When I talk to self-directed SMSF trustees their excuse for not diversifying more from Aussie Shares and Term Deposits was that it was difficult to understand some sectors and to get a decent diversification without building a huge portfolio of stocks, unlisted managed funds, bonds, hybrids etc. They hated application forms especially for SMSF investments but they have been reluctant to use a platform despite my argument that often a platform was a useful vehicle. Most just are not interested in another layer of fees for their SMSF. Each to their own so I left the argument there. However now the mountain is coming to them!

The following is general information and not a recommendation, you still need to do your own research or get advice for your personal circumstances.

In November 2017 Vanguard Australia finally launched a suite of four exchange traded funds (ETFs) that provide greater access to their leading diversified portfolio strategies. This will make SMSF and personal investing a far more accessible and transparent option for many and ultimately help them achieve their financial goals at a lower cost, easier reporting and with less paperwork than currently. They offer a great opportunity to develop a well simple, market leading diversified core to your portfolio.

The four Vanguard Diversified Index ETFs build on their extensive suite of ETFs and unlisted Managed Funds, and are one of the first ETFs allowing investors to gain diversification across and within all major asset classes, while making a clear choice about how much risk they take on. I would argue that AMP’s DMKT and Schroder’s GROW do this to some extent but not at this low a cost as they are actively managed an many might think they are a good blend with Vanguard’s new range.

The conservative (VDCO), balanced (VDBA), growth (VDGR) and high growth (VDHG) ETFs offer investors simple, single trade access to Vanguard’s global expertise in portfolio management and asset allocation, with annual investment costs at just 0.27 per cent. Yes that’s only $2.70 management fee for every $1000 invested in a diversified portfolio, wipe the floor of many industry and retail super funds.

Each Diversified Index ETF is a share class of an existing Vanguard Diversified Index Fund, meaning ETF investors can tap into the benefits of an established asset pool, collectively worth more than $7 billion, through Vanguard’s existing range of non-listed multi-asset funds. Vanguard’s Diversified Index Funds consistently rank in the top quartile of performance with their peers over three, five and 10 year periods, according to Morningstar.

Yes you are giving up some transparency and control but I believe you can rely on Vanguard’s investment experts to continuously assess their portfolio’s exposure and periodically rebalance it back to its intended level of risk.”

Each Vanguard Diversified Index ETF provides investors with extensive global exposure to around 6500 individual companies and more than 5000 fixed income securities.

Just in case you have not heard of Vanguard, here is a little detail to help build a picture of their strength and reach:

The Vanguard Group, Inc.: Key facts and figures*

Founded

1975

Total assets under management

AUD $5.9 trillion

Funds offered

180 in the US, and 190 funds in markets outside the US

Ownership

The Vanguard Group, Inc. is owned by its US-domiciled funds,

which are owned by their shareholders.

Headquarters

Valley Forge, Pennsylvania, USA

Chairman and CEO

F. William McNabb III

Number of employees

About 15,000 worldwide

Vanguard’s Investment Strategy Group, a global team of researchers and analysts, set the asset allocation of the diversified funds as part of a robust framework used by Vanguard globally. This framework includes analysis of concentration risk and currency exposure, and incorporates comprehensive modelling generated by Vanguard’s proprietary forecasting engine, the Vanguard Capital Markets Model.

Looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why not contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make 2018 the year to get organised or it will be 2028 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Your superannuation trust deed along with the superannuation laws form the governing rules that self managed super funds (SMSFs) needs to operate by. The introduction of the $1.6 million transfer balance cap (TBC) and new transition to retirement income stream (TRIS) rules are a ‘game changer’ for SMSFs when discussing benefit payments and estate planning. With the new super rules in effect as of 1 July 2017, now is the right time to review if your trust deed needs to be enhanced or amended to deal with the new approaches and strategies you may need to implement.

Read the deed

The first step in reviewing your superannuation trust deed will be to read it. Trust deeds are legal documents which can be complex to read, so you may want help from an advisor with this.

It is likely that most deeds will not result in a breach of any superannuation laws and would provide the trustee with powers to comply with relevant tax and superannuation laws as they change over time.

The next step would be to review the deed in consideration with your own circumstances.

For example, a common scenario may be a restrictive deed that only provides the trustee with a discretion to pay death benefits. Therefore, if a member of that SMSF wanted to create a binding death benefit nomination, it would be irrelevant due to the deed’s governing rules.

In any event, deeds which are clearly out of date will need to be amended as soon as possible.

Deeds post 1 July 2017

Post 1 July 2017, there are many approaches and strategies that will differ from the past and it is essential to ensure that your SMSF deed does not restrict you in anyway. We note the following areas should be considered:

Paying death benefits

The $1.6 million TBC now restricts the amount of money that can be kept in super on the death of a member. This is crucially important as when a member dies, their TBC dies with them. SMSF members should review their estate planning and further review their trust deed for the following:

Does it allow for binding death benefit nominations (BDBN)?

Do BDBNs lapse every 3 years in accordance with the trust deed when the legislation does not prescribe it?

Does it consider the appropriate solution when there is a conflict between a reversionary pension and a BDBN and which will take precedence?

Reversionary pensions

Reversionary pensions are pensions which continue being paid to a dependant after your death. Under the TBC, reversionary pensions will not count towards a member’s TBC until 12 months after the date of the original recipient’s death. Importantly, the transfer of the pension from the deceased to the new recipient will count towards the TBC. The value of the credit to the TBC will be the value of the pension at the date of death, not the value after 12 months. This increases the complexity of reversionary pensions prompting a review of trust deeds to consider:

Does it allow for a reversionary pension to be added to an existing pension or are there restrictions?

Should it automatically ensure that a pension is reversionary so that it is paid to a surviving spouse?

Pensions

The TBC also has implications for strategies in commencing pensions and making benefit payments. Trust deeds may need to be reviewed for:

Ensuring that commutations are able to be moved into accumulation phase rather than being forced as lump sums out of superannuation.

Are there any specific provisions relating to the TBC? There may be value in ensuring that the deed restricts pensions from being commenced with a value greater than the TBC.

Are there provisions which detail where commutations must be sourced from first?

Are there restrictive pension provisions that the trustees must comply with?

Transition to retirement income streams

Tax concessions for TRISs where the recipient does not have unrestricted access to their superannuation savings (known as meeting a condition of release with a nil chasing restriction) have also been removed. Trust deeds may need to be reviewed for:

Does the deed allow for the 10% maximum benefit payment to fall away once a nil condition of release is met?

Does the deed deal with a TRIS’s character when a nil condition of release? (Does it convert into an account based pension?)

How can we help?

SMSF Specialist Advisors can help you understand how the new laws may impact you and partner with a lawyer/Deed provider to review and amend your trust deed as required. Please feel free to give me a call to arrange a time to meet so that we can discuss your particular requirements, especially in regards to issues that may arise out of the latest super laws, in more detail.

For further educational information please subscribe to this blog and also visit the SMSF Association’s Trustee Knowledge Centre (http://trustees.smsfassociation.com/) to keep on top of the latest changes and information to reach your retirement goals and get the most out of your self managed super fund.

