One of my most popular long term blogs is Why Self Managed Super Funds Should Have A Corporate Trustee and thankfully most new SMSFs are finally being set up with a corporate trustee from the outset. But that leaves many existing SMSFs with Individual Trustees and I get numerous questions about the cost of the transfer process. If you are considering an SMSF the I would encourage you to read through that article and feel free to pass it on to your friends, family or advisors.

The basic costs depend on your current legal document deed provider or the new provider chosen to implement the changes. But here is a guideline

Cost of Sole Purpose Corporate Trustee would usually be around $660-$880 of which $506 is the ASIC registration fee

Trust Deed Amendment to Retire the current Individual trustees and Appoint the new Corporate Trustee is about $200-$375

Then all assets need to be moved in to new Accounts in the name of the new Trustee company.

Shares/ETFs/Hybrids usually cost $55 per share (you can bargain a discount with your broker) but a new Account application is also required

Wrap Platforms – depends on the provider but usually you will have to set up a new Account and they will in-specie transfer them across.

Managed funds may have stamp duty costs depending on the state. A new application for is required before the transfer

Bank account providers just usually require a request in writing, copy of the Company Certificate of Registration and copy of the signed Trust Deed Amendment

Property will depend on the State but some have an exemption or concessional stamp duty and only a small fee for changing the trustee on the title. See more detail here Stamp Duty Requirements on Change of SMSF Trustees – I will try to get this update shortly.

Bullion/Coins – just usually require a request in writing, copy of the Company Certificate of Registration and copy of the Trust Deed Amendment

Ongoing Costs

Costs should not be a deterrent as a sole Purpose Trustee company ASIC review fee is only $55 per year and you can lock that in and get a discount for up to 10 years. See here for more detail on that discount.

Don’t feel like trying to do all this yourself? How much do we charge for guiding you through the process

If you require assistance and advice on making the changes our advice fee starts from $4,400 as it is a time consuming process. This includes:

Review of your current circumstances and portfolio to see what needs to be done

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why not contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Self-funded retirees have felt like punching bags for the last few years with hit after hit chipping away at their ability to fend for themselves within the rules they had relied upon in making their savings plans over the last 30 years. Combine the changing of goal posts with low interest rates and blue-chip underperformance from the banks, telcos and utilities and they are not to be blamed for thinking a hex had been put on them.

So an SMSF friendly budget is the welcome news coming out of the 2018-19 Federal Budget. With many of us SMSF Specialists and you the SMSF members still working through the wide-reaching and complex superannuation changes which took effect from 1 July 2017, this Federal Budget will provide much needed stability while looking to reduce costs for SMSFs and prove additional flexibility.

The key changes proposed for SMSFs and superannuation are:

Three-yearly audit cycle for some self-managed superannuation funds.

The Government will change the annual SMSF audit requirement to a three yearly requirement for SMSFs with a history of good record keeping and compliance. The measure will start on 1 July 2019 for SMSF trustees that have a history of three consecutive years of clear audit reports and that have lodged the fund’s annual returns in a timely manner.

One concern I have is if trustees make a mistake in year 1 that is not discovered until year 3, will they face 3 years interest charges on the penalties.

Expanding the SMSF member limit from four to six

As already announced, the Federal Government confirmed its decision to expand the number of members allowed in an SMSF from four to six. Expanding the definition of an SMSF to a fund with a maximum of six members will provide greater flexibility in how funds can be structured.

Whilst there are some concerns over making decisions I like this move where as mum and dad in their later years want to reduce their involvement but they want help rather with the fund rather than moving to separate retail funds. It may help prevent elder Financial abuse where instead of one child assuming control of the SMSF, more of the family could be involved. Temptation and inheritance impatience is always there for one person but add a few others in to the decision making and the risk of financial abuse reduces considerably.

Also 6 members of a family small business allows for later drawdown from the parents accounts and recontribution for younger family members to retain business real property in the fund after death of the older generation.

Note; you will need to ensure your trust deed allows more than 4 members and it most likely won’t so you will need to update the trust deed first before accepting new members. READ THE DEED

Over 65, 1 additional year Work test exemption

The Government will provide more time for Australians aged 65 to 74 to boost their retirement savings, by introducing an exemption from the superannuation work test.This exemption will apply where an individual’s total superannuation balance is below $300,000 and will permit voluntary superannuation contributions in the first year that they do not meet the work test requirements.

This is good but limited in its scope as more and More people have reached the $300k level because of Super Guarantee Contributions for most since 1992 or before for some. But it is a female friendly move as they are most likely to have lower balances

Life insurance cover in super to be opt-in for individuals under 25 years of age.

The Government will legislate that life insurance cover in superannuation will be opt-in for those individuals under 25 years of age or with account balances under $6000 to ensure that unnecessary fees do not erode smaller balances.

Life insurance cover will also cease where no contributions have been made for a period of 13 months.

If you have kept a retail or industry fund open with small balances to retain insurances you may need to put a small annual contribution in place (I would recommend $100 per half year just in case) to ensure it does not get tagged as dormant.

Older Australian package

The Government introduced the following measures to enhance the standard of living older Australians:

• Increase to the Pension Work Bonus from $250 to $300 per fortnight.

• Amendments to the pension means test rules to encourage the take up of lifetime retirement income products.

• Expansion of the Pensions Loan Scheme to allow more Australians to use the equity in their homes to increase their incomes.

I think this will be a major bonus for those with a lumpy asset or shareholding’s they wish to retain but need more cashflow. At a current rate of 5.25% the Pensions Loan Scheme is a very decent rate and security that you are borrowing from a bank or predatory lender based on a brokers conflicted commissions.

Personal income tax bracket changes (take most these with a pinch of salt!)

The Government has provided personal income tax relief to lower and middle income earners. A Low and Middle Income Tax Offset will now be available for individuals with incomes of up to $125,333.

The $87,000 income threshold, above which a 37 per cent tax rate applies, will increase to $90,000.

Other changes

• A surplus of $2.2 billion is expected in 2019-20, one year ahead of schedule.

• The Government’s planned increase in the Medicare levy from 2 per cent to 2.5 per cent, to fund the National Disability Insurance Scheme, will now not go ahead due to increased tax revenues.

How can we help?

Some of these measures may open up strategy options for you and your family.

