I am breaking the Budget down in to bite size chunks with strategies to consider going forward for SMSF Trustees. The first part which dealt with pension strategies is available here . This second part deals with changes to contribution options, methods and caps.

Before I go into detail here is a summary of the changes that are relevant to SMSF members (No coverage of Defined Benefit Schemes in this article):

Concessional (Pre-Tax Contributions like employer superannuation guarantee (SGC), salary sacrifice and those contributions where you claim a tax deduction).

- Reduction in the concessional contribution cap to $25,000 regardless of age

- Carried forward concessional cap for account balances below $500,000 from 1 July 2018

- All individuals under 65 will be eligible to claim a tax deduction for personal contributions (bye bye 10% rule). work test applies ot over those 65

- Reduction in income threshold to $250,000 where additional super contribution tax applies

- Reduction in contribution tax for people earning less than $37,000

- Extension of low-income spouse contribution tax offset

Non-Concessional (Post Tax Contribution like personal after tax contributions and Government co-contributions).

- Reduction in Non-concessional contribution cap limit to $100 per annum

- Reduction of existing annual non-concessional bring forward provisions

Now the detail:

Reduction in the concessional contribution cap to $25,000 regardless of age

The concessional contribution cap will be reduced from the current level of $30,000 to $25,000 from 1 July 2017, irrespective of the age of the individual. The higher cap of $35,000 that currently applies to individuals over age 50 will be abolished. The reduced cap will continue to be indexed in future years in line with wages growth.

Carried Forward or Catch-up concessional contributions

From 1 July 2018 individuals will be able to make additional concessional contributions where they have not reached their concessional contributions cap in previous years. Access to these unused cap amounts will be limited to those individuals with a superannuation balance less than $500,000. Unused amounts accrued from 1 July 2018 will be able to be carried forward on a rolling basis for a period of five consecutive years.

This measure allows some additional flexibility in the timing of your contributions like making $125,000 for a tax deduction on the sale of a property or share portfolio if you did not make contributions in the previous 4 years. Your ability to save may vary throughout your career and this measure will assist to some extent, but falls well short of my preferred option for a lifetime cap on concessional contributions. The restriction based on size of account balance will add complication to the administration of this measure when multiple funds are involved.

All individuals under 65 will be eligible to claim a tax deduction for personal contributions

From 1 July 2017, all superannuation fund members up to age 65 will be able to claim an income tax deduction for personal superannuation contributions up to the concessional contribution cap ($25,000), regardless of their employment circumstances. This is good news for people who are partially self-employed and partially wage and salary earners, and individuals whose employers do not offer salary sacrifice arrangements, as they will benefit from this proposal. Personal contributions for which a tax deduction is claimed will count towards the concessional, rather than the non-concessional cap.

While I accept the government’s intention is to increase flexibility for more people to access the concessional contribution cap if they are able to do so, the mechanism requiring individuals to notify their fund of their intention to claim a tax deduction for their personal contributions will add considerable complexity to fund administration. the “she’ll be right” and “I’ll do it later factor” will lead to many missing opportunities.

Over 65’s will still need to meet the work test.

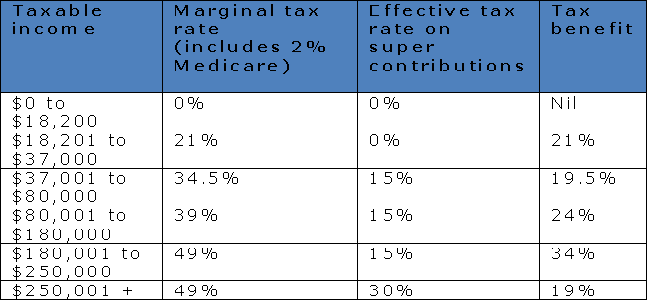

Reduction in income threshold to $250,000 where additional super contribution tax applies

From 1 July 2017, individuals with “relevant income” greater than $250,000 will pay an additional 15 per cent tax on their concessional contributions, down from $300,000. The additional tax, referred to as “Division 293 tax” after the section of the tax legislation which governs the tax, will be payable where the individual’s taxable income (including reportable fringe benefits and certain other amounts) plus concessional contributions (excluding those that exceed the concessional contributions cap) is greater than the $250,000 threshold.

Superannuation still remains attractive despite this change, the 30% tax applied to concessional contributions is still less than the marginal tax rate on earnings so contributing to super remains attractive. But with the lower $25,000 concessional contribution there will be limited scope for you to make optional concessional contributions. For example, if you earn $250,000 and your employer pays the 9.5% SG on your full salary this is an annual employer contribution of $23,750 which has almost fully utilised the new lower cap. If you are on a higher income with disposable income you may look for alternatives outside superannuation or top up your partner/spouse’s superannuation (and potentially receive a tax offset if they earn less than $37,000).

After earlier reports that the threshold would be reduced to $180,000, the proposed threshold of $250,000 means the tax will apply to only around 1 per cent of superannuation fund members. Retention of the existing mechanism which minimises the administrative costs to superannuation funds associated with this tax is welcome.

Reduction in tax for people earning less than $37,000

From 1 July 2017, the Government will introduce a Low Income Superannuation Tax Offset (LISTO) to reduce the tax on superannuation contributions for low-income earners. The measure will apply to individuals with taxable income less than $37,000, and will effectively refund the tax on concessional contributions up to an annual cap of $500. This measure will replace the Low Income Superannuation Contribution (LISC) which was scheduled to be abolished from 1 July 2017, however, the mechanism will be slightly different. Rather than the government making a direct

contribution to the individual’s superannuation account, the offset will apply to the contribution tax deducted by the superannuation fund. The Australian Taxation Office will determine an individual’s eligibility for the LISTO and advise their superannuation fund annually. The fund will then contribute the LISTO to the individual’s account. The government will consult on the implementation of this scheme.

Extension of low-income spouse contribution tax offset

The government will increase access to the low-income spouse superannuation tax offset by raising the income threshold for the low-income spouse from $10,800 to $37,000 and phasing out up to $40,000. This arrangement provides a tax offset of 18 per cent of contributions made by the contributing spouse, up to a maximum offset of $540 per annum.

Non-concessional contribution cap limit of $100,000 or phasing down towards $300,000 using the bring forward provisions

For 2016-17 the single year capped contribution amount is $180,000 and then from 1 July 2017 it reduces to $100,000. So this year you can still use the bring forward rule to contribute the full $540,000 before June 30th 2017 and that has been confirmed by treasury. However if you do not have enough to meet that full contribution limit you can still trigger your cap by contributing at least $180,001 before the end of the year. Note that you may also have already triggered that rule in one of the 2 previous financials years and be wondering how much of the cap you have remaining. Well this table will clarify that for you.

In summary the Limit to Bring Forward Contributions based on year triggered are:

See a full explanation in this article : So How Much Can I Contribute to my SMSF Using the Bring Forward Rule

The cap now also limits the ability to use the cash-out and recontribution strategy for members who have triggered a condition of release. We normally used this between age 60 -65 to reduce the taxable component of your account balance. Before considering this strategy you should check the available lifetime cap with your administrator / advisor including all retail / industry funds you have been a member of at any time. Many SMSF members took annual pensions and simply recontributed the payments as NCC every year. DO NOT DO THIS! check your cap first PLEASE!

Phew! that was a lot!

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

![]()

![]()

![]()

![]()

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.