Plenty out there in the media about the results of the Big 4 Aussie Banks, CBA, NAB , Westpac and ANZ. As this is an education blog I always like to see how the global fund managers (with a strong Aussie equities team) view our banks as they do not tend to have that home country bias and their views are refreshing. So here are a few videos from the team at Franklin Templeton. Not plugging their product just like their educational material and market insights.

As the Australian banking sector continues to experience challenges in response to market and regulatory drivers, we thought it would be timely to catch up with Alastair Hunter, Lead Analyst and Investment Manager at Balanced Equity Management (owned by Franklin Templeton Investments) for his latest perspectives on the Australian banking sector.

Here Alastair talks us through the key factors he identifies as driving bank share prices from capital requirements through to dividend sustainability, and the Franklin Templeton team’s preferred overweights in the sector.

Impact of Brexit and FinTech on Australian Banks – Watch Video(4:54)

In this video, Alastair discusses the direct and indirect impacts on the sector from the Brexit referendum and some of the potential ramifications for bank funding costs from changing dynamics in international markets. He also considers some of the factors impacting on the sector from new Fintech entrants and how the banks may adopt new technologies to drive innovation for their benefit.

Disclaimer: Franklin Templeton Investments Australia Limited (ABN 87 006 972 247) (Australian Financial Services Licence Holder No. 225328) issues this publication for information purposes only and not investment or financial product advice. It expresses no views as to the suitability of the services or other matters described herein to the individual circumstances, objectives, financial situation, or needs of any recipient. You should assess whether the information is appropriate for you and consider obtaining independent taxation, legal, financial or other professional advice before making an investment decision. A Product Disclosure Statement (PDS) for any Franklin Templeton funds is available from Franklin Templeton at Level 19, 101 Collins Street, Melbourne, Victoria, 3000 or www.franklintempleton.com.au or by calling 1800 673 776. The PDS should be considered before making an investment decision.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

The old adage “if it sounds too good to be true then it usually is” holds firm especially with superannuation “release” schemes. The ATO is stepping up its education efforts to help consumers while clamping down on promoters of such schemes. Here at SMSF Coach and our sister firm Verante Financial Planning we are always willing to offer a second opinion on any recommendation you are concerned about.

The Australian Taxation Office (ATO) is extending a helping hand to pre-retirees through Super Scheme Smart, a new initiative launched recently that educates people on the dangers of risky and illegal retirement planning schemes.

The ATO has identified a significant number of retirement planning schemes designed solely to help people avoid paying tax on their assets in an illegal manner and is working to close these down.

From the ATO media video below with ATO Deputy Commissioner, Michael Cranston, he warns:

While retirement planning schemes can vary, there are some common features that people should be aware of. Usually these schemes:

• are artificially contrived and complex, usually connected with a SMSF

• involve a lot of paper shuffling

• are designed to leave the taxpayer with minimal or zero tax, or even a tax refund

• aim to give a present day tax benefit by adopting the arrangement

Individuals caught using an illegal scheme identified by the ATO may incur severe penalties under tax laws. This includes risking loss of their retirement nest egg and also their rights as a trustee to manage and operate a SMSF.

The ATO is delivering practical help and information through their Super Scheme Smart website, including a comprehensive information pack, case studies and videos, as well as sending taxpayer alerts into the community about schemes and why they don’t fit within the law.

Mr Cranston urged people undertaking retirement planning to remain vigilant and to come forward if they believe they are at risk or are already involved in a scheme.

“Retirement planning makes good sense provided it is carried out within the tax and superannuation laws. Make sure you are receiving ethical professional advice when undertaking retirement planning, and if in doubt, seek a second opinion from an independent, trusted and reputable expert.

“We do our best to shut down dodgy schemes but the best defence is working together. Blowing the whistle on those promoting retirement planning schemes will help us stop them from risking your or others’ retirement savings,” Mr Cranston said.

All those approaching retirement who are yet to get “Super Scheme Smart”, are encouraged to take advantage of these resources and report promoters of dodgy schemes by calling 1800 177 006, or via email to reportataxscheme@ato.gov.au

Some examples provided of the current schemes they are concerned about include:

The schemes the ATO are currently worried about include:

Dividend stripping – Where the shareholders in a private company transfer ownership of their shares to a related SMSF so that the company can pay franked dividends to the SMSF. The purpose being to strip profits from the company in a tax-free form. (refer to Taxpayer Alert (TA 2015/1))

Non-arm’s length limited recourse borrowing arrangements – When an SMSF trustee undertakes limited recourse borrowing arrangements (LRBAs) established or maintained on terms that are not consistent with an arm’s length dealing. For more information, see Practical Compliance Guide.

Personal services income – Where an individual (with an SMSF often in pension phase) diverts income earned from personal services to the SMSF where it is concessionally taxed or treated as exempt from tax (refer to Taxpayer Alert (TA 2016/6)).

As mentioned above at Verante Financial Planning we take very good care of our clients and ensure all our client strategies are fully compliant and tick all the boxes so our client can sleep securely at night know that while they have used the superannuation and tax systems to maximise their savings position, they are always within the regulations and the spirit of the law.

The whole focus of this blog, the SMSF Coach is about educating and promoting use of legal strategies and we are consistently warning people of the pitfalls of some strategies and investments out there such as our recent warning on the failed GUEVRA IPO not being suitable for SMSF clients or our very popular Property through super in a SMSF – Part 3: 20 most common mistakes

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Let’s start with a definition of what is an Enduring Power of Attorney (EPoA).

An enduring power of attorney is a legal agreement that enables a person to appoint a trusted person – or people – to make financial and/or property decisions on their behalf. An enduring power of attorney is an agreement made by choice that can be executed by anyone over the age of 18, who has full legal capacity.

We make decisions for ourselves on a range of family, work and lifestyle issues everyday and often we are reluctant to admit that there may come a time when we may no longer be able to do so. People don’t like to think about becoming mentally incapacitated by illnesses such as Alzheimer’s or dementia, or becoming physically or mentally incapacitated as the result of an illness or accident. But if it does occur it is vital there is a vehicle in place allowing someone else to legally make decisions.

If we have legal documents prepared prior to us losing capacity to make them, our decisions can be made by someone we know and trust. If we do not have those documents in place before we lose capacity then decisions may have to be made by a government department set up for the purpose of dealing with financial and personal affairs of an incapacitated person.

