Like every strategy we discuss with clients we stress that have to look at the exit strategies up front rather than scramble to react if something happens that changes the financial position of the members or of the fund.

While a self managed superannuation fund can increase its assets and leverage the potential growth by borrowing to purchase a property, that borrowing can also cause financial distress if a fund member dies or becomes disabled. The lack of liquidity and cash flow could force the trustee to:

- Sell the property in a difficult or dropping market

- Realise capital gains or losses before expected i.e. before the members are in pension phase

- Have to deal with increased transaction costs.

Since August 2012 Trustees of an SMSF have been required to consider insurance for members and we would say that is very sensible when debt is involved.

SUPERANNUATION INDUSTRY (SUPERVISION) REGULATIONS 1994 – REG 4.09 (2)(e)

The trustee of the entity must formulate, review regularly and give effect to an investment strategy that has regard to the whole of the circumstances of the entity including, but not limited to, the following:

for a self managed superannuation fund – whether the trustees of the fund should hold a contract of insurance that provides insurance cover for one or more members of the fund

In the past strategies like Cross insurance on each member of superannuation fund was often used to reduce the impact that the sudden death or disability of a member may have on a fund however the ATO have ruled out many of these strategies including using the SMSF to fund Buy-Sell Agreements between business partners.

SMSF mortgage repayment solutions on death

If there is life insurance on the member that dies then any proceeds are added to their account balance and can be paid as a lump sum out of the fund to beneficiaries but that may leave a fund a debt still to be paid off and with less contributions going in as one member is deceased and the fund may not have the free cash-flow to fund the full balance pay out without selling the property.

The strategies outlined below are those now available as to manage the cash-flow liquidity issues and death benefit payment requirements that have arisen when a fund member dies suddenly, whilst the fund still has a Limited Recourse Loan Arrangement in place.

Payment of insurance benefits as an income stream to spouse

If it is 2 spouses or defacto’s that have set up an SMSF and borrowed to purchase an investment property, life insurance is often used to extinguish the debt. The reason for this is that generally the disability or death will eliminate or reduce the level of contributions that are made for the member, from which the loan repayments have been sourced.

Where the members of a fund are spouses then death benefits can be paid as an income stream. This means that even if a fund has borrowed to purchase a property, the property does not need to be disposed of to pay out the death benefit. This is even more important if your business is run out of the property.

In this case the life/TPD cover can be held by the member covered by the insurance and the premium can be paid from that members account. These arrangements comply with the SIS Regs, and the policy can be held through the self managed fund.

If the member dies or becomes disabled, the proceeds will be credited to the affected member’s account and loan will be repaid. Following the repayment of the loan a pension will commence to be paid to the member in the event of TPD or to the spouse in the event of death. If under 65 they can take as little as 4% per annum to keep as much in the fund as possible.

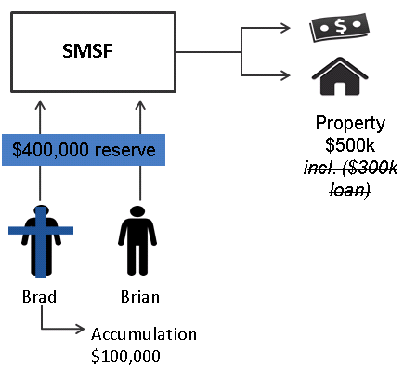

Example: Tax Dependants like spouses

Jack and Diane are married and members of Mellencamp Family Super Fund (“SMSF”)

Account Balances:

Jack – $100,000

Diane – $100,000

SMSF took out a loan of $300,000 to acquire property valued at $500,000

Jack dies after getting a bad knock playing football ( for the younger readers get the full story here

anyway thank you for indulging me and now back to the example:

SMSF Cash flow after Jack’s death

- The loan is paid out.