If you have any questions or would like further clarification in regards to any of the above measures outlined in the 2018-19 Federal Budget, please feel free to give me a call or email to arrange a time to meet or talk by phone so that we can discuss your particular requirements in more detail.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

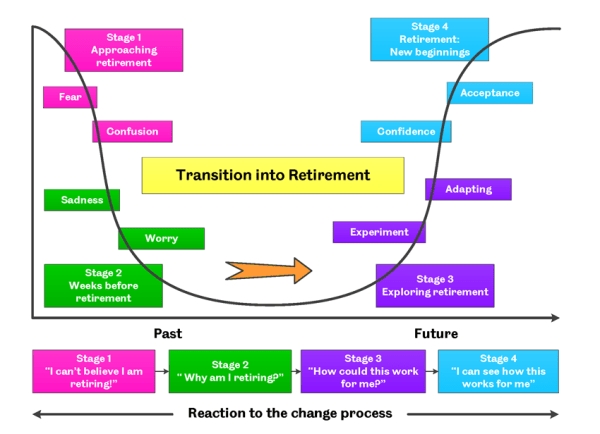

Adapted from ‘Managing Transitions’ by William Bridges.

Retirement. It’s something you’ve thought about for years but kept saying you will deal with it nearer the time. But how do you make sure you’re ready to deal with change when you do come to retire?

So this blog is not about money, it’s about managing change, anxiety and relationships during one of the biggest changes in your life. It has been adapted from an US article.

Retirement might be your time to do your own thing, to travel overseas, go bush in the outback, spend quality time with your loved ones, to return to education, start a different career, take up a volunteer activity, begin an exercise program, or pursue a hobby. There are so many things you could be doing with your newfound time. It seems as though the possibilities for life changes in retirement are endless. But many struggle in that initial period.

Even though you are excited to enter this new stage of life, the amount of change can feel overwhelming and it can intimidating to handle change in retirement. If a lifetime of work demanded much of your time and attention, you may not have had the opportunity to develop many leisure time interests. You may find yourself looking for new things to do and get involved with.

If many of your social activities have involved people from work, you may want and need to develop friendships that are based on your new interests (think about Rotary, Probus, Men’s Shed, Book Club, Classic Car Group, Yoga, Red Hat Society, Bush Walking Club etc.). If you are retiring and adjusting to an empty nest at the same time, you may feel especially challenged handling all of this change associated with retirement. Despite wanting to retire, adapting to so many changes in your life can be difficult.

How you’ve handled change during your lifetime can offer insight into how well you’ll adapt to change in retirement. Having an awareness of how to better manage change can improve your adjustment to retirement.

Here are ten questions to ask yourself about handling life changes in retirement:

1.What changes do you want to make in your life? This is a big question but you probably have some ideas of things you’d like to start doing or do more of. Exercise, travel, family time and household projects are all common starting points. Make a list and begin to identify all the ways you want to change your life in retirement. Tip for Ladies: Is your husband struggling for ideas? Try “101 Things to Do With A Retired Man: … to Get Him Out From Under Your Feet!”

2. Why do you want to make these changes? It’s not enough to say you want to improve your diet or read more books. It’s time to figure out the benefits of making these changes. What will you gain by eating differently or reading more? Recognise why you want to make the change so that you’ll be encouraged to follow through with it.

3. What change do you want to make first? If you’ve been thinking about all you could do in retirement, you may discover that it’s hard to figure out where to begin. Feeling overwhelmed by the choices may mean that you don’t select anything. Keep it simple. If you could change just one thing, what would it be?

4. What impact will your changes have on others? Often if we change something in our life, it has a domino effect. If you go back to school, you may need to use weekend time for studying. If your volunteer project involves evenings, you may need to give up some family time. Recognise that others in your life may question the changes that involve them. Talk about the upcoming changes with significant others and gain their support.

5. Are you willing to change? Are you going to be frustrated making a change in your life when it isn’t something you truly want to do? If you’re a stay-at-home person, don’t kid yourself and try to adopt a freewheeling, caravanning lifestyle just because others say you’ll love it. This is could be a change that you won’t really be willing to make long-term.

6. Are you ready to change? It’s one thing to say you want to start exercising, volunteering or start learning a language. Doing it may be harder than you think. You may be someone who finds change is really difficult. If that’s you, prepare yourself mentally for more challenges right at the start.

7. Are you prepared to make the effort? Making changes in your life requires an effort. Be ready for a learning curve and some inherent frustrations. As adults, we get comfortable in our habits and routines. If you really want to begin an exercise program, you may need a significant amount of willpower to get yourself started.

8. Who can help you change? When you’re learning something new, ask for help. Join a group, connect online or ask others in your network for advice. You may have spent your whole life wanting to figure things out for yourself. Recognise that your time now is a valuable resource. Don’t waste it. Ask for help.

9. Can you check your ego at the door? The first time you try doing something new, it’s likely you won’t be great at it. New things take practice. Don’t let your fear of failure or ego get in the way of learning something new. Look at it this way—you made it this far in life, you are certainly capable of learning a yoga pose or to put up shelves.

10. Are you seeing the results you expected? Make your changes and give yourself a reasonable amount of time to get used to them. Are you seeing the benefits you expected? If not, chalk it up to good experience and move on.

Accept that retirement will bring many changes in your life. Increasing your awareness about how you adapt to change will contribute to your overall retirement happiness.

Looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why not contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make 2018 the year to get organised or it will be 2028 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I have adapted this content to Australian circumstances from an original American article on retirementstyle.com By Deborah Williams

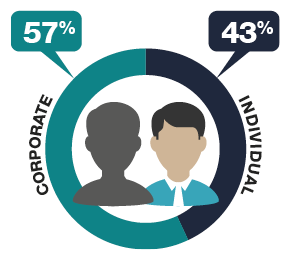

For the last decade every time I saw the SMSF statistical results issued by the ATO I was dismayed by the number of new SMSF funds being set up with Individual Trustees, often well over 80% each year. I assumed this was people setting up self managed superannuation funds without good advice or reasonable research.

So I was delighted to see the latest stats provided by the ATO for 2015-16 but including some 2016-17 data which has seen a complete turnaround with over 80% of new SMSFs being set up with Corporate Trustees and the overall numbers on existing funds turning in favour of using a company.

SMSF trustee structure

At 30 June 2017, 57% of all SMSFs had a corporate trustee rather than individual trustees.

Of newly registered SMSFs in 2015 to 2017, on average 81% were established with a corporate trustee.

A few times over the last 5 years I have run polls asking professionals in the SMSF industry whether they would recommend individual or corporate trustees. Every time the overwhelming result is in favour of Corporate Trustees.

So over 90% of professionals who deal day in day out with SMSF issues and like myself deal with some of the fallout when approached by grieving widows(ers), recommend a Corporate trustee for an SMSF.