Most of us given the choice would probably choose the first one but to do this we need to make the documents whilst we have the mental capacity to make them. A person has capacity to make valid legal documents if they can understand why they are making the document and the choices which may be involved (choosing a person to act for you). You must be able to weigh up the result of giving power to someone else to act for you and you must be able to communicate your decision to make a legal document.

The main reason why we have legal documents giving a person or persons the power to act for us is that they will know our wishes and preferences and will act in our best interests. It is also a cost-effective way of protecting our family, finances and assets.

So why is it important for an SMSF member to have an EPoA

Well except in very limited circumstances, a self managed superannuation fund will only qualify as an SMSF where each member of the fund is either a trustee of the fund or a director of the fund’s corporate trustee. It is because of this threshold requirement for existence as an SMSF that the EPoA becomes a very important document for the SMSF member.

Consider the implications for the SMSF if someone is incapable of making decisions:

How does the SMSF run?

How can documents be executed?

How does a corporate trustee operate?

How can a new trustee appointed?

How will assets be bought or sold?

How are pensions or lump sum withdrawals approved and facilitated?

If there isn’t an EPoA what can happen?

Documents requiring two signatures, can’t be executed

Possible Audit contravention

The ATO may render the fund non-complying

Cannot roll-out an incapacitated member as SIS regulations require member consent (can’t be given if incapacitated)

Apply to QCAT, VCAT, NCAT, SAT(for WA) – Civil and Administrative Tribunal

Apply for guardianship

But who will they appoint? Surviving spouse, son/daughter, Public Trustee?

Do you think the Public Trustee wants to be running a SMSF?

What happens to the SMSF while waiting?

Technical Part (I don’t like to quote reams of legislation but sometimes it is necessary)

Subsection 17A(3) if the Superannuation Industry (Supervision) Act 1993 (SISA) provides that an SMSF will continue to be an SMSF where, amongst other things:

(b) the legal personal representative of a member of the fund is a trustee of the fund or a director of a body corporate that is the trustee of the fund, in place of the member, during any period when:

(i) the member of the fund is under a legal disability; or

(ii) the legal personal representative has an enduring power of attorney in respect of the member of the fund;

The term “legal personal representative” is defined at subsection 10(1) of the SISA as follows:

… the executor of the will or administrator of the estate of a deceased person, the trustee of the estate of a person under a legal disability or a person who holds an enduring power of attorney granted by a person.

So, in short, under the superannuation legislation:

the enduring power of attorney is the key to allowing a fund to continue to qualify as an SMSF notwithstanding that the member may not be acting as trustee of the fund;

the enduring power of attorney “relief” can be invoked to assist not only when the member is under a legal disability.

However, as also evident from the above, the fact of the EPoA being drawn up, properly signed and sitting in someone’s drawer is not enough.

Implementing the exercise of the EPoA with your SMSF

In order to meet the requirements set out in the Superannuation Industry (Supervision) Act and the Self Managed Superannuation Funds Ruling SMSFR 2010/2, the following conditions must be satisfied:

The LPR/EPoA must be appointed as a trustee of the SMSF, or as a director of the corporate trustee of the SMSF. The appointment of the LPR/EPoA must be in accordance with the trust deed, the constitution of the trustee company (if any), the Superannuation Industry (Supervision) Act, and any other relevant legislation (such as the Powers of Attorney Act 1998 (Qld), the Guardianship and Administration Act 1990 (WA) and the Corporations Act 2001 (Cth)).

A member who has lost capacity must cease to be a trustee of the SMSF or a director of the corporate trustee upon the appointment of their LPR.

Where the EPoA appoints multiple attorneys, one or more of those attorneys can be appointed as trustee or as director of the corporate trustee in place of the member.

Similarly, multiple members are able to execute an EPoA for the same LPR, who can be appointed as a trustee or a director of the corporate trustee in place of each of those members.

A member is also able to execute an EPoA in favour of an existing member who is a trustee or director of the corporate trustee. In this case, the incapable member can cease to be a trustee, or director of a corporate trustee, and their LPR, already a trustee or director in their own capacity, will also be considered to be appointed in the capacity as LPR for the incapable member.

Acting as a trustee under the EPOA

Once appointed, the attorney performs their duties as trustee or director of the trustee company as a trustee or a director rather than as attorney or agent for the member. The attorney will be subject to the obligations of a trustee and must sign the trustee declaration stating that they understand their duties as a trustee. The attorney cannot be a disqualified person and must be eligible to be appointed as trustee.

The decision to act as an attorney and the legal duties are significant. The attorney must:

Consider the interests of the donor when making decisions as the attorney;

Take care of property/assets;

Avoid conflicts of interest;

Comply with relevant legislation, and

If necessary, prove that they have been appointed your attorney.

In summary

While the decision to grant an EP0A should not be taken lightly, it is an important document which all adult Australian’s should have in place, but it is particularly vital that every adult who is a member of a SMSF execute a valid EPoA. Failing to have an EPoA can result in delays or a financial disaster if a member loses capacity. Having an EPoA will ensure that upon the loss of capacity of a member, the fund can continue to be a complying SMSF.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Well this blog is not about Self Managed Super Funds but is about a matter close to the hearts of many of my clients. As a parent or grandparent, ensuring that children receive a good education is one of the most common concerns raised with us at Verante. Many people want to leave provision in their wills for such costs so here is one of our preferred strategies.

You can establish a dedicated education fund through a testamentary trust in your Will. This is a tax-effective and flexible way to provide for the education of your children or grandchildren. It can also help to ensure that the funds you want to be applied for their education are preserved and not misused by young beneficiaries or caught up in the complications caused by the rise of complicated blended families (his, hers and ours issues).

If you are a grandparent, leaving bequests via a testamentary trust for payment of education fees and related costs for your grandchildren is a more tax effective method of providing for their education rather than leaving additional bequests to their parents that may be caught up in marriage breakdowns, business bankruptcy or litigation.

What is a testamentary trust?

In general, a trust describes an ownership structure where the assets of the trust are held by a person or organisation (the trustee) for the benefit of other individuals or organisations (the beneficiaries).

A testamentary trust is a trust that is created within and by your Will. You need to arrange it as part of your Will making but it only comes in to effect on your death.

A testamentary trust may be created using specified assets, a designated portion of your estate or the entire remaining balance of your estate. Multiple trusts may be created by the one Will.

Normally the Trustee of this trust will be the executor of your estate, a surviving spouse or sibling of the deceased. You also have the option of appointing an Independent trustee company. Often this trustee will step down when the beneficiary reaches a target age or completes their education.

What is an education fund?

