Another of our background articles on the basics of implementing Self Managed Super Fund strategies in plain English.

There are a number of reasons why you may decide to establish a pension from your SMSF but we believe everyone over 55 should at least consider one and the majority of people over 60 would be hard pressed to give a decent reason why not to use one.

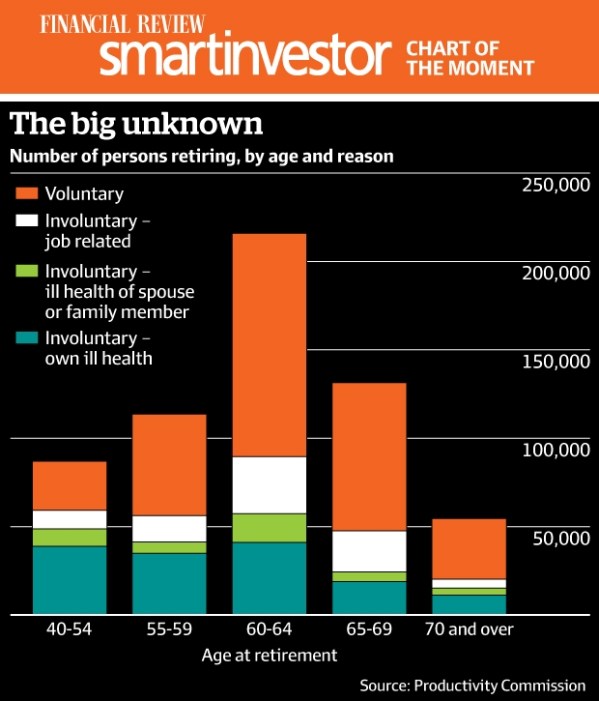

The usual reasons for members to move into pension phase (proper name is Account Based Pension) include:

- Cutting back hours and using a Transition to Retirement Pension to make up for lost income (see our blog on Transition to Retirement pensions)

- Pre-retirement tax minimisation strategies via a Transition to Retirement Pension;

- Full Retirement;

- Incapacity (Temporary or Total and Permanent) due to illness or injury; or

- You need additional funds to meet your increased living and medical expenses as you age.

The main reason someone would not start a pension is that they are still 55-59 and already contributing up to their contribution limits and do not need the cash to meet their current living expenses. In this case they may incur tax on the pension that outweighs the benefits or may affect Centrelink benefits of an older spouse. Otherwise the main reason is someone who does not need the funds and is over 65 and would like to retain the full balance of the capital and earnings in superannuation environment and the 15% tax on earnings is not an obstacle (yes there are some for whom this is suitable).

So what is an Account Based Pension?

When you are contributing to super, you are in ‘Accumulation’ phase. Essentially all contributions and earnings in the fund are allocated to your member’s Accumulation account. This money then remains preserved until you satisfy a “condition of release” (Ok let’s explain this jargon).

“Condition of release”

A condition of release is a nominated event that the member must satisfy to be able to withdraw benefits from their superannuation fund such as:

- Reaching preservation age (55 for people born before 01/071960 and rising incrementally to 60 for those before 30/06/1964 with 60 for all born after 01/07/1964)

- Permanent retirement from the workforce on or after your preservation age

- Termination of employment after turning age 60 (without necessarily retiring permanently)

- Reaching age 65 (whether you are retired or not)

- Permanent incapacity

- Diagnosis of a terminal medical condition

- Severe financial hardship

- Eligibility for approval on compassionate grounds

- Satisfying any other condition of release as specified in superannuation law.

Once you have satisfied a condition of release your benefits become reclassified to unrestricted non-preserved and the member has the option of starting an income stream via a pension with all or part of their account balance

If you decide to establish a pension with your account, the balance is now referred to as being in ‘pension phase’. This means that no further contributions can be made into this account. Don’t panic! SMSF members often have an accumulation account (to contribute to) and a pension account (to withdraw from) at the same time.

Benefits of setting up a pension

Account Balance moves to Tax free status (Everyone understands Tax Free!!!!!)

While you are in accumulation phase, the fund will pay 15% tax on all contributions and taxable income within the fund. The real benefit in my opinion for you moving into pension phase as early as possible is that the portion of the fund supporting the pension also moves into a tax-free environment. This means that there is no tax to pay on any income or capital gains from the assets supporting the pension. So if you and your younger spouse had 50/50 balances in the fund and you went in to pension phase then you could expect approximately 50% of the earnings to be tax-free.

Tax free pension income stream (like a tax haven but in Australia!)

For members receiving SMSF pension payments from the age of 60 onwards, there is no requirement to report the pension in your personal tax return. This means that all pension and indeed Lump Sum withdrawals from your self-managed super fund are tax-free! Yes, that often means that you will no longer need to do a tax return at all if your other earnings are low. For those 55-59 the pension can be very tax effective if combined with salary sacrifice a s you receive a 15% Pension Tax offset.

Refund of franking credits – the Sweetener!

Franking credits also known as imputation credits represent the local tax paid by Australian companies on their earnings (currently 30%) and are attached to franked dividends. These credits are fully refundable to superannuation funds in pension phase. Usually they are used to offset any tax liabilities the fund has, however for a fund fully in pension phase, the income is no longer taxable, so no tax liability and the franking credits will be refunded in cash to the fund. This can lead to an improvement in your returns by up to 30% on the earnings of blue chip shares in your fund. This is why the fully franked dividends of companies like Telstra, Westpac and Woolies have become known as the “Pensioners Friend”. See this article for a full explanation of The added value of franking credits in a SMSF Portfolio

Control of amounts and timing of payments

As long as the minimum payment requirements of the pension are met, the member can control how much pension they will withdraw as well as the timing of those payments. We often structure payments to match how the client received their pay while working, be it fortnightly, monthly or for some half-yearly or annually if they had other regular income to cover living expenses.

What is required to set up the Pension in a SMSF?

All you need to do is organise a Pension Kit with your advisor or administrator.

The Pension Kit document package for a SMSF Pension set up includes:

- Application form – from fund member to fund trustee(s) requesting a pension and the details like the chosen start date and where to be paid and when;

- Minutes of the fund trustee(s) agreeing to pay the pension, often agreeing to the pension from the request date but delaying the issue of the final documents until the annual financials have been prepared;

- The Pension Payment Agreement containing the rules under which the pension will be paid;

- A Product Disclosure Statement summarising the features of the Pension (rules and regulations basically);

- A cover letter explaining what to do next as far as making the payments.

Why not click here to Schedule a Meeting by phone, face to face or via Skype if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or online via Skype.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

![]()

![]()

![]()

![]()

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.