Costs

Costs should not be a deterrent as a sole Purpose Trustee company only costs about $600-$880 to set up and the ASIC review fee is only $48 per year and you can lock that in and get a discount for up to 10 years. See here for more detail on that discount.

I have set out my arguments for a Corporate Trustee in this previous article Why Self Managed Super Funds Should Have A Corporate Trustee. If you are considering an SMSF the I would encourage you to read through that article and feel free to pass it on to your friends, family or advisors.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

When I talk to self-directed SMSF trustees their excuse for not diversifying more from Aussie Shares and Term Deposits was that it was difficult to understand some sectors and to get a decent diversification without building a huge portfolio of stocks, unlisted managed funds, bonds, hybrids etc. They hated application forms especially for SMSF investments but they have been reluctant to use a platform despite my argument that often a platform was a useful vehicle. Most just are not interested in another layer of fees for their SMSF. Each to their own so I left the argument there. However now the mountain is coming to them!

The following is general information and not a recommendation, you still need to do your own research or get advice for your personal circumstances.

In November 2017 Vanguard Australia finally launched a suite of four exchange traded funds (ETFs) that provide greater access to their leading diversified portfolio strategies. This will make SMSF and personal investing a far more accessible and transparent option for many and ultimately help them achieve their financial goals at a lower cost, easier reporting and with less paperwork than currently. They offer a great opportunity to develop a well simple, market leading diversified core to your portfolio.

The four Vanguard Diversified Index ETFs build on their extensive suite of ETFs and unlisted Managed Funds, and are one of the first ETFs allowing investors to gain diversification across and within all major asset classes, while making a clear choice about how much risk they take on. I would argue that AMP’s DMKT and Schroder’s GROW do this to some extent but not at this low a cost as they are actively managed an many might think they are a good blend with Vanguard’s new range.

The conservative (VDCO), balanced (VDBA), growth (VDGR) and high growth (VDHG) ETFs offer investors simple, single trade access to Vanguard’s global expertise in portfolio management and asset allocation, with annual investment costs at just 0.27 per cent. Yes that’s only $2.70 management fee for every $1000 invested in a diversified portfolio, wipe the floor of many industry and retail super funds.

Each Diversified Index ETF is a share class of an existing Vanguard Diversified Index Fund, meaning ETF investors can tap into the benefits of an established asset pool, collectively worth more than $7 billion, through Vanguard’s existing range of non-listed multi-asset funds. Vanguard’s Diversified Index Funds consistently rank in the top quartile of performance with their peers over three, five and 10 year periods, according to Morningstar.

Yes you are giving up some transparency and control but I believe you can rely on Vanguard’s investment experts to continuously assess their portfolio’s exposure and periodically rebalance it back to its intended level of risk.”

Each Vanguard Diversified Index ETF provides investors with extensive global exposure to around 6500 individual companies and more than 5000 fixed income securities.

Just in case you have not heard of Vanguard, here is a little detail to help build a picture of their strength and reach:

The Vanguard Group, Inc.: Key facts and figures*

Founded

1975

Total assets under management

AUD $5.9 trillion

Funds offered

180 in the US, and 190 funds in markets outside the US

Ownership

The Vanguard Group, Inc. is owned by its US-domiciled funds,

which are owned by their shareholders.

Headquarters

Valley Forge, Pennsylvania, USA

Chairman and CEO

F. William McNabb III

Number of employees

About 15,000 worldwide

Vanguard’s Investment Strategy Group, a global team of researchers and analysts, set the asset allocation of the diversified funds as part of a robust framework used by Vanguard globally. This framework includes analysis of concentration risk and currency exposure, and incorporates comprehensive modelling generated by Vanguard’s proprietary forecasting engine, the Vanguard Capital Markets Model.

Looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why not contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make 2018 the year to get organised or it will be 2028 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I love working on strategies for clients but sometimes you just need a true expert or excellent software to crunch the numbers. I was looking for some ideas on downsizing as it had become clear to me that is was not the panacea to retirement funding that client’s often believe it would be. So I was looking for an in-depth article working through the numbers and Rob van Dalen of Optimo Financial has kindly stepped up to provide the required analysis in our latest guest blog. Rob’s main warning is to do your sums on your own particular situation before leaping in to a downsizing strategy.

Optimo Financial

Suite 204, 10-12 Clarke Street, Crows Nest NSW 2065

PO Box 931, Crows Nest NSW 1585

Do Your Sums Before Downsizing

A popular subject often talked about at family barbecues is; “should mum and dad downsize when they get older?” Often it’s assumed that downsizing is the best option moving forward. To test and possibly challenge this we decided to run a few scenarios through our Pathfinder Financial Optimisation Platform to find out. Read our findings below;

1.1 The Clients

In this example, we look at the case of David and Alice who have recently retired and who will soon both be eligible for the age pension. David was born on 11 April 1953 while Alice was born on 15 November 1952. They have a modest $400,000 in super. Their other assets are the family home valued at $900,000 and personal assets valued at $40,000. They have no debt. They would like to have $50,000pa (increasing at CPI) for living expenses. They are worried that their super is not sufficient to maintain their desired income. Consequently, they have contemplated selling the family home and moving to a cheaper area where they could buy a new home for $500,000. Will downsizing leave them better off?

1.2 Assumptions

We have assumed in the analysis:

· Pension fund returns 5.7%pa;

· House selling costs 2.5%;

· House purchase costs 6% (including stamp duty);

· House prices in the long term increase at 3%pa;

· CPI 2.5%p.a.

1.3 Scenario 1: Retain Current Home

We first examine the scenario where David and Alice retain their current home. In this case, they will receive income from the government pension as well as drawing a pension from their own super. Figure 1 shows the sources of their income over a 20 year period.

David and Alice receive approximately 64% of their income from the age pension and associated benefits (see also Figure 6 below). The remainder is withdrawn from their pension account through withdrawing the minimum amount each year (plus some extra for the first few years until they become eligible for the age pension).

Their age pensions are limited approximately equally by the income and assets tests. After 20 years, David and Alice have a combined wealth of $1,960,000 most of which is from the family home.

1.4 Scenario 2: Downsizing Family Home in 2016/17

The next scenario sees David and Alice downsizing their family home from $900,000 to $500,000 in 2016/17. Their ages enable them to deposit the excess funds generated from the house sale into super as non-concessional contributions. However, a Pathfinder® analysis shows that increasing their superannuation balance reduces their age pension because, unlike the family home, super counts towards the age pension assets test and is deemed for the income test. Figure 2 shows the results of the age pension assets and income tests for David and Alice and we can see that their pension is now limited by the assets test. For a home owning couple, the age pension reduces at a rate of $3 per fortnight for each $1,000 of assets in excess of $575,000. This taper rate was doubled from 1 January 2017, so now has a much larger impact on the pension received.