Assets inherited directly by your beneficiaries become part of their personal assets and are under their control. The future of these assets depends on the beneficiary’s ability to manage their own financial affairs, with no guarantee that the assets will be applied for any particular purpose, such as their education.

An education fund is a trust which focuses on funding the education of a particular beneficiary (the ‘primary beneficiary’). It gives you assurance that the income of the trust will be directed to the educational and other purposes you have specified in your Will.

You set the terms of the testamentary trust in your will. These terms can restrict the ability of any of the beneficiaries to control the activities and investments of the trust or give them complete control. You are in effect choosing to ‘rule from the grave’ to ensure that the inherited assets are protected and used sensibly for the benefit of the primary beneficiary

How does an education fund operate?

The typical features included in an education fund are:

The trust can be funded by your some or all of your assets and by payments in consequence of your death such as superannuation death benefits or insurance proceeds paid to your estate.

A proportion of your estate is held on trust until the primary beneficiary (child/children) achieves a particular level of education or satisfies other conditions established in your Will. Many of our clients choose age 25.

The trustee has the power to apply the income and capital of the trust for a variety of purposes specified in your Will for the benefit of the primary beneficiary, with the emphasis being on the educational needs of the primary beneficiary.

During the financial year, income and capital are distributed to the primary beneficiary to the extent required for the approved purposes. Any remaining income is either accumulated within the trust or distributed to other beneficiaries, as directed by the Will.

When the primary beneficiary has satisfied the conditions specified in the Will (such as attaining a particular level of education or age), they gain control of the remaining balance in the education fund and may either continue the trust or vest it (end it) at any time.

If the primary beneficiary fails to satisfy the conditions within a specified period, the trustee may determine that the remaining balance in the education fund be distributed to other beneficiaries named in the Will or held on trust for the education of those beneficiaries (or their descendants).

An education fund will normally be a mandatory trust imposed upon the beneficiary due to your desire that they continue their education to a specified level. The beneficiary will not normally be given the option of terminating the trust or eventually inheriting the trust without satisfying specified conditions.

Example

George and Helen have a combined estate worth $1,500,000. They have three young grandchildren whom they wish to make their beneficiaries as they had already helped their children to set themselves up as financially secure.

George and Helen are concerned that, in the event of their deaths, their grandchildren will not be sufficiently mature to use their inheritance responsibly. They wish to establish an education fund to ensure that the grandchildren are encouraged to further their education, but are also adequately provided for during their developing years.

As a result, George and Helen’s Wills provide that 50 per cent of the inheritance received by a child ($250,000 each) will be held in testamentary trust funds on the following terms:

Until the beneficiary turns 25, their access to the income and capital of the trust is limited to specified purposes, such as:

education expenses, including HECS liabilities

hospital and medical expenses

rent or accommodation charges

electricity, gas and other utility payments

maintenance and income support at the discretion of the trustee.

If a specified level of tertiary education has been completed by the age of 25, the beneficiary will be given full control of the trust at the time of attaining that educational level, with the ability to either continue the trust for tax planning purposes (as a tax-effective vehicle for supporting the education of their own children) or terminate it.

If the beneficiary does not attain the required level of education by the age of 25, the remaining balance of the education fund will be distributed amongst charities specified in the Wills.

The education funds will ensure that each child is adequately supported, but also given an incentive to further their education. If all children were from the one family you could use just one Trust.

Additional issues to discuss with your legal expert

Common areas which require further thought are:-

Whether to have one or several Trusts established under the Will

The selection of the appropriate trustee or trustees

The method of appointing replacement trustees

Whether some classes of beneficiaries are restricted to income and some to capital

Back-up Strategy

There is a second chance for your family to establish a testamentary trust after you die but this second chance must be taken advantage of within three years of your death. This enables a trust to be established from your assets and for the income to enjoy the same tax advantages as income derived through a testamentary trust. However, the assets used to establish the trust cannot exceed the amount which the beneficiary would have received under the law, if you died without a Will.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options or get a referral do a recommended Estate Planning solicitor. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

OK, It has happened. I always worried that British pride and fear of immigration would lead to this outcome. So where to from here? What does it mean for SMSF Investors?

The situation is unprecedented and there is no verified or tested procedure for EU exit. This means there is uncertainty as to what happens next. You can expect that:

Article 50 of the EU constitution – the law governing the process of the UK’s divorce from the EU – will be triggered

This will kick-start the formal two-year process determining the terms of the UK’s EU exit, including the shape of its future access to the EU Single Market

There will be significant pressure on Prime Minister David Cameron to resign (Update: that has happened) and for Scotland to review its position within the UK

In the short run, Self Managed Superannuation Fund investors can expect:

Shock to investor confidence and increased asset price volatility primarily in the EU but also with Aussie companies who have exposure to that region especially the UK (BTT, CYBG, Henderson, HVN, IRESS)

This vote combined with global economic conditions, high asset valuations, our election next month and the progress towards the U.S. election in November will all likely contribute to volatility through the second half of the year.

Further strength in the Aussie Dollar short-term and declines in the pound (time to pay in advance for the UK trip of a lifetime!)

Downward pressure on equities, especially financial sector stocks and companies with overseas earnings. Time to buy the world at a discount. If not confident then look to great proven managers like Magellan and Platinum to pick the opportunities and ETFs from Vanguard, Ishares, State Street and Betashares for core or sector specific exposure.

Flight to safety will see USD and GOLD seen as safe havens. We can point you to the right people if interested in Bullion

Upward pressure on corporate bond yields owing to increased uncertainty and the worsening short term growth outlook – as with equities, the financial sector is most

exposed. Look to proven managers in this fixed interest and credit space like Vimal Gor at BT Investment Management to guide you.

Modest declines in-house prices are possible, as our banks may find it harder to raise overseas debt and therefore pass on increased costs to borrowers and hence curtail new purchases.

The leave vote will create short-term volatility and hurt growth prospects as markets deal with increased uncertainty. Inevitably however, the increased volatility should open up potential opportunities to benefit tactically through buying of those companies and assets that show solid traits of being well capitalised and with good management that should be able to best withstand the uncertainty. In a nutshell you will get a one-off opportunity to buy quality assets as a discount but you must search for quality among the chaff.

From time to time, as with the Greek debt Crisis, equity markets experience heightened, event-related volatility. A good adviser will ensure that you focus on your long-term goals and understand:

Volatility is a normal part of long-term investing and equity returns premium revolve around getting higher than cash returns for accepting that volatility.