Want a Superannuation Review or are you just looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make this the year to get organised or it will be 2028 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

There are many rumours and well-intentioned but wrong advice out here on the internet about how to maximise Centrelink or DVA pension by “gifting assets” before applying. I want to clear up some of those misunderstandings

The gifting and deprivation rules prevent you from giving away assets or income over a certain level in order to increase age pension and allowance entitlements. For Centrelink and Department of Veteran’s Affairs (DVA) purposes, gifts made in excess of certain amounts are treated as an asset and subject to the deeming provisions for a period of 5 years from disposal.

Acknowledgement: I have relied on the excellent guidance of the AMP TAPin team for the majority of the content in this article. They write great technical articles for advisors and I try and make them SMSF trustee friendly.

What is considered a gift for Centrelink purposes?

For deprivation provisions to apply, it must be shown that a person has destroyed or diminished the value of an asset, income or a source of income.

A person disposes of an asset or income when they:

− engage in a course of conduct that destroys, disposes of or diminishes the value of their assets or income, and

− do not receive adequate financial consideration in exchange for the asset or income.

Adequate financial consideration can be accepted when the amount received reasonably equates to the market value of the asset. It may be necessary to obtain an independent market valuation to support your estimated value or transferred value or Centrelink may use their own resources to do so..

Deprivation also applies where the asset gifted does not actually count under the assets test. For example, unless the ‘granny flat’ provisions apply, deprivation is assessed if a person does not receive adequate financial consideration when they:

− transfer the legal title of their principal home to another person, or

− buy a new principal home in another person’s name.

What are the gifting limits?

The gifting rules do not prevent a person from making a gift to another person. Rather, they cap the amount by which a gift will reduce a person’s assessable income and assets, thereby increasing social security entitlements.

There are two gifting limits.

A person or a couple can dispose of assets of up to $10 000 each financial year. This $10, 000 limit applies to a single person or to the combined amounts gifted by a couple, and

An additional disposal limit of $30 000 over a five financial years rolling period.

The $10,000 and $30,000 limits apply together. That is, although people can continue to gift assets of up to $10 000 per financial year without penalty, they need to take care not to exceed the gifting free limit of $30 000 in a rolling five-year period.

What happens if the gifting limits are exceeded?

If the gifting limits are breached, the amount in excess of the gifting limit is considered to be a deprived asset of the person and/or their spouse.

The deprived amount is then assessed as an asset for 5 anniversary years from the date of gift. It is assessed as an asset for asset test purposes and subject to deeming under the income test.

After the expiration of the 5 year period, the deprived amount is neither considered to be a person’s asset nor deemed.

Example 1: Single pensioner – gifts not impacted by deprivation rules

Sally, a single pensioner, has financial assets valued at $275,000. She has decided to gift some money to her son to improve his financial situation. Her plan for gifting is as follows:

Financial year

2017/18

2018/19

2019/20

2020/21

2021/22

2022/23

Amount gifted

$6,000

$6,000

$6,000

$6,000

$6,000

$6,000

With this gifting plan, Sally is not affected by either gifting rule. This is because she has kept under the $10,000 in a single year rule and also within the $30,000 per rolling five-year period.

Example 2: Single pension – Gifts impacted by both gifting rules

Peter is eligible for the Age Pension. He has given away the following amounts:

Financial year

Amount gifted

Deprived asset assessed using the $10,000 in a financial year free area rule

Deprived asset assessed using the $30,000 five-year free area rule

2017/18

$33,000

$23,000

$0

2018/19

$2,000

$0

$0

In this case, $23,000 of the $33,000 given away in 2017/18 exceeds the gifting limit (the first limit of $10,000) for that financial year, so it will continue to be treated as an asset and subject to deeming for five years.

In 2018/19, while gifts totalling $35,000 have been made, no deprived asset is assessed under the five-year rule after taking into account the deprived assets already assessed, ie $33,000 + $2,000 – $23,000 = $12,000, which is less than the relevant limit of $30,000.

Example 3: Couple impacted by both gifting rules

Ted and Alice are eligible for the Age Pension. They give away the following amounts:

Financial year

Amount gifted

Deprived asset assessed using the $10,000 in a financial year free area rule

Deprived asset assessed using the $30,000 five-year free area rule

2017/18

$10,000

$0

$0

2018/19

$13,000

$3,000

$0

2019/20

$10,000

$0

$0

2020/21

$10,000

$0

$10,000

2021/22

Any gifts in 2014/15 will be assessed as deprived assets under the five-year rule

In this case, $3,000 of the $13,000 given away in 2018/19 exceeds the gifting limit for that year, so it will continue to be treated as an asset and subject to deeming for five years. The $10,000 given away in 2020/21 exceeds the $30,000 limit for the five-year period commencing on 1 July 2017, so it will also continue to be treated as an asset and subject to deeming for five years.

Are some gifts exempt from the rules?

Certain gifts can be made without triggering the gifting provisions. Broadly speaking, these include:

− Assets transferred between the members of a couple. A common example is where a person who has reached Age Pension age withdraws money from their superannuation and contributes it to a superannuation account in the name of the spouse who has not yet reached age pension age.

− Certain gifts made by a family member or a certain close relative to a Special Disability Trust. For more information on Special Disability Trusts, refer to Department of Human Services – Special Disability Trusts.

− Assets given or construction costs paid for a ‘granny flat’ interest. See Department of Human Services – Granny Flat Interest for further detail.

Trying to be too smart – Gifting prior to claim

Contrary to what many read on the internet any amounts gifted in the five years prior to accessing the Age Pension or other allowance are subject to the gifting rules

Deprivation provisions do not apply when a person has disposed of an asset within the five years prior to accessing the Age Pension or other allowance but could not reasonably have expected to become qualified for payment. For example, a person qualifies for a social security entitlement after unexpected death of a partner or job loss.

Gifting and deceased estates

The gifting rules apply to a person’s interest in a deceased estate if the person does any of the following:

− Gives away their right to their interest in a deceased estate for no/inadequate consideration,

− Directs the executor to distribute their interest in a deceased estate for no/inadequate consideration, or

− After the estate has been finalised, gives away their interest in a deceased estate to a third-party for no/inadequate consideration.

The above rules apply even if the deceased died without a will.

Gifting and death of a partner

In some circumstances, couples in receipt of a social security benefit may give away assets prior to death of one of them. Prior to death, any deprived assets would have been assessed against the pensioner couple for five years from the date of the disposal. Now that a member of the couple has passed away, how will the deprived assets be assessed for the surviving partner?

The amount of deprivation that continues to be held against a surviving partner depends on who legally owned the assets prior to death.

Table 1: Gifting and death of a partner

Legal owner of the deprived asset

Assessment of deprived assets

jointly,

does not change.

by the deceased partner,

is reduced to zero.

by the surviving partner,

increases by the amount held against the deceased partner by the outstanding balance held against the deceased partner.

Example 4: Death of a partner

Daryl (age 84) and Gail (age 78) gifted an apartment worth $260,000 to their son Ethan on 1 July 2019. At the time the gift was made, Centrelink assessed $250,000 as a deprived asset. Daryl passed away on 1 July 2020.