So in 2019/20, for example, their age pension reduces from $36,337 to $9,004 and they must draw more from their pension account to make up the difference. Their wealth after 20 years is now projected at $1,581,000 or about $379,000 less than in the first scenario.

1.5 Scenario 3: Downsizing Family Home in 2027/28

In the third scenario, we examine the possibility that David and Alice defer the downsizing for ten years, say in 2027/28. Their age pension is initially unaffected until they downsize the family home, but after that time their age pension payments are severely curtailed. Their projected wealth after 20 years is now $1,714,000. This is a better outcome than in the second scenario but is still $246,000 less than if they keep their existing home.

1.6 Comparing the Scenarios

Figure 3 gives a comparison of the annual age pension received in the three scenarios. You can see that the scenario where they retain their current home, yields a higher pension and that their pension drops sharply after the sale of their house in the other two scenarios.

Figure 4 shows the total age pension payments over the 20 years. You can see that by keeping their original family home, their total pension entitlement is significantly higher than either of the downsizing options we analysed.

Figure 5 shows the total wealth over the 20 year period analysed.

The first point to note is the importance of the age pension towards retirement income, depending, of course, on the particular circumstances. Figure 6 shows the composition of retirement income over the 20 years analysed for Scenario 1.

1.7 Conclusions

In this example, the age pension plus estimated concession card benefits contribute about 64% to income while the account based pensions contribute about 36%. The second point is that downsizing the family home may not result in improving the overall situation as an increase in payments from a private pension may be more or less offset by a decrease in the age pension.

1.8 Pathfinder Learnings

In our Pathfinder® analysis, we find, perhaps surprisingly, that a couple could be considerably worse off by downsizing the family home. Any funds added to super by the income generated from downsizing could be dissipated by a reduction in the age pension. In addition, the costs of sale and repurchase of a family home are significant.

The age pension can provide a buffer between retirement savings and lifestyle expenses.

For persons eligible for the age pension, downsizing the family home may leave you worse off financially because of the impact of the age pension income and assets test.

Thank you Robby

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

There are many rumours and well-intentioned but wrong advice out here on the internet about how to maximise Centrelink or DVA pension by “gifting assets” before applying. I want to clear up some of those misunderstandings

The gifting and deprivation rules prevent you from giving away assets or income over a certain level in order to increase age pension and allowance entitlements. For Centrelink and Department of Veteran’s Affairs (DVA) purposes, gifts made in excess of certain amounts are treated as an asset and subject to the deeming provisions for a period of 5 years from disposal.

Acknowledgement: I have relied on the excellent guidance of the AMP TAPin team for the majority of the content in this article. They write great technical articles for advisors and I try and make them SMSF trustee friendly.

What is considered a gift for Centrelink purposes?

For deprivation provisions to apply, it must be shown that a person has destroyed or diminished the value of an asset, income or a source of income.

A person disposes of an asset or income when they:

− engage in a course of conduct that destroys, disposes of or diminishes the value of their assets or income, and

− do not receive adequate financial consideration in exchange for the asset or income.

Adequate financial consideration can be accepted when the amount received reasonably equates to the market value of the asset. It may be necessary to obtain an independent market valuation to support your estimated value or transferred value or Centrelink may use their own resources to do so..

Deprivation also applies where the asset gifted does not actually count under the assets test. For example, unless the ‘granny flat’ provisions apply, deprivation is assessed if a person does not receive adequate financial consideration when they:

− transfer the legal title of their principal home to another person, or

− buy a new principal home in another person’s name.

What are the gifting limits?

The gifting rules do not prevent a person from making a gift to another person. Rather, they cap the amount by which a gift will reduce a person’s assessable income and assets, thereby increasing social security entitlements.

There are two gifting limits.

A person or a couple can dispose of assets of up to $10 000 each financial year. This $10, 000 limit applies to a single person or to the combined amounts gifted by a couple, and

An additional disposal limit of $30 000 over a five financial years rolling period.

The $10,000 and $30,000 limits apply together. That is, although people can continue to gift assets of up to $10 000 per financial year without penalty, they need to take care not to exceed the gifting free limit of $30 000 in a rolling five-year period.

What happens if the gifting limits are exceeded?

If the gifting limits are breached, the amount in excess of the gifting limit is considered to be a deprived asset of the person and/or their spouse.

The deprived amount is then assessed as an asset for 5 anniversary years from the date of gift. It is assessed as an asset for asset test purposes and subject to deeming under the income test.

After the expiration of the 5 year period, the deprived amount is neither considered to be a person’s asset nor deemed.

Example 1: Single pensioner – gifts not impacted by deprivation rules

Sally, a single pensioner, has financial assets valued at $275,000. She has decided to gift some money to her son to improve his financial situation. Her plan for gifting is as follows:

Financial year

2017/18

2018/19

2019/20

2020/21

2021/22

2022/23

Amount gifted

$6,000

$6,000

$6,000

$6,000

$6,000

$6,000

With this gifting plan, Sally is not affected by either gifting rule. This is because she has kept under the $10,000 in a single year rule and also within the $30,000 per rolling five-year period.

Example 2: Single pension – Gifts impacted by both gifting rules

Peter is eligible for the Age Pension. He has given away the following amounts:

Financial year

Amount gifted

Deprived asset assessed using the $10,000 in a financial year free area rule

Deprived asset assessed using the $30,000 five-year free area rule

2017/18

$33,000

$23,000

$0

2018/19

$2,000

$0

$0

In this case, $23,000 of the $33,000 given away in 2017/18 exceeds the gifting limit (the first limit of $10,000) for that financial year, so it will continue to be treated as an asset and subject to deeming for five years.

In 2018/19, while gifts totalling $35,000 have been made, no deprived asset is assessed under the five-year rule after taking into account the deprived assets already assessed, ie $33,000 + $2,000 – $23,000 = $12,000, which is less than the relevant limit of $30,000.