Avoid being swayed by media hype and overly negative sentiment.

SMSF trustees and other long-term investors are usually rewarded for taking additional equity risk when there is “blood on the streets”

Market corrections can create attractive opportunities to buy quality assets at a discount. Afraid to pick sectors then use a multi-manager like Russell Investments to spread the risk

Some active investment can help navigation in periods of increased volatility. That is why we at Verante believe in passive/active blended portfolio design

So what to do?

Make sure you have some cash ready for purchases

Review your portfolio for any stocks or assets over exposed to Europe and seek research or comment on them

Wait for some sign of the market bottoming and take small and targeted purchases in discounted sectors without getting carried away.

Research , research and more research or outsource / work with SMSF specialist advisors like us who have made the contacts and done the leg work in portfolio design.

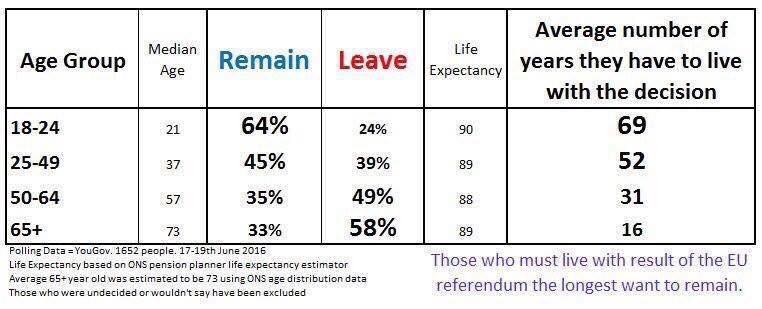

Finally a table that sums up the fact that those who have to live with this decision were against it.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

As an SMSF Specialist and Financial Planner I do not pretend to my clients that I am an investment guru or that I can tell what will be the next big thing!. I believe my job is to guide them in portfolio construction and advise on diversification while bringing up opportunities to their attention that they may not have considered. This includes some IPO’s and in the last few years I have supported HPI, MPL, QVE, BWP, PIC and avoided some I just couldn’t see long-term value in like MYR, Dick Smith (DSH), McGrath (MEA). I never call them all right but I do limit what clients invest in each to what they can afford to lose.

I did not make these decisions for my clients on my own. I relied heavily for support on services such as our own in-house research team at Magnitude and eQR equities research, third-party research services like Morningstar, Intelligent Investor and discussions with peers and those I believe are thought leaders in the SMSF and Investment space. See the Twitter list here

So when I saw the Guvera IPO come up and having followed them from about 2 years ago when I signed up to their beta service it tweaked my interest. But once I had done my own research and read what others had provided I decided this was a no go area for any SMSF client looking to build wealth for retirement as superannuation is intended.

The figures spoke for themselves. $1.2 million in revenue on a $81.1 million loss and a failed attempt to raise money from size-able seed investors. Believe me there are many sources of venture and angel capital funds out there for good start-up ventures with potential so when an idea has good prospects it will receive support and at such an early stage in its life it should not be seeking a listing on the ASX as it has not proved itself.

I struggle to see how a responsible advisor could recommend a IPO like Guvera’s to many SMSF investors let alone 3000 of them. It appears that the main fund-raiser for this IPO is promoting it via related Accounting firms and rumours of SMSFs being set up just to invest in this IPO as their only current asset. I also question if Accountants and Advisers who have become promoters of this IPO are receiving options or referral fees and assume that they are fully disclosing these to clients who must trust them for guidance. I question whether post July 2016 when Accountants’s will be legally obliged to provide Statements of Advice under a Best Interest’s duty and fully outlining the terms and risks on a personal basis for a client or their SMSF if such an investment could be as targeted to SMSFs.

Its not just me, the Australian Shareholders Association raise concerns about Guvera on Ross Greenwood’s show on 2GB. Listen here for the podcast. http://www.2gb.com/audioplayer/182331

This type of venture is a very, very highly speculative investment suitable for no more than 1-5% of the most aggressive of investors portfolios so I do not believe it should be promoted by private equity through accounting firms or financial planning firms to their SMSF clients. I will call it now as possibly the next Trio or WestPoint.

So that’s my call and guidance I have given to my clients. What are your thoughts? Am I becoming an old fuddy-duddy with no eye to the potential future of this firm?

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Ok so as SMSF trustees you are obliged to consider insurance for members but you might think you don’t need it or that you can manage risks. Here is a light-hearted look at some reasons why you might need to reconsider that decision.

Cats have 9 lives. You don’t. Enough said.

Cats get a free ride. You pay the rent/mortgage. Living in an lane way or the bush might work for a feral feline, but for your family, not so much. Your rent or mortgage still needs to be paid regardless of illness, injury or death.

Cats can hunt. You can barely handle the line at the Woolies.

Stalking prey for dinner is not an option. Your family needs cash to put food on the table.

Kittens move out at 8 weeks. Your kids may still be at home when they’re 25..30..and back again at 45 with a few kids in tow!

Your kids may leave for uni at 18, but they could be freeloading off your parental generosity well past their studying years…focusing on becoming an “entrepreneur”, an “artist” or just “finding themselves”.

Cats always land on their feet. You need a safety net. Life on the edge might be thrilling for you, but a nightmare for your family.

Cover your life and your income. Protect your family’s most important asset—you and your earning capacity (unless, of course, you’re a cat).

Contact us to figure out the life and income protection insurance you need.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I am breaking the Budget down in to bite size chunks with strategies to consider going forward for SMSF Trustees. The first part which dealt with pension strategies is available here . This second part deals with changes to contribution options, methods and caps.

Before I go into detail here is a summary of the changes that are relevant to SMSF members (No coverage of Defined Benefit Schemes in this article):

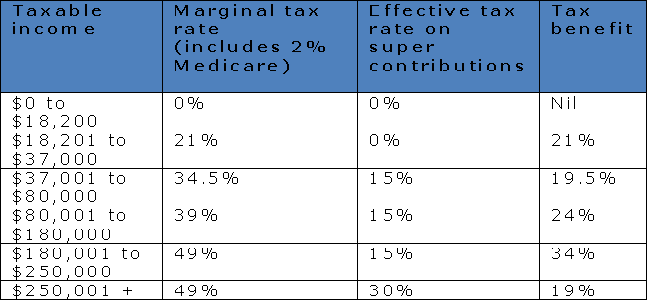

Concessional (Pre-Tax Contributions like employer superannuation guarantee (SGC), salary sacrifice and those contributions where you claim a tax deduction).

