have personal items or assets listed on a policy in your funds name, and likewise you cannot have your fund’s assets listed on a personal policy for some of your personal assets.

As with all insurances, you really do get what you pay for. The more optional extras you include in your policy the more protection you will have. Let’s go through a fairly standard Landlords Insurance policy and give some simple definitions of each section. Like your personal household insurance policy your landlord’s policy will have cover for both your Building and for your Contents. These are fairly standard; however it is important to read the definitions to determine which items come under which section of cover. You may be in for a surprise if you haven’t studied the wording properly.

Where a Landlords Insurance policy differs in comparison to your standard household insurance is in the additional covers offered.

Loss of Rent – This is to cover your lost income if you have a claim under your building and contents cover, and the property becomes uninhabitable as a result.

Strata Title Mortgagee’s Protection – This covers the mortgagee named in the Schedule as if they were “You” on the same terms as Section1 against physical loss or physical damage caused by any of the Defined Events (it does not include the Additional Benefits).

Deliberate Damage and/or Theft by Tenants – Cover for physical damage arising from deliberate, intentional or malicious acts and acts of theft to the Building or Contents by the Tenant.

Tenant Default – This cover if for loss of rent, payable by the Tenant, which arises from damage covered under the Deliberate Damage/Theft by Tenant section above or from breach of a written Lease agreement.

Chances are you’ve worked hard at acquiring your assets and building your Super for your retirement. Don’t skimp on your insurances because when the time comes and you have a claim, you won’t be congratulating yourself on how much money you saved on your insurance premiums. Instead you will be hoping your insurance policy will respond to your claim.

If you’re at all unsure on what you need, talk to an Insurance Broker. If you don’t know an insurance broker, then speak to the people you trust with your Investments and your accounts because they should be able to put you in touch with an Insurance broker they trust.

For more information please don’t hesitate to contact me.

The SMSF Coach or Verante Financial Planning do not request or receive any commissions or referral fees from recommending services from Insurance brokers, we just want the best professional advice for our clients.