Example 3: Couple impacted by both gifting rules

Ted and Alice are eligible for the Age Pension. They give away the following amounts:

Financial year

Amount gifted

Deprived asset assessed using the $10,000 in a financial year free area rule

Deprived asset assessed using the $30,000 five-year free area rule

2017/18

$10,000

$0

$0

2018/19

$13,000

$3,000

$0

2019/20

$10,000

$0

$0

2020/21

$10,000

$0

$10,000

2021/22

Any gifts in 2014/15 will be assessed as deprived assets under the five-year rule

In this case, $3,000 of the $13,000 given away in 2018/19 exceeds the gifting limit for that year, so it will continue to be treated as an asset and subject to deeming for five years. The $10,000 given away in 2020/21 exceeds the $30,000 limit for the five-year period commencing on 1 July 2017, so it will also continue to be treated as an asset and subject to deeming for five years.

Are some gifts exempt from the rules?

Certain gifts can be made without triggering the gifting provisions. Broadly speaking, these include:

− Assets transferred between the members of a couple. A common example is where a person who has reached Age Pension age withdraws money from their superannuation and contributes it to a superannuation account in the name of the spouse who has not yet reached age pension age.

− Certain gifts made by a family member or a certain close relative to a Special Disability Trust. For more information on Special Disability Trusts, refer to Department of Human Services – Special Disability Trusts.

− Assets given or construction costs paid for a ‘granny flat’ interest. See Department of Human Services – Granny Flat Interest for further detail.

Trying to be too smart – Gifting prior to claim

Contrary to what many read on the internet any amounts gifted in the five years prior to accessing the Age Pension or other allowance are subject to the gifting rules

Deprivation provisions do not apply when a person has disposed of an asset within the five years prior to accessing the Age Pension or other allowance but could not reasonably have expected to become qualified for payment. For example, a person qualifies for a social security entitlement after unexpected death of a partner or job loss.

Gifting and deceased estates

The gifting rules apply to a person’s interest in a deceased estate if the person does any of the following:

− Gives away their right to their interest in a deceased estate for no/inadequate consideration,

− Directs the executor to distribute their interest in a deceased estate for no/inadequate consideration, or

− After the estate has been finalised, gives away their interest in a deceased estate to a third-party for no/inadequate consideration.

The above rules apply even if the deceased died without a will.

Gifting and death of a partner

In some circumstances, couples in receipt of a social security benefit may give away assets prior to death of one of them. Prior to death, any deprived assets would have been assessed against the pensioner couple for five years from the date of the disposal. Now that a member of the couple has passed away, how will the deprived assets be assessed for the surviving partner?

The amount of deprivation that continues to be held against a surviving partner depends on who legally owned the assets prior to death.

Table 1: Gifting and death of a partner

Legal owner of the deprived asset

Assessment of deprived assets

jointly,

does not change.

by the deceased partner,

is reduced to zero.

by the surviving partner,

increases by the amount held against the deceased partner by the outstanding balance held against the deceased partner.

Example 4: Death of a partner

Daryl (age 84) and Gail (age 78) gifted an apartment worth $260,000 to their son Ethan on 1 July 2019. At the time the gift was made, Centrelink assessed $250,000 as a deprived asset. Daryl passed away on 1 July 2020.

The treatment of the deprived assets for Gail will depend on who legally owned the assets prior to Daryl’s death. The impact of different ownership options is shown below:

Legal owner of the deprived asset

Assessment of deprived assets

jointly,

Half of the asset value of the deprived asset will be assessed against the surviving spouse. As the amount of the deprived asset is $250,000, only $125,000 will be assessed against Gail

by the deceased partner,

No amount will be assessed against the surviving partner. As the amount of the deprived asset is $250,000, the amount assessable to Gail is $0.

by the surviving partner,

The full amount will continue to be assessed against the surviving partner. As the amount of the deprived asset is $250,000, the amount assessable to Gail remains at $250,000.

Want a Centrelink Review or are you just looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why not contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options. Do it! make this the year to get organised or it will be 2028 before you know it.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

With all the talk about Total Super Balance caps and where people will invest money going forward if they can’t get it in to superannuation, the spotlight is being shone on “trusts” at present. This has also brought with it the claims of tax avoidance or tax minimisation, so what exactly are trusts and are there differences between Family Trusts, Units Trusts, Discretionary Trusts and Testamentary Trusts to name a few.

Trusts are a common strategy and this article aims to aid a better understanding of how a trust works, the role and obligations of a trustee, the accounting and income tax implications and some of the advantages and pitfalls. Of course, there is no substitute for specialist legal, tax and accounting advice when a specific trust issue arises and the general information in this article needs to be understood within that context.

Introduction

Trusts are a fundamental element in the planning of business, investment and family financial affairs. There are many examples of how trusts figure in everyday transactions:

Cash management trusts and property trusts are used by many people for investment purposes

Joint ventures are frequently conducted via unit trusts

Money held in accounts for children may involve trust arrangements

Superannuation funds are trusts

Many businesses are operated through a trust structure

Executors of deceased estates act as trustees

There are charitable trusts, research trusts and trusts for animal welfare

Solicitors, real estate agents and accountants operate trust accounts

There are trustees in bankruptcy and trustees for debenture holders

Trusts are frequently used in family situations to protect assets and assist in tax planning.

Although trusts are common, they are often poorly understood.

What is a trust?

A frequently held, but erroneous view, is that a trust is a legal entity or person, like a company or an individual. But this is not true and is possibly the most misunderstood aspect of trusts.

A trust is not a separate legal entity. It is essentially a relationship that is recognised and enforced by the courts in the context of their “equitable” jurisdiction. Not all countries recognise the concept of a trust, which is an English invention. While the trust concept can trace its roots back centuries in England, many European countries have no natural concept of a trust, however, as a result of trade with countries which do recognise trusts their legal systems have had to devise ways of recognising them.

The nature of the relationship is critical to an understanding of the trust concept. In English law the common law courts recognised only the legal owner and their property, however, the equity courts were willing to recognise the rights of persons for whose benefit the legal holder may be holding the property.

Put simply, then, a trust is a relationship which exists where A holds property for the benefit of B. A is known as the trustee and is the legal owner of the property which is held on trust for the beneficiary B. The trustee can be an individual, group of individuals or a company. There can be more than one trustee and there can be more than one beneficiary. Where there is only one beneficiary the trustee and beneficiary must be different if the trust is to be valid.

The courts will very strictly enforce the nature of the trustee’s obligations to the beneficiaries so that, while the trustee is the legal owner of the relevant property, the property must be used only for the benefit of the beneficiaries. Trustees have what is known as a fiduciary duty towards beneficiaries and the courts will always enforce this duty rigorously.

The nature of the trustee’s duty is often misunderstood in the context of family trusts where the trustees and beneficiaries are not at arm’s length. For instance, one or more of the parents may be trustees and the children beneficiaries. The children have rights under the trust which can be enforced at law, although it is rare for this to occur.