Reduction in the concessional contribution cap to $25,000 regardless of age

Carried forward concessional cap for account balances below $500,000 from 1 July 2018

All individuals under 65 will be eligible to claim a tax deduction for personal contributions (bye bye 10% rule). work test applies ot over those 65

Reduction in income threshold to $250,000 where additional super contribution tax applies

Reduction in contribution tax for people earning less than $37,000

Extension of low-income spouse contribution tax offset

Non-Concessional (Post Tax Contribution like personal after tax contributions and Government co-contributions).

Reduction in Non-concessional contribution cap limit to $100 per annum

Reduction of existing annual non-concessional bring forward provisions

Now the detail:

Reduction in the concessional contribution cap to $25,000 regardless of age

The concessional contribution cap will be reduced from the current level of $30,000 to $25,000from 1 July 2017, irrespective of the age of the individual. The higher cap of $35,000 that currently applies to individuals over age 50 will be abolished. The reduced cap will continue to be indexed in future years in line with wages growth.

Carried Forward or Catch-up concessional contributions

From 1 July 2018 individuals will be able to make additional concessional contributions where they have not reached their concessional contributions cap in previous years. Access to these unused cap amounts will be limited to those individuals with a superannuation balance less than $500,000. Unused amounts accrued from 1 July 2018 will be able to be carried forward on a rolling basis for a period of five consecutive years.

This measure allows some additional flexibility in the timing of your contributions like making $125,000 for a tax deduction on the sale of a property or share portfolio if you did not make contributions in the previous 4 years. Your ability to save may vary throughout your career and this measure will assist to some extent, but falls well short of my preferred option for a lifetime cap on concessional contributions. The restriction based on size of account balance will add complication to the administration of this measure when multiple funds are involved.

All individuals under 65 will be eligible to claim a tax deduction for personal contributions

From 1 July 2017, all superannuation fund members up to age 65 will be able to claim an income tax deduction for personal superannuation contributions up to the concessional contribution cap ($25,000), regardless of their employment circumstances. This is good news for people who are partially self-employed and partially wage and salary earners, and individuals whose employers do not offer salary sacrifice arrangements, as they will benefit from this proposal. Personal contributions for which a tax deduction is claimed will count towards the concessional, rather than the non-concessional cap.

While I accept the government’s intention is to increase flexibility for more people to access the concessional contribution cap if they are able to do so, the mechanism requiring individuals to notify their fund of their intention to claim a tax deduction for their personal contributions will add considerable complexity to fund administration. the “she’ll be right” and “I’ll do it later factor” will lead to many missing opportunities.

Over 65’s will still need to meet the work test.

Reduction in income threshold to $250,000 where additional super contribution tax applies

From 1 July 2017, individuals with “relevant income” greater than $250,000 will pay an additional 15 per cent tax on their concessional contributions, down from $300,000. The additional tax, referred to as “Division 293 tax” after the section of the tax legislation which governs the tax, will be payable where the individual’s taxable income (including reportable fringe benefits and certain other amounts) plus concessional contributions (excluding those that exceed the concessional contributions cap) is greater than the $250,000 threshold.

Superannuation still remains attractive despite this change, the 30% tax applied to concessional contributions is still less than the marginal tax rate on earnings so contributing to super remains attractive. But with the lower $25,000 concessional contribution there will be limited scope for you to make optional concessional contributions. For example, if you earn $250,000 and your employer pays the 9.5% SG on your full salary this is an annual employer contribution of $23,750 which has almost fully utilised the new lower cap. If you are on a higher income with disposable income you may look for alternatives outside superannuation or top up your partner/spouse’s superannuation (and potentially receive a tax offset if they earn less than $37,000).

After earlier reports that the threshold would be reduced to $180,000, the proposed threshold of $250,000 means the tax will apply to only around 1 per cent of superannuation fund members. Retention of the existing mechanism which minimises the administrative costs to superannuation funds associated with this tax is welcome.

Reduction in tax for people earning less than $37,000

From 1 July 2017, the Government will introduce a Low Income Superannuation Tax Offset (LISTO) to reduce the tax on superannuation contributions for low-income earners. The measure will apply to individuals with taxable income less than $37,000, and will effectively refund the tax on concessional contributions up to an annual cap of $500. This measure will replace the Low Income Superannuation Contribution (LISC) which was scheduled to be abolished from 1 July 2017, however, the mechanism will be slightly different. Rather than the government making a direct

contribution to the individual’s superannuation account, the offset will apply to the contribution tax deducted by the superannuation fund. The Australian Taxation Office will determine an individual’s eligibility for the LISTO and advise their superannuation fund annually. The fund will then contribute the LISTO to the individual’s account. The government will consult on the implementation of this scheme.

Extension of low-income spouse contribution tax offset

The government will increase access to the low-income spouse superannuation tax offset by raising the income threshold for the low-income spouse from $10,800 to $37,000 and phasing out up to $40,000. This arrangement provides a tax offset of 18 per cent of contributions made by the contributing spouse, up to a maximum offset of $540 per annum.

Non-concessional contribution cap limit of $100,000 or phasing down towards $300,000 using the bring forward provisions

For 2016-17 the single year capped contribution amount is $180,000 and then from 1 July 2017 it reduces to $100,000. So this year you can still use the bring forward rule to contribute the full $540,000 before June 30th 2017 and that has been confirmed by treasury. However if you do not have enough to meet that full contribution limit you can still trigger your cap by contributing at least $180,001 before the end of the year. Note that you may also have already triggered that rule in one of the 2 previous financials years and be wondering how much of the cap you have remaining. Well this table will clarify that for you.

In summary the Limit to Bring Forward Contributions based on year triggered are:

The cap now also limits the ability to use the cash-out and recontribution strategy for members who have triggered a condition of release. We normally used this between age 60 -65 to reduce the taxable component of your account balance. Before considering this strategy you should check the available lifetime cap with your administrator / advisor including all retail / industry funds you have been a member of at any time. Many SMSF members took annual pensions and simply recontributed the payments as NCC every year. DO NOT DO THIS! check your cap first PLEASE!

Phew! that was a lot!

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I am breaking the Budget down in to bite size chunks with strategies to consider going forward for SMSF Trustees. Let’s start with Pensions.

The government is removing the tax exemption for earnings on assets supporting ‘transition to retirement’ pension / income streams but has allowed the pension payments and withdrawals from superannuation by people over age 60 to remain tax-free. No special rules for Self Managed Superannuation funds so these rules apply to all.

