Not only do SMSF members need to have an up-to-date will but everyone who is a member of an SMSF needs to also put into place an enduring power of attorney.

The Australian Law Reform Commission’s (ALRC) recommendations in its final report titled “Elder Abuse – A National Legal Response” are positive steps towards helping mitigate the risks that could face ageing self-managed super fund (SMSF) members.

It involves changes to the superannuation laws to ensure that trustees consider planning for the loss of capacity of an SMSF member and estate planning as part of a fund’s investment strategy, and for the ATO to be told when an individual becomes a trustee of an SMSF because of an enduring power of attorney (EPOA).

TRUSTING SOMEONE TO DEAL WITH YOUR FINANCIAL MATTERS IF YOU CAN’T

An enduring power of attorney (EPOA) deals with your finances if you lose capacity or are unable to attend to financial matters personally and/or as a trustee of your SMSF. Your attorney is able to deal with your assets in the same way that you deal with them (subject to any directions or limitations and being appointed as a director of the SMSF Corporate Trustee). This includes signing tax returns and financial statements of the fund, buying and selling real estate or shares, accessing bank accounts and spending money on behalf of yourself personally and on your behalf as trustee of your SMSF.

For an EPOA to take your place as Trustee you must resign and they are appointed in your place. They cannot manage affairs of the SMSF using the EPOA alone, they must be made a trustee or a trustee director.

This is because if a member loses their mental capacity, perhaps through having a stroke or suffering onset of dementia, they will no longer be able to be a trustee of their fund, or a director of the corporate trustee, putting at risk the complying status of the fund.

Another occasion may be if a member departs overseas indefinitely. In this case their enduring attorney in Australia can become the trustee or director of the trustee in their place to avoid fund residency issues under subsection 295-95(2) of the Income Tax Assessment Act 1997.

Scenario we handled: Judith’s father was in the UK and had a fall. She flew back to check he was ok but found it was worse than expected and that he would need multiple surgeries and rehab over a protracted period and she would need to be there most of the time to manage the process and care for him. Her son, James, was her EPOA so she resigned as Director of the Trustee Company and James used the Enduring Power of Attorney to allow him to be appointed as director with her 2nd husband for the 3 year period she was away.

If you do not address the situation within the six-month period of grace allowed under section s17A(4) of the Superannuation Industry (Supervision) Act 1993 (SISA), the consequences for the fund and your retirement savings could be very serious indeed and attract severe penalties.

Unlike a general power of attorney, an EPOA continues to operate in the event that you lose capacity.

WHY SHOULD YOU HAVE A TRUSTED ENDURING POWER OF ATTORNEY?

It is important to have an EPOA in place for each fund member because without it, in the event that you lose capacity, your next of kin would have to make an application to the NSW Civil and Administrative Tribunal (or relevant government body in your state) to obtain a financial management order to deal with your assets. This lengthy (often more than the 6 month grace period allowed under the SIS Act) and costly process can be avoided if you have the foresight to establish your EPOA in advance. It can also lead to major friction in the family and especially with blended families and outcomes you did not expect or wish for under any circumstances!

EPOA SHOULD BE SOMEONE YOU TRUST AND CONSIDER APPOINTING SUBSTITUTE ATTORNEYS

We recommend that you seek legal advice and arrange for an EPOA to be prepared covering your personal finances and SMSF role. You may like to appoint your spouse, adult child, accountant, lawyer, business partner or close friend as your attorney in the first instance. Our legal advisers also suggest appointing substitute attorneys in case your primary attorney is unwilling or unable to act. We had one case where father had dementia but son who was EPOA was on secondment to PNG so could not take up the power of attorney

Your nominated attorney should be someone whom you trust and believe would make decisions in your best interests. I often recommend that you leave written details of your preferences for dealing with asset sales, buy backs, dividend reinvestment plans, term deposit maturities, minimum pensions and add clear instructions if they should work with trusted advisers like Financial planners, accountants and auditors before making major decisions.

You should of course consider having reversionary pensions or non-lapsing binding death nominations to ensure as much as possible that your wishes are carried out.

So when next reviewing your wills and powers of attorney just ask your solicitor if they are confident that the EPOA would also cover Superannuation matters or if that should be specifically mentioned.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

![]()

![]()

![]()

![]()

![]()

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

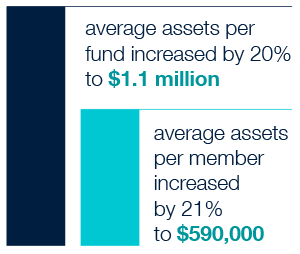

The majority of SMSFs continued to be solely in the accumulation phase (52%) with the remaining 48% making pension payments to some of or all members.

The majority of SMSFs continued to be solely in the accumulation phase (52%) with the remaining 48% making pension payments to some of or all members.