The treatment of the deprived assets for Gail will depend on who legally owned the assets prior to Daryl’s death. The impact of different ownership options is shown below:

Legal owner of the deprived asset

Assessment of deprived assets

jointly,

Half of the asset value of the deprived asset will be assessed against the surviving spouse. As the amount of the deprived asset is $250,000, only $125,000 will be assessed against Gail

by the deceased partner,

No amount will be assessed against the surviving partner. As the amount of the deprived asset is $250,000, the amount assessable to Gail is $0.

by the surviving partner,

The full amount will continue to be assessed against the surviving partner. As the amount of the deprived asset is $250,000, the amount assessable to Gail remains at $250,000.

Want a Centrelink Review or are you just looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why not contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make this the year to get organised or it will be 2028 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

With all the talk about Total Super Balance caps and where people will invest money going forward if they can’t get it in to superannuation, the spotlight is being shone on “trusts” at present. This has also brought with it the claims of tax avoidance or tax minimisation, so what exactly are trusts and are there differences between Family Trusts, Units Trusts, Discretionary Trusts and Testamentary Trusts to name a few.

Trusts are a common strategy and this article aims to aid a better understanding of how a trust works, the role and obligations of a trustee, the accounting and income tax implications and some of the advantages and pitfalls. Of course, there is no substitute for specialist legal, tax and accounting advice when a specific trust issue arises and the general information in this article needs to be understood within that context.

Introduction

Trusts are a fundamental element in the planning of business, investment and family financial affairs. There are many examples of how trusts figure in everyday transactions:

Cash management trusts and property trusts are used by many people for investment purposes

Joint ventures are frequently conducted via unit trusts

Money held in accounts for children may involve trust arrangements

Superannuation funds are trusts

Many businesses are operated through a trust structure

Executors of deceased estates act as trustees

There are charitable trusts, research trusts and trusts for animal welfare

Solicitors, real estate agents and accountants operate trust accounts

There are trustees in bankruptcy and trustees for debenture holders

Trusts are frequently used in family situations to protect assets and assist in tax planning.

Although trusts are common, they are often poorly understood.

What is a trust?

A frequently held, but erroneous view, is that a trust is a legal entity or person, like a company or an individual. But this is not true and is possibly the most misunderstood aspect of trusts.

A trust is not a separate legal entity. It is essentially a relationship that is recognised and enforced by the courts in the context of their “equitable” jurisdiction. Not all countries recognise the concept of a trust, which is an English invention. While the trust concept can trace its roots back centuries in England, many European countries have no natural concept of a trust, however, as a result of trade with countries which do recognise trusts their legal systems have had to devise ways of recognising them.

The nature of the relationship is critical to an understanding of the trust concept. In English law the common law courts recognised only the legal owner and their property, however, the equity courts were willing to recognise the rights of persons for whose benefit the legal holder may be holding the property.

Put simply, then, a trust is a relationship which exists where A holds property for the benefit of B. A is known as the trustee and is the legal owner of the property which is held on trust for the beneficiary B. The trustee can be an individual, group of individuals or a company. There can be more than one trustee and there can be more than one beneficiary. Where there is only one beneficiary the trustee and beneficiary must be different if the trust is to be valid.

The courts will very strictly enforce the nature of the trustee’s obligations to the beneficiaries so that, while the trustee is the legal owner of the relevant property, the property must be used only for the benefit of the beneficiaries. Trustees have what is known as a fiduciary duty towards beneficiaries and the courts will always enforce this duty rigorously.

The nature of the trustee’s duty is often misunderstood in the context of family trusts where the trustees and beneficiaries are not at arm’s length. For instance, one or more of the parents may be trustees and the children beneficiaries. The children have rights under the trust which can be enforced at law, although it is rare for this to occur.

Types of trusts

In general terms the following types of trusts are most frequently encountered in asset protection and investment contexts:

Fixed trusts

Unit trusts

Discretionary trusts – Family Trusts

Bare trusts

Hybrid trusts

Testamentary trusts

Superannuation trusts

Special Disability Trusts

Charitable Trusts

Trusts for Accommodation – Life Interests and Rights of Residence

A common issue with all trusts is access to income and capital. Depending on the type of trust that is used, a beneficiary may have different rights to income and capital. In a discretionary trust the rights to income and capital are usually completely at the discretion of the trustee who may decide to give one beneficiary capital and another income. This means that the beneficiary of such a trust cannot simply demand payment of income or capital. In a fixed trust the beneficiary may have fixed rights to income, capital or both.

Fixed trusts

In essence these are trusts where the trustee holds the trust assets for the benefit of specific beneficiaries in certain fixed proportions. In such a case the trustee does not have to exercise a discretion since each beneficiary is automatically entitled to his or her fixed share of the capital and income of the trust.

Unit trusts

These are generally fixed trusts where the beneficiaries and their respective interests are identified by their holding “units” much in the same way as shares are issued to shareholders of a company.

The beneficiaries are usually called unitholders. It is common for property, investment trusts (eg managed funds) and joint ventures to be structured as unit trusts. Beneficiaries can transfer their interests in the trust by transferring their units to a buyer.

There are no limits in terms of trust law on the number of units/unitholders, however, for tax purposes the tax treatment can vary depending on the size and activities of the trust.

Discretionary trusts – Family Trusts

These are often called “family trusts” because they are usually associated with tax planning and asset protection for a family group. In a discretionary trust the beneficiaries do not have any fixed interests in the trust income or its property but the trustee has a discretion to decide whether anyone will receive income and/or capital and, if so, how much.

For the purposes of trust law, a trustee of a discretionary trust could theoretically decide not to distribute any income or capital to a beneficiary, however, there are tax reasons why this course of action is usually not taken.

The attraction of a discretionary trust is that the trustee has greater control and flexibility over the disposition of assets and income since the nature of a beneficiary’s interest is that they only have a right to be considered by the trustee in the exercise of his or her discretion.

Bare trusts

A bare trust exists when there is only one trustee, one legally competent beneficiary, no specified obligations and the beneficiary has complete control of the trustee (or “nominee”). A common example of a bare trust is used within a self-managed fund to hold assets under a limited recourse borrowing arrangement.

Hybrid trusts

These are trusts which have both discretionary and fixed characteristics. The fixed entitlements to capital or income are dealt with via “special units” which the trustee has power to issue.

Testamentary trusts

As the name implies, these are trusts which only take effect upon the death of the testator. Normally, the terms of the trust are set out in the testator’s will and are often used when the testator wishes to provide for their children who have yet to reach adulthood or are handicapped.

Superannuation trusts

All superannuation funds in Australia operate as trusts. This includes self-managed superannuation funds.

The deed (or in some cases, specific acts of Parliament) establishes the basis of calculating each member’s entitlement, while the trustee will usually retain discretion concerning such matters as the fund’s investments and the selection of a death benefit beneficiary.

The Federal Government has legislated to establish certain standards that all complying superannuation funds must meet. For instance, the “preservation” conditions, under which a member’s benefit cannot be paid until a certain qualification has been reached (such as reaching age 65), are a notable example.

Special Disability Trusts

Special Disability Trusts allow a person to plan for the future care and accommodation needs of a loved one with a severe disability. Find out more in this Q & A about Special Disability Trusts.

Charitable Trusts

You may wish to provide long term income benefit to a charity by providing tax free income from your estate, rather than giving an immediate gift. This type of trust is effective if large amounts of money are involved and the purpose of the gift suits a long term benefit e.g. scholarships or medical research.