Types of trusts

In general terms the following types of trusts are most frequently encountered in asset protection and investment contexts:

Fixed trusts

Unit trusts

Discretionary trusts – Family Trusts

Bare trusts

Hybrid trusts

Testamentary trusts

Superannuation trusts

Special Disability Trusts

Charitable Trusts

Trusts for Accommodation – Life Interests and Rights of Residence

A common issue with all trusts is access to income and capital. Depending on the type of trust that is used, a beneficiary may have different rights to income and capital. In a discretionary trust the rights to income and capital are usually completely at the discretion of the trustee who may decide to give one beneficiary capital and another income. This means that the beneficiary of such a trust cannot simply demand payment of income or capital. In a fixed trust the beneficiary may have fixed rights to income, capital or both.

Fixed trusts

In essence these are trusts where the trustee holds the trust assets for the benefit of specific beneficiaries in certain fixed proportions. In such a case the trustee does not have to exercise a discretion since each beneficiary is automatically entitled to his or her fixed share of the capital and income of the trust.

Unit trusts

These are generally fixed trusts where the beneficiaries and their respective interests are identified by their holding “units” much in the same way as shares are issued to shareholders of a company.

The beneficiaries are usually called unitholders. It is common for property, investment trusts (eg managed funds) and joint ventures to be structured as unit trusts. Beneficiaries can transfer their interests in the trust by transferring their units to a buyer.

There are no limits in terms of trust law on the number of units/unitholders, however, for tax purposes the tax treatment can vary depending on the size and activities of the trust.

Discretionary trusts – Family Trusts

These are often called “family trusts” because they are usually associated with tax planning and asset protection for a family group. In a discretionary trust the beneficiaries do not have any fixed interests in the trust income or its property but the trustee has a discretion to decide whether anyone will receive income and/or capital and, if so, how much.

For the purposes of trust law, a trustee of a discretionary trust could theoretically decide not to distribute any income or capital to a beneficiary, however, there are tax reasons why this course of action is usually not taken.

The attraction of a discretionary trust is that the trustee has greater control and flexibility over the disposition of assets and income since the nature of a beneficiary’s interest is that they only have a right to be considered by the trustee in the exercise of his or her discretion.

Bare trusts

A bare trust exists when there is only one trustee, one legally competent beneficiary, no specified obligations and the beneficiary has complete control of the trustee (or “nominee”). A common example of a bare trust is used within a self-managed fund to hold assets under a limited recourse borrowing arrangement.

Hybrid trusts

These are trusts which have both discretionary and fixed characteristics. The fixed entitlements to capital or income are dealt with via “special units” which the trustee has power to issue.

Testamentary trusts

As the name implies, these are trusts which only take effect upon the death of the testator. Normally, the terms of the trust are set out in the testator’s will and are often used when the testator wishes to provide for their children who have yet to reach adulthood or are handicapped.

Superannuation trusts

All superannuation funds in Australia operate as trusts. This includes self-managed superannuation funds.

The deed (or in some cases, specific acts of Parliament) establishes the basis of calculating each member’s entitlement, while the trustee will usually retain discretion concerning such matters as the fund’s investments and the selection of a death benefit beneficiary.

The Federal Government has legislated to establish certain standards that all complying superannuation funds must meet. For instance, the “preservation” conditions, under which a member’s benefit cannot be paid until a certain qualification has been reached (such as reaching age 65), are a notable example.

Special Disability Trusts

Special Disability Trusts allow a person to plan for the future care and accommodation needs of a loved one with a severe disability. Find out more in this Q & A about Special Disability Trusts.

Charitable Trusts

You may wish to provide long term income benefit to a charity by providing tax free income from your estate, rather than giving an immediate gift. This type of trust is effective if large amounts of money are involved and the purpose of the gift suits a long term benefit e.g. scholarships or medical research.

Trusts for Accommodation – Life Interests and Right of Residence

A Life Interest or Right of Residence can be set up to provide for accommodation for your beneficiary. They are often used so that a family member can have the right to live in the family home for as long as they wish. These trusts can be restrictive so it is particularly important to get professional advice in deciding whether such a trust is right for your situation.

Establishing a trust

Although a trust can be established without a written document, it is preferable to have a formal deed known as a declaration of trust or a deed of settlement. The declaration of trust involves an owner of property declaring themselves as trustee of that property for the benefit of the beneficiaries. The deed of settlement involves an owner of property transferring that property to a third person on condition that they hold the property on trust for the beneficiaries.

The person who transfers the property in a settlement is said to “settle” the property on the trustee and is called the “settlor”.

In practical terms, the original amount used to establish the trust is relatively small, often only $10 or so. More substantial assets or amounts of money are transferred or loaned to the trust after it has been established. The reason for this is to minimise stamp duty which is usually payable on the value of the property initially affected by the establishing deed.

The identity of the settlor is critical from a tax point of view and it should not generally be a person who is able to benefit under the trust, nor be a parent of a young beneficiary. Special rules in the tax law can affect such situations.

Also critical to the efficient operation of a trust is the role of the “appointor”. This role allows the named person or entity to appoint (and usually remove) the trustee, and for that reason, they are seen as the real controller of the trust. This role is generally unnecessary for small superannuation funds (those with fewer than five members) since legislation generally ensures that all members have to be trustees.

The trust fund

In principle, the trust fund can include any property at all – from cash to a huge factory, from shares to one contract, from operating a business to a single debt. Trust deeds usually have wide powers of investment, however, some deeds may prohibit certain forms of investment.

The critical point is that whatever the nature of the underlying assets, the trustee must deal with the assets having regard to the best interests of the beneficiaries. Failure to act in the best interests of the beneficiaries would result in a breach of trust which can give rise to an award of damages against the trustee.

A trustee must keep trust assets separate from the trustee’s own assets.

The trustee’s liabilities

A trustee is personally liable for the debts of the trust as the trust assets and liabilities are legally those of the trustee. For this reason if there are significant liabilities that could arise a limited liability (private) company is often used as trustee.

However, the trustee is entitled to use the trust assets to satisfy those liabilities as the trustee has a right of indemnity and a lien over them for this purpose.

This explains why the balance sheet of a corporate trustee will show the trust liabilities on the credit side and the right of indemnity as a company asset on the debit side. In the case of a discretionary trust it is usually thought that the trust liabilities cannot generally be pursued against the beneficiaries’ personal assets, but this may not be the case with a fixed or unit trust.