Taxing Transition to Retirement Pension earnings

From 1 July 2017 in the TTR pension phase of superannuation the tax-exemption on earnings will no longer apply to transition to retirement (TTR) pensions from.

Most TTRs were started as a tax planning strategy using salary sacrifice and the exempt status of pension income. From 1 July 2017 tax will be applied to the earnings derived in a TTR pension.

In addition, you cannot elect for payments to be taxed as lump sums rather than as pension payments to gain a better tax outcome. We used this for people aged 55-60 and fully retired up until now

Strategy implications for current TTR clients:

SMSFs with existing TTRs for members may wish to maintain them until the changes take effect (and legislation is passed). At that point they should consider one of the following options:

Do a commutation of the pension and roll back to the accumulation phase of superannuation

Convert to a full account-based pension if a condition of release has been met

Continue the Transition to Retirement pension if it suits your circumstances.

Seek advice before making any rash decisions.

From 1 July 2017, 15% tax will be applied to the earnings derived in a TTR pension and combined with the lower concessional contribution caps these strategies are likely to be less effective and less popular but still offer some opportunities for clients so we will review the appropriateness on an individual basis before 1 July 2017

Pension transfer cap of $1.6 million

From 1 July 2017, the maximum amount of superannuation that a person can transfer into pension phase is limited to $1.6 million.

Clients who are already in pension phase before 1 July 2017 will be required to transfer any balance above $1.6 million back into accumulation phase. Clients who are starting pensions from 1 July 2017 cannot roll more than $1.6 million into the pension phase (in total), but the balance rolled over can grow over $1.6 million due to earnings without penalty. some CGT relief will be available on investments moving back to accumulation phase but I will deal with that in a later blog.

The capital value of any Defined Benefit Income Streams will be counted towards the $1.6m limit using a multiple of 16 times the annual income stream.

The ATO has promised a portal or access to a central place where people can check their balances across SMSF, retail, DB and industry funds will be available soon.

Amounts transferred in excess of $1.6 million to retirement will be taxed in a similar way to excess non-concessional contributions. That means both the excess amount and earnings on that excess amount in retirement phase will be taxed. So please do not ignore this limit which applies from 01 July 2017.

Strategy implications for current SMSF pension clients:

This measure limits the tax-free benefits generated from pension phase but do not limit the amount that can be saved in accumulation phase which is only taxed at a maximum of 15%. However the overall amount you can get in to Superannuation is limited by changes to contribution caps.

Those clients who have pension balances in excess of $1.6 million can choose to:

leave savings in the accumulation phase of superannuation where tax on earnings is applied at 15% or

withdraw to invest outside superannuation or

withdraw and recontribute to a spouse / partner with a lower superannuation balance who has not used up their caps.

The $1.6 million cap will be indexed in $100,000 increments in line with the consumer price index. Where a member has previously used up a proportion of their retirement balance limit, they will be able to us the remaining proportion of the indexed cap.

Investment Strategies

We will look at each available strategies to consider the tax implications and comparisons of investment options inside or outside superannuation.

For many the option to withdraw some funds when fully retired and seek other tax effective arrangements including using the Low Income Tax Offset and Seniors and Pensioners Tax Offset to minimise tax on earnings outside of super

For the funds kept in Superannuation we will look at ways to maximise returns from investments within the caps by looking at segregating assets supporting the pension and focusing those on high yield, high return assets that can grow the tax exempt pension balance through earnings above the minimum withdrawal rates. That means we will focus on cash, fixed interest and term deposits in the still concessionally taxed accumulation balance, taxed at a maximum 15%.

Other issues

We have been strong advocates of evening up balances in superannuation between partners and this strategy implemented over the last 10 years will benefit many clients.

The Government has also confirmed that they will remove tax barriers to the development of new retirement income products by extending the tax exemption on earnings in the retirement phase to products such as deferred start lifetime annuities and group self-annuitisation products (Yeah , I am not sure what they are either).

These products can provide more flexibility and choice for Australian retirees, and help them to better manage consumption and risk in retirement.

This change was recommended by the Retirement Income Streams Review. The Government has released the Review and agreed all its recommendations. The announcement also states that they will consult on how the new retirement income products will be treated under the Age Pension means test.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

Suppose the government had about A$10 billion a year to fund lower income tax. It could reduce personal income tax by about 6%, or lower each marginal rate by about 1.5 percentage points. Alternatively it could reduce company tax by about 15%, or reduce the current 30% rate to 24%. Which option has more merit?

But the answer as to which is more likely to drive the “jobs and growth” the government has been promising is not that simple. And it is difficult if not impossible to comprehensively model which option is better.

Income tax affects households differently

The two lower income tax options have different implications for the distribution of the tax burden over time. They also impact changes in incentives and rewards to promote a larger economy and higher future living standards, and how much can be clawed back after the first round revenue loss.

A reduction of personal income tax rates provides a more direct and explicit increase in household income, and a quicker gain, when compared with a reduction of the corporate tax rate. Also, lower personal tax rates allow greater government discretion in the distribution of the benefits across households with different incomes, demographic and other characteristics.

Company tax cuts can impact wages and investment

Individuals benefit from lower corporate tax rates with higher market wages. But the higher wage rates will take some years to materialise, and the magnitude of increase attributed to the lower corporate tax rate, versus other factors, is open to debate.

Benefits of a lower corporate tax rate, and in time the flow of these benefits as higher wage rates, involves a chain of decision changes. Australian corporations depend on the savings of international investors for an important share of their investment funds. They use this money to invest in machinery, buildings technology and so forth. But to get it they must show investors they will get a superior return, after Australian corporate income tax is paid, compared to alternative investments in other countries.

If Australia’s company tax rate was cut, this would lower the bar on the required return to attract investment. In the end the lower corporate tax rate induces an increase in investment, resulting in a larger stock of capital and associated technology and expertise. But, this capital accumulation process takes many years.

The enlarged stock of capital, technology and expertise per worker becomes a key driver of increased worker productivity. In time, more productive workers are able to negotiate higher wages. Via this chain of decision changes, employees benefit from the lower corporate tax rate.

Personal tax cuts promote productivity

Lower personal income tax rates provide incentives for a more productive economy and higher living standards through two main mechanisms. Lower marginal income tax rates increase the incentive for, and the rewards from, joining the workforce, working more hours, and putting more into education and skill acquisition. These incentives are especially important for women with children and older workers.