Trusts for Accommodation – Life Interests and Right of Residence

A Life Interest or Right of Residence can be set up to provide for accommodation for your beneficiary. They are often used so that a family member can have the right to live in the family home for as long as they wish. These trusts can be restrictive so it is particularly important to get professional advice in deciding whether such a trust is right for your situation.

Establishing a trust

Although a trust can be established without a written document, it is preferable to have a formal deed known as a declaration of trust or a deed of settlement. The declaration of trust involves an owner of property declaring themselves as trustee of that property for the benefit of the beneficiaries. The deed of settlement involves an owner of property transferring that property to a third person on condition that they hold the property on trust for the beneficiaries.

The person who transfers the property in a settlement is said to “settle” the property on the trustee and is called the “settlor”.

In practical terms, the original amount used to establish the trust is relatively small, often only $10 or so. More substantial assets or amounts of money are transferred or loaned to the trust after it has been established. The reason for this is to minimise stamp duty which is usually payable on the value of the property initially affected by the establishing deed.

The identity of the settlor is critical from a tax point of view and it should not generally be a person who is able to benefit under the trust, nor be a parent of a young beneficiary. Special rules in the tax law can affect such situations.

Also critical to the efficient operation of a trust is the role of the “appointor”. This role allows the named person or entity to appoint (and usually remove) the trustee, and for that reason, they are seen as the real controller of the trust. This role is generally unnecessary for small superannuation funds (those with fewer than five members) since legislation generally ensures that all members have to be trustees.

The trust fund

In principle, the trust fund can include any property at all – from cash to a huge factory, from shares to one contract, from operating a business to a single debt. Trust deeds usually have wide powers of investment, however, some deeds may prohibit certain forms of investment.

The critical point is that whatever the nature of the underlying assets, the trustee must deal with the assets having regard to the best interests of the beneficiaries. Failure to act in the best interests of the beneficiaries would result in a breach of trust which can give rise to an award of damages against the trustee.

A trustee must keep trust assets separate from the trustee’s own assets.

The trustee’s liabilities

A trustee is personally liable for the debts of the trust as the trust assets and liabilities are legally those of the trustee. For this reason if there are significant liabilities that could arise a limited liability (private) company is often used as trustee.

However, the trustee is entitled to use the trust assets to satisfy those liabilities as the trustee has a right of indemnity and a lien over them for this purpose.

This explains why the balance sheet of a corporate trustee will show the trust liabilities on the credit side and the right of indemnity as a company asset on the debit side. In the case of a discretionary trust it is usually thought that the trust liabilities cannot generally be pursued against the beneficiaries’ personal assets, but this may not be the case with a fixed or unit trust.

Powers and duties of a trustee

A trustee must act in the best interests of beneficiaries and must avoid conflicts of interest. The trustee deed will set out in detail what the trustee can invest in, the businesses the trustee can carry on and so on. The trustee must exercise powers in accordance with the deed and this is why deeds tend to be lengthy and complex so that the trustee has maximum flexibility.

Who can be a trustee?

Any legally competent person, including a company, can act as a trustee. Two or more entities can be trustees of the same trust.

A company can act as trustee (provided that its constitution allows it) and can therefore assist with limited liability, perpetual succession (the company does not “die”) and other advantages. The company’s directors control the activities of the trust. Trustees’ decisions should be the subject of formal minutes, especially in the case of important matters such as beneficiaries’ entitlements under a discretionary trust.

Trust legislation

All states and territories of Australia have their own legislation which provides for the basic powers and responsibilities of trustees. This legislation does not apply to complying superannuation funds (since the Federal legislation overrides state legislation in that area), nor will it apply to any other trust to the extent the trust deed is intended to exclude the operation of that legislation. It will usually apply to bare trusts, for example, since there is no trust deed, and it will apply where a trust deed is silent on specific matters which are relevant to the trust – for example, the legislation will prescribe certain investment powers and limits for the trustee if the deed does not exclude them.

Income tax and capital gains tax issues

Because a trust is not a person, its income is not taxed like that of an individual or company unless it is a corporate, public or trading trusts as defined in the Income Tax Assessment Act 1936. In essence the tax treatment of the trust income depends on who is and is not entitled to the income as at midnight on 30 June each year.

If all or part of the trust’s net income for tax purposes is paid or belongs to an ordinary beneficiary, it will be taxed in their hands like any other income. If a beneficiary who is entitled to the net income is under a “legal disability” (such as an infant), the income will be taxed to the trustee at the relevant individual rates.

Income to which no beneficiary is “presently entitled” will generally be taxed at highest marginal tax rate and for this reason it is important to ensure that the relevant decisions are made as soon as possible after 30 June each year and certainly within 2 months of the end of the year. The two month “period of grace” is particularly relevant for trusts which operate businesses as they will not have finalised their accounts by 30 June. In the case of discretionary trusts, if this is done the overall amount of tax can be minimised by allocating income to beneficiaries who pay a relatively low rate of tax.

The concept of “present entitlement” involves the idea that the beneficiary could demand immediate payment of their entitlement.

It is important to note that a company which is a trustee of a trust is not subject to company tax on the trust income it has responsibility for administering.

In relation to capital gains tax (CGT), a trust which holds an asset for at least 12 months is generally eligible for the 50% capital gains tax concession on capital gains that are made. This discount effectively “flows” through to beneficiaries who are individuals. A corporate beneficiary does not get the benefit of the 50% discount. Trusts that are used in a business rather than an investment context may also be entitled to additional tax concessions under the small business CGT concessions.

Since the late 1990s discretionary trusts and small unit trusts have been affected by a number of highly technical measures which affect the treatment of franking credits and tax losses. This is an area where specialist tax advice is essential.

Why a trust and which kind?

Apart from any tax benefits that might be associated with a trust, there are also benefits that can arise from the flexibility that a trust affords in responding to changed circumstances.

A trust can give some protection from creditors and is able to accommodate an employer/employee relationship. In family matters, the flexibility, control and limited liability aspects combined with potential tax savings, make discretionary trusts very popular.

In arm’s length commercial ventures, however, the parties prefer fixed proportions to flexibility and generally opt for a unit trust structure, but the possible loss of limited liability through this structure commonly warrants the use of a corporate entity as unitholder ie a company or a corporate trustee of a discretionary trust.

There are strengths and weaknesses associated with trusts and it is important for clients to understand what they are and how the trust will evolve with changed circumstances.

Trusts which incur losses

One of the most fundamental things to understand about trusts is that losses are “trapped” in the trust. This means that the trust cannot distribute the loss to a beneficiary to use at a personal level. This is an important issue for businesses operated through discretionary or unit trusts.

Establishment procedures

The following procedures apply to a trust established by settlement (the most common form of trust):

Decide on Appointors and back-up Appointors as they are the ultimate controllers of the trust. They appoint and change Trustees.

Settlor determined to establish a trust (should never be anyone who could become a beneficiary)

Select the trustee. If the trustee is a company, form the company.

Settlor makes a gift of money or other property to the trustee and executes the trust deed. (Pin $10 to the front of the register is the most common way of doing this)

Apply for ABN and TFN to allow you open a trust bank account

Establish books of account and statutory records and comply with relevant stamp duty requirements (Hint: Get your Accountant to do this)

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

There are all sorts of unexpected consequences coming out of the changes to the superannuation rules. As a result of moving funds over $1.6m back to accumulation to meet the Transfer Balance Cap (TBC), you may in fact now qualify for the Commonwealth Seniors Health Care card.