Powers and duties of a trustee

A trustee must act in the best interests of beneficiaries and must avoid conflicts of interest. The trustee deed will set out in detail what the trustee can invest in, the businesses the trustee can carry on and so on. The trustee must exercise powers in accordance with the deed and this is why deeds tend to be lengthy and complex so that the trustee has maximum flexibility.

Who can be a trustee?

Any legally competent person, including a company, can act as a trustee. Two or more entities can be trustees of the same trust.

A company can act as trustee (provided that its constitution allows it) and can therefore assist with limited liability, perpetual succession (the company does not “die”) and other advantages. The company’s directors control the activities of the trust. Trustees’ decisions should be the subject of formal minutes, especially in the case of important matters such as beneficiaries’ entitlements under a discretionary trust.

Trust legislation

All states and territories of Australia have their own legislation which provides for the basic powers and responsibilities of trustees. This legislation does not apply to complying superannuation funds (since the Federal legislation overrides state legislation in that area), nor will it apply to any other trust to the extent the trust deed is intended to exclude the operation of that legislation. It will usually apply to bare trusts, for example, since there is no trust deed, and it will apply where a trust deed is silent on specific matters which are relevant to the trust – for example, the legislation will prescribe certain investment powers and limits for the trustee if the deed does not exclude them.

Income tax and capital gains tax issues

Because a trust is not a person, its income is not taxed like that of an individual or company unless it is a corporate, public or trading trusts as defined in the Income Tax Assessment Act 1936. In essence the tax treatment of the trust income depends on who is and is not entitled to the income as at midnight on 30 June each year.

If all or part of the trust’s net income for tax purposes is paid or belongs to an ordinary beneficiary, it will be taxed in their hands like any other income. If a beneficiary who is entitled to the net income is under a “legal disability” (such as an infant), the income will be taxed to the trustee at the relevant individual rates.

Income to which no beneficiary is “presently entitled” will generally be taxed at highest marginal tax rate and for this reason it is important to ensure that the relevant decisions are made as soon as possible after 30 June each year and certainly within 2 months of the end of the year. The two month “period of grace” is particularly relevant for trusts which operate businesses as they will not have finalised their accounts by 30 June. In the case of discretionary trusts, if this is done the overall amount of tax can be minimised by allocating income to beneficiaries who pay a relatively low rate of tax.

The concept of “present entitlement” involves the idea that the beneficiary could demand immediate payment of their entitlement.

It is important to note that a company which is a trustee of a trust is not subject to company tax on the trust income it has responsibility for administering.

In relation to capital gains tax (CGT), a trust which holds an asset for at least 12 months is generally eligible for the 50% capital gains tax concession on capital gains that are made. This discount effectively “flows” through to beneficiaries who are individuals. A corporate beneficiary does not get the benefit of the 50% discount. Trusts that are used in a business rather than an investment context may also be entitled to additional tax concessions under the small business CGT concessions.

Since the late 1990s discretionary trusts and small unit trusts have been affected by a number of highly technical measures which affect the treatment of franking credits and tax losses. This is an area where specialist tax advice is essential.

Why a trust and which kind?

Apart from any tax benefits that might be associated with a trust, there are also benefits that can arise from the flexibility that a trust affords in responding to changed circumstances.

A trust can give some protection from creditors and is able to accommodate an employer/employee relationship. In family matters, the flexibility, control and limited liability aspects combined with potential tax savings, make discretionary trusts very popular.

In arm’s length commercial ventures, however, the parties prefer fixed proportions to flexibility and generally opt for a unit trust structure, but the possible loss of limited liability through this structure commonly warrants the use of a corporate entity as unitholder ie a company or a corporate trustee of a discretionary trust.

There are strengths and weaknesses associated with trusts and it is important for clients to understand what they are and how the trust will evolve with changed circumstances.

Trusts which incur losses

One of the most fundamental things to understand about trusts is that losses are “trapped” in the trust. This means that the trust cannot distribute the loss to a beneficiary to use at a personal level. This is an important issue for businesses operated through discretionary or unit trusts.

Establishment procedures

The following procedures apply to a trust established by settlement (the most common form of trust):

Decide on Appointors and back-up Appointors as they are the ultimate controllers of the trust. They appoint and change Trustees.

Settlor determined to establish a trust (should never be anyone who could become a beneficiary)

Select the trustee. If the trustee is a company, form the company.

Settlor makes a gift of money or other property to the trustee and executes the trust deed. (Pin $10 to the front of the register is the most common way of doing this)

Apply for ABN and TFN to allow you open a trust bank account

Establish books of account and statutory records and comply with relevant stamp duty requirements (Hint: Get your Accountant to do this)

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

There are all sorts of unexpected consequences coming out of the changes to the superannuation rules. As a result of moving funds over $1.6m back to accumulation to meet the Transfer Balance Cap (TBC), you may in fact now qualify for the Commonwealth Seniors Health Care card.

How?

There may be a silver lining to the new $1.6 million transfer balance cap (TBC) for some SMSF members. Having less money in an account based pension and more money in accumulation or other assets may result in some SMSF members being entitled to receive the Commonwealth Seniors Health Card (CSHC). This is because amounts held in accumulation phase are not deemed for the CSHC and are not included in a member’s personal taxable income.

Now if the excess over the $1.6m is/was withdrawn out of superannuation, whether it will count as income for the CHSC will depend on how the client invests it. for example financial investments such as shares, rented investment property and interest will be deemed but a Holiday home not rented out will not be deemed towards the CSHC income test.

Older pensions may be even more forgiving!

Income from an account based pension is deemed under the usual Centrelink deeming rates unless the account based pension commenced before 1 January 2015, and the client was entitled to the card before 1 January 2015 and continues to hold the card. This is known as the grandfathering rules.

For SMSF members who are not eligible for the grandfathering rules, holding a significant amount of money in an account based pension means that they have a lower likelihood of being eligible for a CSHC. Prior to 1 July 2017, for most SMSF members it was more beneficial to hold as much as possible in an account based pension for tax purposes even if this meant they were ineligible for the CSHC. The tax savings on the excess would have outstripped the CSHC benefit.

However, from 1 July 2017, SMSF members can only hold up to $1.6 million in an account based pension and if they are also receiving defined benefit pension income the amount which can be held in account based pensions will be lower. Depending on other income the member receives, this may result in them now being entitled to the CSHC.

You don’t believe me? The following example explains how this works in a simple scenario:

Example – single person

James is single and is age 67. In the 2016 -2017 financial year, he had $2 million in his account based pension, and no other income.