Also, lower personal income tax rates reduce distortions to household decisions on how much to save and where to invest savings in owner occupied homes, other property, financial deposits, shares, superannuation and other options.

The current income tax system imposes different forms of income tax on the different options with very different effective tax rates. For example, income earned on owner occupied housing (of imputed rent and capital gains) is exempt from income tax while the nominal interest on financial deposits (associated with offsetting inflation as well as the returns for delayed consumption) faces the personal rate. Lower personal income tax rates reduce the magnitudes of the distortions caused by different effective tax rates on different saving and investment options.

The difference is in the timing

Lowering the rate of corporate or personal income tax will generate a larger and more productive economy. A larger economy means larger tax bases, and not just income tax, but also GST, payroll and excise. The enlarged tax bases generate larger tax revenues and a partial recapture over time of the first round revenue cost of the income tax rate reductions.

The revenue recapture is expected to be larger for the corporate income tax rate reduction option. With the imputation system, for domestic shareholders a reduction in corporate income tax and less franking credits would be offset by a larger direct personal income tax payment on dividend income.

The greater price sensitivity of the international supply of funds to Australia enticed by a lower corporate tax rate is expected to boost the size of the Australian economy, and tax bases, more than the labour supply response to lower personal tax rates.

Models don’t have the answer

Ultimately, quantifying the relative national productivity, distribution and revenue effects of the lower corporate tax and personal income tax options requires detailed computable general equilibrium models.

Arguably, available models, including those used by government, lack the detail of progressive personal income tax rates for different households, and details of household choices among different investment options with different effective tax rates, to confidently measure the relative effects of the two options.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Sira Anamwong at FreeDigitalPhotos.net

Rate for 2025-26 Related Property LRBA is 8.95%and Listed Shares 10.95%

Old Rate for 2024-25 Related Property LRBA was 9.35% and Listed Shares 11.35%

The ATO have issued long-awaited guidelines providing SMSF trustees with suggested ‘Safe Harbour’ loan terms on which trustees may use to structure a related party Limited Recourse Borrowing Arrangement (LRBA) consistent with dealing at arm’s length with that related party.

By implementing these “Safe Harbour” loan terms, SMSF trustees are assured by the ATO Commissioner that

..for income tax purposes, the Commissioner accepts that an LRBA structured in accordance with this Guideline is consistent with an arm’s length dealing and that the NALI provisions do not apply purelybecause of the terms of the borrowing arrangement.

It is absolutely essential that all non-bank SMSF borrowing arrangements (LRBAs) be reviewed prior now extended to 1 Jan 2017

Where has this come from?

The ATO first released and then re-issued ATO Interpretative Decisions in 2015 (ATO ID 2015/27 and ATO ID 2015/28), dealing with Non-Arm’s Length Income(NALI) derived from listed shares and real property purchased by an SMSF under an LRBA involving a related party lender – where the terms of the loan were not deemed to be on commercial terms.

These ATOIDs state that the use of a non-arm’s length LRBA gives rise to NALI in the SMSF. Broadly, the rationale for this view is that the income derived from an investment that was purchased using a related party LRBA, where the terms of the loan are more favorable to the SMSF, is more than the income the fund would have derived if it had otherwise being dealing on an arm’s length basis.

NALI is taxed at the top marginal tax rate, currently 47% – regardless of whether the income is derived while the fund is in accumulation phase where tax is normally 15% or in pension phase when the income would usually be tax exempt.

After that bombshell, the ATO announced that it would not take proactive compliance action from a NALI perspective against an SMSF trustee where an existing non-commercial related party LRBA was already in place, as long as such an LRBA was brought onto commercial terms or wound up by 30 June 2016.

The Nitty Gritty Details of the Safe Harbour Steps

The ATO has issued Practical Compliance Guideline PCG 2016/5. As a result, provided an SMSF trustee follows these guidelines in good faith, they can be assured that (for income tax compliance purposes) their arrangement will be taken to be consistent with an arm’s length dealing.

The ‘Safe Harbour’ provisions are for any non-bank LRBA entered into before 30 June 2016, and also those that will be entered into after 30 June 2016.

Broadly, this PCG outlines two ‘Safe Harbours’. These Safe Harbours provide the terms on which SMSF trustees may structure their LRBAs. An LRBA structured in accordance with the relevant Safe Harbour will be deemed to be consistent with an arm’s length dealing and the NALI provisions will not apply due merely to of the terms of the borrowing arrangement.

The terms of the borrowing under the LRBA must be established and maintained throughout the duration of the LRBA in accordance with the guidelines provided.

Safe Harbour 1

Safe Harbour 2

Asset Type

Investment in Real Property

Investment in a collection of Listed Shares or Units

Interest RateNote: as of 10 Jan 2019: The RBA no longer round the rates to the nearest 5 basis points.

RBA Indicator Lending Rates for banks providing standard variable housing loans for investors. Use the May rate immediately preceding the tax year. (2015/16 year = 5.75%)(2016-17 year = 5.65%)(2017-18 year = 5.8%)(2018-19 year = 5.8%)(2019-2020 year = 5.94%)(2020-2021 year = 5.1%) (2021-2022 year = 5.1%)(2022-2023 year = 5.35%)2024 FY = 8.85% (2024-25 year = 9.35%) (2025-26 year 8.95%)

Same as Real Property + a margin of 2%

Fixed / Variable

Interest rate may be fixed or variable.

Interest rate may be fixed or variable.

Term of Loan

Variable interest rate loans:Original loan – 15 year maximum loan term (both residential and commercial).Re-financing – maximum loan term is 15 years less the duration(s) of any previous loan(s) in respect of the asset (for both residential and commercial).Fixed interest rate loan:

Rate may be fixed for a maximum period of 5 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 5.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 5 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

Variable interest rate loans:Original loan – 7 year maximum loan term.Re-financing – maximum loan term is 7 years less the duration(s) of any previous loan(s) in respect of the collection of assets.Fixed interest rate loan:

Rate may be fixed up to for a maximum period of 3 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 7 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 7.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 3 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan cannot exceed 7 years.

Loan-Value –RatioLVR

Maximum 70% LVR for both commercial & residential property. Total LVR of 70% if more than one loan.

Maximum 50% LVR.Total LVR of 50% if more than one loan.

Security

A registered mortgage over the property.

A registered charge/mortgage or similar security (that provides security for loans for such assets).

Personal Guarantee

Not required

Not required

Nature & frequency of repayments

Each repayment is to be both principal and interest.Repayments to be made monthly.