- Diane starts a minimum 4% annual death benefit pension. Only one member left contributing now but no interest to pay.

| Rent | $17,500 |

| Concessional contributions | $5,000 |

| Total inflows | $22,500 |

| Interest | $0 |

| Operating costs | ($2,000) |

| Life premiums | $0 |

| Pension | ($16,000) |

| Total outflows | ($18,000) |

| Tax | ($675) |

| Net cash flow (surplus) | $3,825 |

what are the tax implications of the pension

| Age at Death | Type of Super Death Benefit | Age of Recipient- DEPENDANT | Taxation Treatment of Taxed Element |

| Any age | Lump Sum | Any age | Tax free |

| 60 & above | Income stream | Any age | Tax free |

| Below 60 | Income stream | 60 & above | Tax free |

| Below 60 | Income stream | Below 60 | Marginal rate of tax less 15% tax offset |

To implement the strategy, the following factors, need to be considered:

- The funds trust deed must permit the fund to hold the insurance and to pay the TPD or death benefits as an income stream

- The fund’s investment strategy should state that the trustees have considered the needs of the individual members and determined to take out life insurance for the fund members in order to repay any outstanding mortgage under an LRBA

- Whether the fund’s cash flow allows for the taking out of the insurance policies. The premiums will normally be deductible in this circumstance as the benefits can be paid as a pension. For younger trustees you should consider Level Premiums and reviewing the cover as the loan is paid down.

Funding benefits from a reserve

If a fund is not able to pay a death or disability benefit in the form of a pension because they don’t have a spouse or the fund trust deed does not permit the payment of a benefit as a pension, then it may need to consider the use of a reserve strategy.

This strategy involves the fund trustee taking sufficient TPD and death cover over the lives of the fund members to enable the repayment of a loan and the payment of benefits as a lump sum.

The fact that the insurance policies are paid from the fund’s reserve and the insurance proceeds in the event of an insured event are credited to the reserve, means that the insurance benefit can remain in the fund. The fact that the insurance proceeds can remain in the fund means that insurance liabilities can be met and the loan repaid without the asset purchased under the borrowing arrangement needing to be sold.

In order to implement the strategy effectively, insurance policies premiums for each of the fund members will need to be paid from the reserve. The fact that the premium is paid from the reserve will then require any insurance proceeds after an insured event to be credited to the reserve.

Example 2 – Non- Tax Dependants – 2 brothers in a business

So sadly Brad dies …big ahhhh!

SMSF Cash flow after Brad’s death

- Death benefits are held in a Reserve.

- The loan is paid out but the value is held in the reserve account

- Results in large reserve ($400,000)

allocate back to Brian < 5% of his balance p.a. or

allocate up to $25,000 p.a. this year and $25,000pa going forward to Brian’s account depending on other concessional contributions in year

| Rent | $17,500 |

| Concessional contributions | $10,000 |

| Total inflows | $27,500 |

| Interest | ($18,000) |

| Operating costs | ($2,000) |

| Life premiums | ($1,500)* |

| Pension | $0 |

| Total outflows | ($21,500) |

| Tax | ($900) |

| Net cash flow (surplus) | $5,100 |

* Deducted from general fund expenses

Other Issues to consider

There are a number of other issues that fund trustees will need to consider when implementing this strategy:

- If the members of the fund are business partners rather than spouses, the spouse of the deceased member may feel that the business partners are benefiting from the death of their spouse. It is really important to discuss these strategies upfront with family so they know they are provided for but that the business needs stability too.

- When the insurance proceeds are credited to a reserve, it may be difficult to transfer that reserve back to fund members without exceeding the excessive concessional contributions cap.

- The insurance premiums are not tax-deductible under Section 295-465 of the ITAA 97 because the policy is not held for the purpose of providing a fund member with a death or disability benefit.

- The cost of the insurance premiums could be very high so seek advice on all possible solutions.

- The cost of the insurance premiums may limit the trustee’s capacity to take out other insurance cover for members

By the Way – one other reason to cover your exit strategies

What happens if a trustee fails to address insurance in their SMSF?

The trustees could be fined 100 penalty units ($21,000) for each trustee – Section 34 SIS Act; Section 4AA Crimes Act 1911

and if someone else has been affected by the loss as a result:

A person who suffers loss or damage …may recover … against that other person or against any person involved in the contravention. – Section 55(3) SIS Act

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

![]()

![]()

![]()

![]()

![]()

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Vichaya Kiatying-Angsulee at FreeDigitalPhotos.net