The deemed income from his account based pension is calculated as $64,247 based on deeming rates and thresholds as at 1 July 2017. His deemed income exceeds the income threshold of $52,796 for the CSHC and therefore he is not entitled to a CSHC.

On 30 June 2017, he rolls $400,000 back to accumulation leaving $1.6million in his account based pension.

The deemed income on $1.6 million is $51,247 and is under the income threshold of $52,796 (20 March 2017) meaning that James is entitled to a CSHC after rolling back money from his account based pension to accumulation.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Client Question : My next question is about the threshold income level at which my wife and I will start to pay personal tax in 2017-18. I read “about $28,000” in the paper the other day for my situation (age >65), but my wife does not turn 65 until 2018, so her tax-free level may be different. It would be useful to know these numbers in the case we decide to take some lump sums out of super because of the new limits. We are considering investing some money tax-free in our personal names, free of SMSF red tape.

Personal Tax-free Thresholds

The amount you can earn before you have to pay tax, actually depends on your age.

Under 65

For those people under age 65, the effective tax-free threshold is currently $20,542. How do we calculate this amount? Well, if you look at the ATO’s current Individual income tax rate table, you pay no tax on the first $18,200 you earn in a year.

However, you also get the benefit of the full low income tax offset if you earn below $37,000. That means the tax office will offset up to $445 from the tax you would normally have to pay. So you can earn another couple of thousand dollars before you have to pay tax.

How much can I earn before paying taxes after age 65

For those who have reached age pension age, they can earn even more without paying tax. If you are over 65, you get access to the Seniors and Pensioners Tax Offset (SAPTO). This reduces or eliminates the tax that would normally be liable to pay on some additional income

Using the SAPTO benefit, the amount you can earn each year as a pensioner before having to pay tax, is:

$32,279 for single people,

$28,974 each for members of a couple or $57,948 combined.

The beauty of this benefit is that for clients in SMSF Pension phase any income drawn from a super fund income stream once over 60 is tax-free and non-assessable, meaning it doesn’t count towards the above thresholds.

Based on an earnings rate of 5% this means that a couple could have over $500,000 in each of their names and not pay any tax. But be careful as if you are investing in growth assets then triggering capital gains in the future may mean exceeding these thresholds where as within the SMSF the CGT on pension assets is NIL and 10-15% in accumulation.

Also consider the tax position if you are likely:

to receive an inheritance

large capital gain on an asset he’d outside super

to have one parter live significantly longer (they may end up with large amounts outside the super system)

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Tax free Image courtesy of Stuart Miles /FreeDigitalPhotos.net

Suppose the government had about A$10 billion a year to fund lower income tax. It could reduce personal income tax by about 6%, or lower each marginal rate by about 1.5 percentage points. Alternatively it could reduce company tax by about 15%, or reduce the current 30% rate to 24%. Which option has more merit?

But the answer as to which is more likely to drive the “jobs and growth” the government has been promising is not that simple. And it is difficult if not impossible to comprehensively model which option is better.

Income tax affects households differently

The two lower income tax options have different implications for the distribution of the tax burden over time. They also impact changes in incentives and rewards to promote a larger economy and higher future living standards, and how much can be clawed back after the first round revenue loss.

A reduction of personal income tax rates provides a more direct and explicit increase in household income, and a quicker gain, when compared with a reduction of the corporate tax rate. Also, lower personal tax rates allow greater government discretion in the distribution of the benefits across households with different incomes, demographic and other characteristics.

Company tax cuts can impact wages and investment

Individuals benefit from lower corporate tax rates with higher market wages. But the higher wage rates will take some years to materialise, and the magnitude of increase attributed to the lower corporate tax rate, versus other factors, is open to debate.

Benefits of a lower corporate tax rate, and in time the flow of these benefits as higher wage rates, involves a chain of decision changes. Australian corporations depend on the savings of international investors for an important share of their investment funds. They use this money to invest in machinery, buildings technology and so forth. But to get it they must show investors they will get a superior return, after Australian corporate income tax is paid, compared to alternative investments in other countries.

If Australia’s company tax rate was cut, this would lower the bar on the required return to attract investment. In the end the lower corporate tax rate induces an increase in investment, resulting in a larger stock of capital and associated technology and expertise. But, this capital accumulation process takes many years.

The enlarged stock of capital, technology and expertise per worker becomes a key driver of increased worker productivity. In time, more productive workers are able to negotiate higher wages. Via this chain of decision changes, employees benefit from the lower corporate tax rate.

Personal tax cuts promote productivity

Lower personal income tax rates provide incentives for a more productive economy and higher living standards through two main mechanisms. Lower marginal income tax rates increase the incentive for, and the rewards from, joining the workforce, working more hours, and putting more into education and skill acquisition. These incentives are especially important for women with children and older workers.

Also, lower personal income tax rates reduce distortions to household decisions on how much to save and where to invest savings in owner occupied homes, other property, financial deposits, shares, superannuation and other options.

The current income tax system imposes different forms of income tax on the different options with very different effective tax rates. For example, income earned on owner occupied housing (of imputed rent and capital gains) is exempt from income tax while the nominal interest on financial deposits (associated with offsetting inflation as well as the returns for delayed consumption) faces the personal rate. Lower personal income tax rates reduce the magnitudes of the distortions caused by different effective tax rates on different saving and investment options.

The difference is in the timing

Lowering the rate of corporate or personal income tax will generate a larger and more productive economy. A larger economy means larger tax bases, and not just income tax, but also GST, payroll and excise. The enlarged tax bases generate larger tax revenues and a partial recapture over time of the first round revenue cost of the income tax rate reductions.

The revenue recapture is expected to be larger for the corporate income tax rate reduction option. With the imputation system, for domestic shareholders a reduction in corporate income tax and less franking credits would be offset by a larger direct personal income tax payment on dividend income.

The greater price sensitivity of the international supply of funds to Australia enticed by a lower corporate tax rate is expected to boost the size of the Australian economy, and tax bases, more than the labour supply response to lower personal tax rates.

Models don’t have the answer

Ultimately, quantifying the relative national productivity, distribution and revenue effects of the lower corporate tax and personal income tax options requires detailed computable general equilibrium models.

Arguably, available models, including those used by government, lack the detail of progressive personal income tax rates for different households, and details of household choices among different investment options with different effective tax rates, to confidently measure the relative effects of the two options.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Sira Anamwong at FreeDigitalPhotos.net

Rate for 2025-26 Related Property LRBA is 8.95%and Listed Shares 10.95%