Each repayment is to be both principal and interest.Repayments to be made monthly.

Loan Agreement

A written and executed loan agreement is required.

A written and executed loan agreement is required.

Information sourced from Practical Compliance Guidelines PCG 2016/5.

Potential Trap to be aware of: Importantly, as part of this announcement, the ATO also indicated that the amount of principal and interest payments actually made with respect to a borrowing under an LRBA for the year ended 30 June 2016 must be in accordance with terms that are consistent with an arm’s length dealing.Information sourced from Practical Compliance Guidelines PCG 2016/5.

For the 2017-18 and 2018-19 years the rate is 5.8%

For the 2019-20 year the rate is 5.94%

For the 2020-21 year the rate is 5.1%

For the 2021-22 year the rate is 5.1%

For the 2022-23 year the rate is 5.35%

For the 2023-24 year the rate is 8.85%

For the 2024-25 year the rate is 9.35% until 30 June 2025

For the 2025-26 year the rate is 8.95%

For 2019-20 and later years, the rate published for May (the rate for the month of May immediately prior to the start of the relevant financial year)

It is the applicable rate under Column H of the above spreadsheet (click on link). The rate seems to have started in August 2015 but I assume we must use the May rate from now on.

In referencing the Indicator Rate you can use: Ref: Title: Lending rates; Housing loans; Banks; Variable; Standard; Investor Lending rates; Housing loans; Banks; Variable; Standard; Investor Frequency: Monthly Units: Per cent per annum Source RBA Publication Date 04-Apr-2016 Series ID: FILRHLBVSI

A complying SMSF borrowed money under an LRBA, using the funds to acquire commercial property valued at $500,000 on 1 July 2011.

The borrower is the SMSF trustee.

The lender is an SMSF member’s father (a related party).

A holding trust has been established, and the holding trust trustee is the legal owner of the property until the borrowing is repaid.

The loan has the following features:

the total amount borrowed is $500,000

the SMSF met all the costs associated with purchasing the property from existing fund assets.

the loan is interest free

the principal is repayable at the end of the term of the loan, but may be repaid earlier if the SMSF chooses to do so

the term of the loan is 25 years

the lender’s recourse against the SMSF is limited to the rights relating to the property held in the holding trust, and

the loan agreement is in writing.

We do not consider that this LRBA has been established or maintained on arm’s length terms. The income earned from the property, which is rented to an unrelated party, may give rise to NALI.

At 1 July 2015, the property was valued at $643,000, and the SMSF has not repaid any of the principal since the loan commenced.

If after considering TD 2016/16, it is determined that the income earned from the property is in fact NALI, to avoid having to report NALI for the 2015-16 year (and prior years) the Fund has a number of options.

Option 1 – Alter the terms of the loan to meet guidelines

The SMSF and the lender could alter the terms of the loan arrangement to meet Safe Harbour 1 (for real property).

To bring the terms of the loan into line with this Safe Harbour, the trustees of the SMSF must ensure that:

The 70% LVR is met (in this case, the value of the property at 1 July 2015 may be used).

Based on a property valuation of $643,000 at 1 July 2015, the maximum the SMSF can borrow is $450,100. The SMSF needs to repay $49,900 of principal as soon as practical before 30 June 2016.

The loan term cannot exceed 11 years from 1 July 2015.

The SMSF must recognise that the loan commenced 4 years earlier. An additional 11 years would not exceed the maximum 15 year term.

The SMSF can use a variable interest rate. Alternatively, it can alter the terms of the loan to use a fixed rate of interest for a period that ensures the total period for which the rate of interest is fixed does not exceed 5 years. The loan must convert to a variable interest rate loan at the end of the nominated period.

The interest rate of 5.75% applies for 2015-16 and 5.65% p.a. applies from 1 July 2016 to 30 June 2017. The SMSF trustee must determine and pay the appropriate amount of principal and interest payable for the year. This calculation must take the opening balance of $500,000, the remaining term of 11 years, and the timing of the capital repayment, into account.

After 1 July 2016, the new LRBA must continue under terms complying with the ATO’s guidelines relating to real property at all times.

For example, the SMSF must ensure that it updates the interest rate used for the loan on 1 July each year (if variable) or as appropriate (if fixed), and make monthly principal and interest repayments accordingly.

Option 2 – Refinance through a commercial lender

The fund could refinance the LRBA with a commercial lender, extinguish the original arrangement and pay the associated costs.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant part of the 2015-16 year.

Option 3 – Payout the LRBA

The SMSF may decide to repay the loan to the related party, and bring the LRBA to an end before 30 January 2017.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and the relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant period.

Each option will have many advantages and disadvantages – so it is important to understand what the practical implications of each option are, and how physically you will approach each option. Seek specialised advice on this matter as it is not a strategy suitable for DIY implementation

Important Note to 13.22C or Unrelated Unit Trust Investors

The guidelines provided in this PCG are not applicable to an SMSF LRBA involving an investment in an unlisted company or unit trust (e.g. where a related party LRBA has been entered into to acquire a collection of units in an unrelated private trust or a 13.22C compliant trust). As such, trustees who have entered into such an arrangement will have no option but to benchmark their particular loan arrangement based on commercial loan terms, or to bring the LRBA to an end.

Please visit out SMSF Property page to get details on all available strategies for SMSF property investors.

UPDATE (Relief for those caught by Budget measures)

In a letter to an industry association, the Treasurer, Scott Morrison, has outlined transitional arrangements to allow additional non-concessional contributions above the proposed lifetime limit in certain limited circumstances. Contributions made in the following circumstances may be permitted without causing a breach of the lifetime cap:

where the trustees of a self managed superannuation fund (SMSF) have entered into a contract to purchase an asset prior to 3 May 2016 that completes after this date and non-concessional contributions were planned to be made to complete the contract of sale. Non-concessional contributions will be permitted only to allow the contract to complete provided they are within the relevant non-concessional cap that was applicable prior to Budget night, and

where additional contributions are made in order to comply with the Australian Taxation Office’s (ATO) Practical Compliance Guideline (PCG) 2016/5 related to limited recourse borrowing arrangements, provided they are made prior to 31 January 2017.

Additional non-concessional contributions made under these proposed transitional arrangements will count towards the lifetime cap, but will not result in an excess.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Click here for appointment options.

Liam Shorte B.Bus FSSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 9899 3693, Mobile: 0413 936 299

PO Box 6002, Norwest NSW 2153

U40, 8 Victoria Ave., Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572