How?

There may be a silver lining to the new $1.6 million transfer balance cap (TBC) for some SMSF members. Having less money in an account based pension and more money in accumulation or other assets may result in some SMSF members being entitled to receive the Commonwealth Seniors Health Card (CSHC). This is because amounts held in accumulation phase are not deemed for the CSHC and are not included in a member’s personal taxable income.

Now if the excess over the $1.6m is/was withdrawn out of superannuation, whether it will count as income for the CHSC will depend on how the client invests it. for example financial investments such as shares, rented investment property and interest will be deemed but a Holiday home not rented out will not be deemed towards the CSHC income test.

Older pensions may be even more forgiving!

Income from an account based pension is deemed under the usual Centrelink deeming rates unless the account based pension commenced before 1 January 2015, and the client was entitled to the card before 1 January 2015 and continues to hold the card. This is known as the grandfathering rules.

For SMSF members who are not eligible for the grandfathering rules, holding a significant amount of money in an account based pension means that they have a lower likelihood of being eligible for a CSHC. Prior to 1 July 2017, for most SMSF members it was more beneficial to hold as much as possible in an account based pension for tax purposes even if this meant they were ineligible for the CSHC. The tax savings on the excess would have outstripped the CSHC benefit.

However, from 1 July 2017, SMSF members can only hold up to $1.6 million in an account based pension and if they are also receiving defined benefit pension income the amount which can be held in account based pensions will be lower. Depending on other income the member receives, this may result in them now being entitled to the CSHC.

You don’t believe me? The following example explains how this works in a simple scenario:

Example – single person

James is single and is age 67. In the 2016 -2017 financial year, he had $2 million in his account based pension, and no other income.

The deemed income from his account based pension is calculated as $64,247 based on deeming rates and thresholds as at 1 July 2017. His deemed income exceeds the income threshold of $52,796 for the CSHC and therefore he is not entitled to a CSHC.

On 30 June 2017, he rolls $400,000 back to accumulation leaving $1.6million in his account based pension.

The deemed income on $1.6 million is $51,247 and is under the income threshold of $52,796 (20 March 2017) meaning that James is entitled to a CSHC after rolling back money from his account based pension to accumulation.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Client Question : My next question is about the threshold income level at which my wife and I will start to pay personal tax in 2017-18. I read “about $28,000” in the paper the other day for my situation (age >65), but my wife does not turn 65 until 2018, so her tax-free level may be different. It would be useful to know these numbers in the case we decide to take some lump sums out of super because of the new limits. We are considering investing some money tax-free in our personal names, free of SMSF red tape.

Personal Tax-free Thresholds

The amount you can earn before you have to pay tax, actually depends on your age.

Under 65

For those people under age 65, the effective tax-free threshold is currently $20,542. How do we calculate this amount? Well, if you look at the ATO’s current Individual income tax rate table, you pay no tax on the first $18,200 you earn in a year.

However, you also get the benefit of the full low income tax offset if you earn below $37,000. That means the tax office will offset up to $445 from the tax you would normally have to pay. So you can earn another couple of thousand dollars before you have to pay tax.

How much can I earn before paying taxes after age 65

For those who have reached age pension age, they can earn even more without paying tax. If you are over 65, you get access to the Seniors and Pensioners Tax Offset (SAPTO). This reduces or eliminates the tax that would normally be liable to pay on some additional income

Using the SAPTO benefit, the amount you can earn each year as a pensioner before having to pay tax, is:

$32,279 for single people,

$28,974 each for members of a couple or $57,948 combined.

The beauty of this benefit is that for clients in SMSF Pension phase any income drawn from a super fund income stream once over 60 is tax-free and non-assessable, meaning it doesn’t count towards the above thresholds.

Based on an earnings rate of 5% this means that a couple could have over $500,000 in each of their names and not pay any tax. But be careful as if you are investing in growth assets then triggering capital gains in the future may mean exceeding these thresholds where as within the SMSF the CGT on pension assets is NIL and 10-15% in accumulation.

Also consider the tax position if you are likely:

to receive an inheritance

large capital gain on an asset he’d outside super

to have one parter live significantly longer (they may end up with large amounts outside the super system)

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Tax free Image courtesy of Stuart Miles /FreeDigitalPhotos.net

The changes to the superannuation system, announced by the Australian Government in the 2016–17 Budget, have now received royal assent and the finer details of how to implement them have been released. While the government claim these changes were designed to improve the sustainability, flexibility and integrity of Australia’s superannuation system, they did not work with industry or the ATO before announcing them and as such it has been a nightmare to try to get your head around what the actual changes are and how strategies need to be implemented to manage them.

As a result we are getting last-minute guidance from the ATO and software providers as well as SMSF, Industry and Retail Super providers. The government have back-flipped on some measures, amended others because of collateral damage and tightened other measures for obscure reasons. With most of these changes commencing from 1 July 2017 I have tried to put some useful links together.

A short video overview of the changes is provided below. I have provided more detailed information links and will update these as they are progressively published to help you understand the changes, how they may affect you, and what you may need to know and do now, or in the future as a trustee of a self-managed super fund (SMSF). Even more detailed information is available to help you understand the changes, including for some topics, law companion guidelines (see below) to provide certainty about how the changes will be administered.

For those who wish to dive in to the detail please view the Law Companion Guides below. A law companion guideline is a type of public ruling. It gives the ATO view on how recently enacted law applies. It is usually developed at the same time as the drafting of the Bill.

The ATO normally release a law companion guideline in draft form for comment when the Bill is introduced into Parliament. It is finalised after the Bill receives Royal Assent. It provides early certainty in the application of the new law. Please make sure to look for updates before relying on this information.

The ATO have also released access to answers to some frequently asked questions and they can be found in this document Super Changes Q & As

Example: Q. How are my pensions and annuities valued for transfer balance cap purposes?

ANSWER : You need to contact your fund about the value of your pensions and annuities.

The value of your pension or annuity will generally be the value of your pension account for an account-based pension.

Special rules apply to calculate the value of: • lifetime pensions • lifetime annuities that existed on 30 June 2017, and • life expectancy and market linked pensions and annuities where the income stream existed on 30 June 2017

Lifetime pension and annuities These are valued by multiplying the annual entitlement by a factor of 16.This provides a simple valuation rule based on general actuarial considerations. Your annual entitlement to a superannuation income stream is worked out by reference to the first payment entitlement for the year. The first payment is annualised based on the number of days in the period to which the payment refers. (I.e. the first payment divided by the number of days the payment relates to multiplied by 365).

This means that a lifetime pension that pays $100,000 per annum will have a special value of $1.6 million which counts towards your transfer balance cap in the 2017-18 financial year.

For a lifetime pension or annuity already being paid on 1 July 2017, the special value will be based on annualising the first payment in the 2017-18 financial year. This may include indexation, so may be slightly higher than your current annual lifetime pension payments.

Life expectancy and market linked pensions and annuities being paid on or before 30 June 2017 are valued by multiplying the annual entitlement by the number of years remaining on the term of the product (rounded up to the nearest year).

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

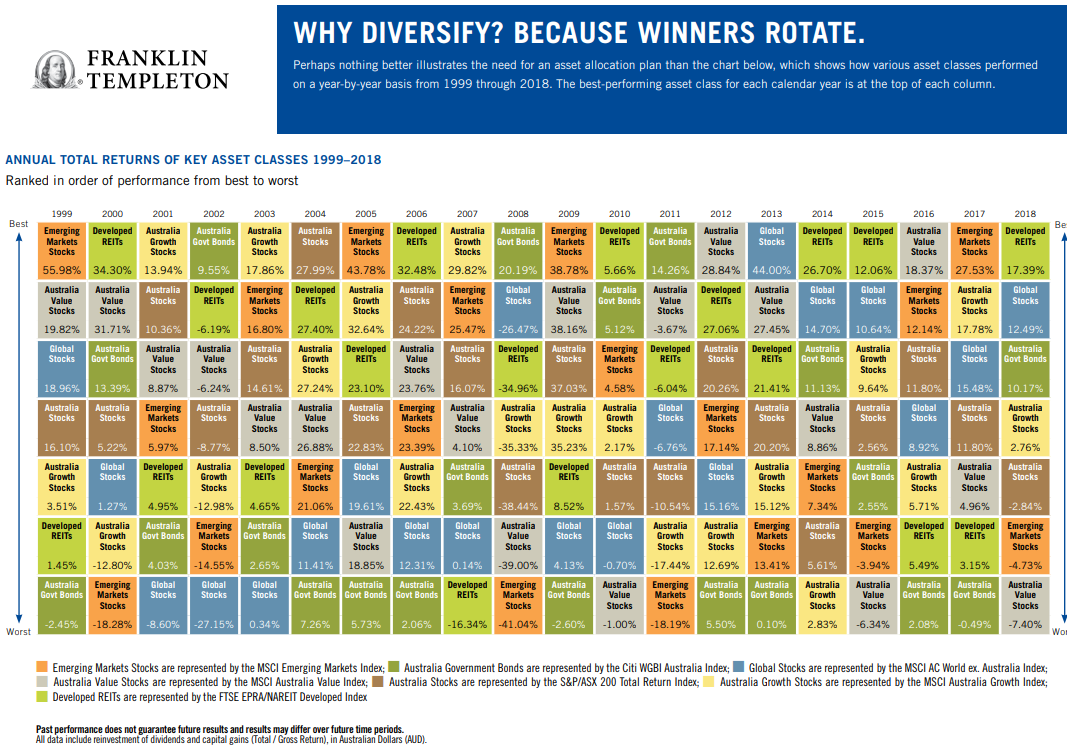

Do you know which asset sector performed best last year, the year before? Do you think those results will guide you for next year? Think again. I don’t think many SMSF Investors would have guessed Global Listed Property would have been the top performers in the last 6 years but in 2016 was a disappointing under performer. Many burnt in the property sector in the GFC had avoided it like the plague and missed some of the upside.

Franklin Templeton Austalia’s annual asset class ladder for 2018 is a great tool to visualise how each asset class/sector has performed over the last 20 years and pour water on ideas that we can reliably predict next years winners.

Click on this picture to access the larger version in PDF pormat

What becomes glaringly obvious after scrutinising the table is that no single asset class consistently outperforms the others. Just in case you subscribe to the ‘last years greyhound is this years dog” or that cycles are predictable, the table shows no clues or discernible pattern into how the previous year’s winners or losers will perform in the following year as the pattern appears totally random.

We coach clients to build a diversified strategy with some tactical allocations when sectors or assets appear oversold or opportunities arise like when the Aussie dollar was getting USD $1.10 a few years back and the opportunity came to overweight international stocks.

I hope this information has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Rate for 2025-26 Related Property LRBA is 8.95%and Listed Shares 10.95%

Old Rate for 2024-25 Related Property LRBA was 9.35% and Listed Shares 11.35%

The ATO have issued long-awaited guidelines providing SMSF trustees with suggested ‘Safe Harbour’ loan terms on which trustees may use to structure a related party Limited Recourse Borrowing Arrangement (LRBA) consistent with dealing at arm’s length with that related party.

By implementing these “Safe Harbour” loan terms, SMSF trustees are assured by the ATO Commissioner that

..for income tax purposes, the Commissioner accepts that an LRBA structured in accordance with this Guideline is consistent with an arm’s length dealing and that the NALI provisions do not apply purelybecause of the terms of the borrowing arrangement.

It is absolutely essential that all non-bank SMSF borrowing arrangements (LRBAs) be reviewed prior now extended to 1 Jan 2017

Where has this come from?

The ATO first released and then re-issued ATO Interpretative Decisions in 2015 (ATO ID 2015/27 and ATO ID 2015/28), dealing with Non-Arm’s Length Income(NALI) derived from listed shares and real property purchased by an SMSF under an LRBA involving a related party lender – where the terms of the loan were not deemed to be on commercial terms.

These ATOIDs state that the use of a non-arm’s length LRBA gives rise to NALI in the SMSF. Broadly, the rationale for this view is that the income derived from an investment that was purchased using a related party LRBA, where the terms of the loan are more favorable to the SMSF, is more than the income the fund would have derived if it had otherwise being dealing on an arm’s length basis.

NALI is taxed at the top marginal tax rate, currently 47% – regardless of whether the income is derived while the fund is in accumulation phase where tax is normally 15% or in pension phase when the income would usually be tax exempt.

After that bombshell, the ATO announced that it would not take proactive compliance action from a NALI perspective against an SMSF trustee where an existing non-commercial related party LRBA was already in place, as long as such an LRBA was brought onto commercial terms or wound up by 30 June 2016.

The Nitty Gritty Details of the Safe Harbour Steps

The ATO has issued Practical Compliance Guideline PCG 2016/5. As a result, provided an SMSF trustee follows these guidelines in good faith, they can be assured that (for income tax compliance purposes) their arrangement will be taken to be consistent with an arm’s length dealing.

The ‘Safe Harbour’ provisions are for any non-bank LRBA entered into before 30 June 2016, and also those that will be entered into after 30 June 2016.

Broadly, this PCG outlines two ‘Safe Harbours’. These Safe Harbours provide the terms on which SMSF trustees may structure their LRBAs. An LRBA structured in accordance with the relevant Safe Harbour will be deemed to be consistent with an arm’s length dealing and the NALI provisions will not apply due merely to of the terms of the borrowing arrangement.

The terms of the borrowing under the LRBA must be established and maintained throughout the duration of the LRBA in accordance with the guidelines provided.

Safe Harbour 1

Safe Harbour 2

Asset Type

Investment in Real Property

Investment in a collection of Listed Shares or Units

Interest RateNote: as of 10 Jan 2019: The RBA no longer round the rates to the nearest 5 basis points.

RBA Indicator Lending Rates for banks providing standard variable housing loans for investors. Use the May rate immediately preceding the tax year. (2015/16 year = 5.75%)(2016-17 year = 5.65%)(2017-18 year = 5.8%)(2018-19 year = 5.8%)(2019-2020 year = 5.94%)(2020-2021 year = 5.1%) (2021-2022 year = 5.1%)(2022-2023 year = 5.35%)2024 FY = 8.85% (2024-25 year = 9.35%) (2025-26 year 8.95%)

Same as Real Property + a margin of 2%

Fixed / Variable

Interest rate may be fixed or variable.

Interest rate may be fixed or variable.

Term of Loan

Variable interest rate loans:Original loan – 15 year maximum loan term (both residential and commercial).Re-financing – maximum loan term is 15 years less the duration(s) of any previous loan(s) in respect of the asset (for both residential and commercial).Fixed interest rate loan:

Rate may be fixed for a maximum period of 5 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 5.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 5 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

Variable interest rate loans:Original loan – 7 year maximum loan term.Re-financing – maximum loan term is 7 years less the duration(s) of any previous loan(s) in respect of the collection of assets.Fixed interest rate loan:

Rate may be fixed up to for a maximum period of 3 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 7 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 7.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 3 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan cannot exceed 7 years.

Loan-Value –RatioLVR

Maximum 70% LVR for both commercial & residential property. Total LVR of 70% if more than one loan.

Maximum 50% LVR.Total LVR of 50% if more than one loan.

Security

A registered mortgage over the property.

A registered charge/mortgage or similar security (that provides security for loans for such assets).

Personal Guarantee

Not required

Not required

Nature & frequency of repayments

Each repayment is to be both principal and interest.Repayments to be made monthly.

Each repayment is to be both principal and interest.Repayments to be made monthly.

Loan Agreement

A written and executed loan agreement is required.

A written and executed loan agreement is required.

Information sourced from Practical Compliance Guidelines PCG 2016/5.

Potential Trap to be aware of: Importantly, as part of this announcement, the ATO also indicated that the amount of principal and interest payments actually made with respect to a borrowing under an LRBA for the year ended 30 June 2016 must be in accordance with terms that are consistent with an arm’s length dealing.Information sourced from Practical Compliance Guidelines PCG 2016/5.

For the 2017-18 and 2018-19 years the rate is 5.8%

For the 2019-20 year the rate is 5.94%

For the 2020-21 year the rate is 5.1%

For the 2021-22 year the rate is 5.1%

For the 2022-23 year the rate is 5.35%

For the 2023-24 year the rate is 8.85%

For the 2024-25 year the rate is 9.35% until 30 June 2025

For the 2025-26 year the rate is 8.95%

For 2019-20 and later years, the rate published for May (the rate for the month of May immediately prior to the start of the relevant financial year)

It is the applicable rate under Column H of the above spreadsheet (click on link). The rate seems to have started in August 2015 but I assume we must use the May rate from now on.

In referencing the Indicator Rate you can use: Ref: Title: Lending rates; Housing loans; Banks; Variable; Standard; Investor Lending rates; Housing loans; Banks; Variable; Standard; Investor Frequency: Monthly Units: Per cent per annum Source RBA Publication Date 04-Apr-2016 Series ID: FILRHLBVSI

A complying SMSF borrowed money under an LRBA, using the funds to acquire commercial property valued at $500,000 on 1 July 2011.

The borrower is the SMSF trustee.

The lender is an SMSF member’s father (a related party).

A holding trust has been established, and the holding trust trustee is the legal owner of the property until the borrowing is repaid.

The loan has the following features:

the total amount borrowed is $500,000

the SMSF met all the costs associated with purchasing the property from existing fund assets.

the loan is interest free

the principal is repayable at the end of the term of the loan, but may be repaid earlier if the SMSF chooses to do so

the term of the loan is 25 years

the lender’s recourse against the SMSF is limited to the rights relating to the property held in the holding trust, and

the loan agreement is in writing.

We do not consider that this LRBA has been established or maintained on arm’s length terms. The income earned from the property, which is rented to an unrelated party, may give rise to NALI.

At 1 July 2015, the property was valued at $643,000, and the SMSF has not repaid any of the principal since the loan commenced.

If after considering TD 2016/16, it is determined that the income earned from the property is in fact NALI, to avoid having to report NALI for the 2015-16 year (and prior years) the Fund has a number of options.

Option 1 – Alter the terms of the loan to meet guidelines

The SMSF and the lender could alter the terms of the loan arrangement to meet Safe Harbour 1 (for real property).

To bring the terms of the loan into line with this Safe Harbour, the trustees of the SMSF must ensure that:

The 70% LVR is met (in this case, the value of the property at 1 July 2015 may be used).

Based on a property valuation of $643,000 at 1 July 2015, the maximum the SMSF can borrow is $450,100. The SMSF needs to repay $49,900 of principal as soon as practical before 30 June 2016.

The loan term cannot exceed 11 years from 1 July 2015.

The SMSF must recognise that the loan commenced 4 years earlier. An additional 11 years would not exceed the maximum 15 year term.

The SMSF can use a variable interest rate. Alternatively, it can alter the terms of the loan to use a fixed rate of interest for a period that ensures the total period for which the rate of interest is fixed does not exceed 5 years. The loan must convert to a variable interest rate loan at the end of the nominated period.

The interest rate of 5.75% applies for 2015-16 and 5.65% p.a. applies from 1 July 2016 to 30 June 2017. The SMSF trustee must determine and pay the appropriate amount of principal and interest payable for the year. This calculation must take the opening balance of $500,000, the remaining term of 11 years, and the timing of the capital repayment, into account.

After 1 July 2016, the new LRBA must continue under terms complying with the ATO’s guidelines relating to real property at all times.

For example, the SMSF must ensure that it updates the interest rate used for the loan on 1 July each year (if variable) or as appropriate (if fixed), and make monthly principal and interest repayments accordingly.

Option 2 – Refinance through a commercial lender

The fund could refinance the LRBA with a commercial lender, extinguish the original arrangement and pay the associated costs.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant part of the 2015-16 year.

Option 3 – Payout the LRBA

The SMSF may decide to repay the loan to the related party, and bring the LRBA to an end before 30 January 2017.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and the relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant period.

Each option will have many advantages and disadvantages – so it is important to understand what the practical implications of each option are, and how physically you will approach each option. Seek specialised advice on this matter as it is not a strategy suitable for DIY implementation

Important Note to 13.22C or Unrelated Unit Trust Investors

The guidelines provided in this PCG are not applicable to an SMSF LRBA involving an investment in an unlisted company or unit trust (e.g. where a related party LRBA has been entered into to acquire a collection of units in an unrelated private trust or a 13.22C compliant trust). As such, trustees who have entered into such an arrangement will have no option but to benchmark their particular loan arrangement based on commercial loan terms, or to bring the LRBA to an end.

Please visit out SMSF Property page to get details on all available strategies for SMSF property investors.

UPDATE (Relief for those caught by Budget measures)

In a letter to an industry association, the Treasurer, Scott Morrison, has outlined transitional arrangements to allow additional non-concessional contributions above the proposed lifetime limit in certain limited circumstances. Contributions made in the following circumstances may be permitted without causing a breach of the lifetime cap:

where the trustees of a self managed superannuation fund (SMSF) have entered into a contract to purchase an asset prior to 3 May 2016 that completes after this date and non-concessional contributions were planned to be made to complete the contract of sale. Non-concessional contributions will be permitted only to allow the contract to complete provided they are within the relevant non-concessional cap that was applicable prior to Budget night, and

where additional contributions are made in order to comply with the Australian Taxation Office’s (ATO) Practical Compliance Guideline (PCG) 2016/5 related to limited recourse borrowing arrangements, provided they are made prior to 31 January 2017.

Additional non-concessional contributions made under these proposed transitional arrangements will count towards the lifetime cap, but will not result in an excess.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Click here for appointment options.

Liam Shorte B.Bus FSSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 9899 3693, Mobile: 0413 936 299

PO Box 6002, Norwest NSW 2153

U40, 8 Victoria Ave., Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

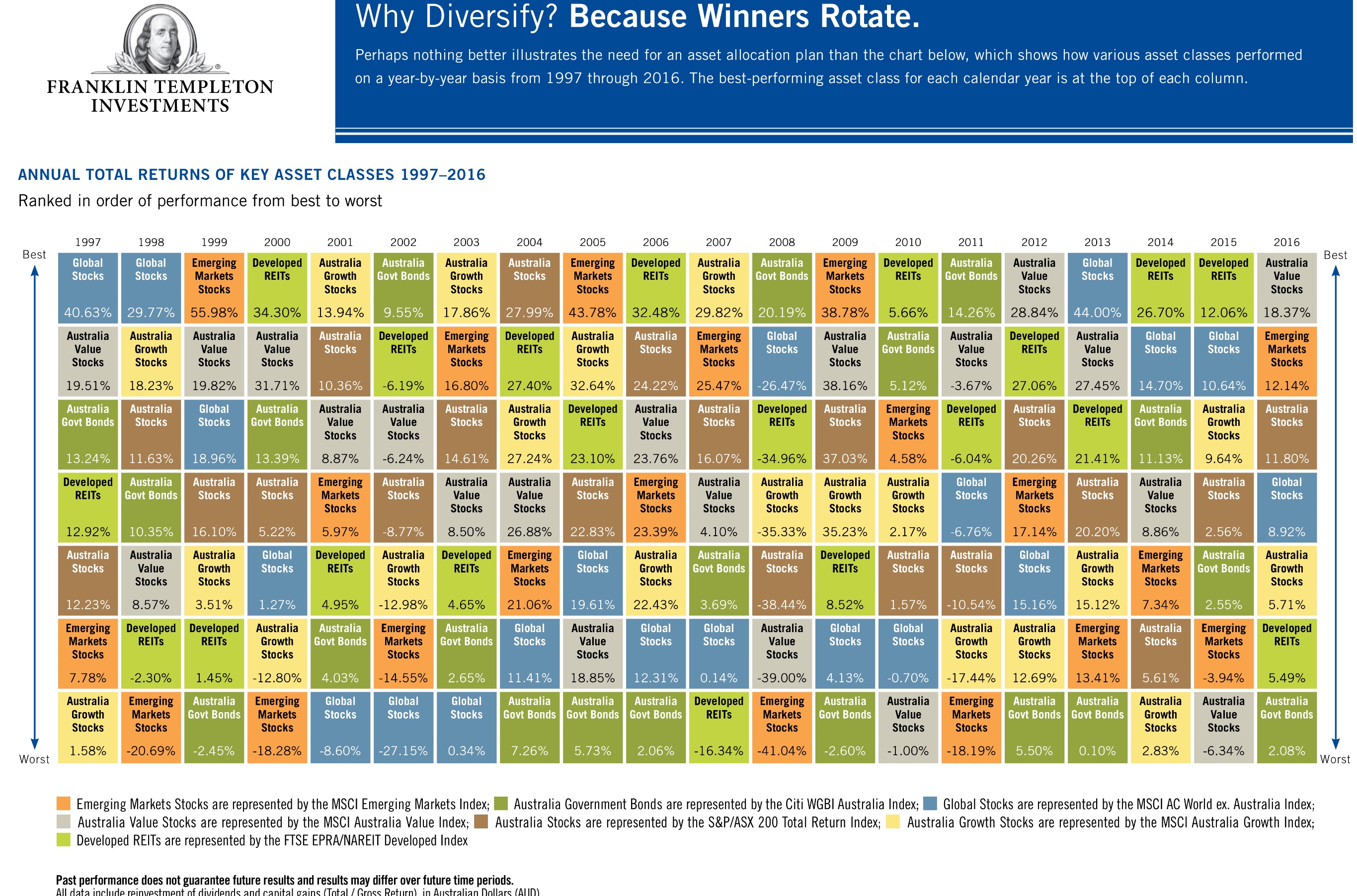

Do you know which asset sector performed best last year, the year before? Do you think those results will guide you for next year? Think again. I don’t think many SMSF Investors would have guessed Australian Listed Property would have been the strongest in 3 out of the last 4 years but in 2016 was a disappointing underperformer. Many burnt in the property sector in the GFC had avoided it like the plague and missed some of the upside.

Franklin Templeton Austalia’s annual asset class ladder for 2016 is a great tool to visualise how each asset class/sector has performed over the last 20 years and pour water on ideas that we can reliably predict next years winners.

What becomes glaringly obvious after scrutinising the table is that no single asset class consistently outperforms the others. Just in case you subscribe to the ‘last years greyhound is this years dog” or that cycles are predictable, the table shows no clues or discernible pattern into how the previous year’s winners or losers will perform in the following year as the pattern appears totally random.

We coach clients to build a diversified strategy with some tactical allocations when sectors or assets appear oversold or opportunities arise like when the Aussie dollar was getting USD $1.10 a few years back and the opportunity came to overweight international stocks.

I hope this information has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

So you have a great idea to move some assets to your SMSF but you want to stay within the rules and keep your fund compliant. Then you hit the jargon associated with Superannuation rules and regulations.

You need to understand who are “related parties” of your SMSF for two reasons, to ensure compliance with the acquisition from a related party rules and to determine the in-house assets.

A related party is defined in the Superannuation Industry Supervision) Act 1993 known as the SIS Act. This is the bible when it comes to Superannuation so you should save that link above. Anyway in the SIS Act sec 10(1) a related party is defined as:

Fund member

Standard employer-sponsor of the fund or

Part 8 associate of a fund member or a part 8 associate of a standard employer-sponsor of the fund.

Ok the first one is easy. Any member including you yourself is a related party.

Standard Employer

A standard employer sponsor of a fund is an employer who contributes to the fund due to an agreement between the employer and the trustee of the fund. These were common in the early days of SMSFs but largely non-existent now.

Where an employer only contributes to a fund due to an agreement between the member and the employer such as under a salary sacrifice arrangement, they will not be considered a standard employer sponsor.

If an SMSF has a standard employer sponsor, which would be uncommon, the relationship will be noted either in the trust deed or in an attached schedule to the deed.

Part 8 associate

Now prepare for a headache to hit you hard after reading this one.

Part 8 associates are broken down in the legislation to Part 8 associates of individuals, companies and partnerships. However, if there is no standard employer sponsor, we only need to examine the part 8 associates of the members who will always be individuals.

The part 8 associates of a member are:

a relative of the member (parent, grandparent, brother, sister, uncle, aunt, nephew, niece, linear descendant or adopted child of the member or their spouse or a spouse of the aforementioned)

other members of the SMSF (a person who is not a member but acting as individual trustee or director under an Enduring Power of Attorney is not necessarily a Part 8 associate)

a partner of the member (legal partnership, not ‘business partners’ i.e. company directors) and their spouses and children

the trustee of a trust the member controls and