Suppose the government had about A$10 billion a year to fund lower income tax. It could reduce personal income tax by about 6%, or lower each marginal rate by about 1.5 percentage points. Alternatively it could reduce company tax by about 15%, or reduce the current 30% rate to 24%. Which option has more merit?

But the answer as to which is more likely to drive the “jobs and growth” the government has been promising is not that simple. And it is difficult if not impossible to comprehensively model which option is better.

Income tax affects households differently

The two lower income tax options have different implications for the distribution of the tax burden over time. They also impact changes in incentives and rewards to promote a larger economy and higher future living standards, and how much can be clawed back after the first round revenue loss.

A reduction of personal income tax rates provides a more direct and explicit increase in household income, and a quicker gain, when compared with a reduction of the corporate tax rate. Also, lower personal tax rates allow greater government discretion in the distribution of the benefits across households with different incomes, demographic and other characteristics.

Company tax cuts can impact wages and investment

Individuals benefit from lower corporate tax rates with higher market wages. But the higher wage rates will take some years to materialise, and the magnitude of increase attributed to the lower corporate tax rate, versus other factors, is open to debate.

Benefits of a lower corporate tax rate, and in time the flow of these benefits as higher wage rates, involves a chain of decision changes. Australian corporations depend on the savings of international investors for an important share of their investment funds. They use this money to invest in machinery, buildings technology and so forth. But to get it they must show investors they will get a superior return, after Australian corporate income tax is paid, compared to alternative investments in other countries.

If Australia’s company tax rate was cut, this would lower the bar on the required return to attract investment. In the end the lower corporate tax rate induces an increase in investment, resulting in a larger stock of capital and associated technology and expertise. But, this capital accumulation process takes many years.

The enlarged stock of capital, technology and expertise per worker becomes a key driver of increased worker productivity. In time, more productive workers are able to negotiate higher wages. Via this chain of decision changes, employees benefit from the lower corporate tax rate.

Personal tax cuts promote productivity

Lower personal income tax rates provide incentives for a more productive economy and higher living standards through two main mechanisms. Lower marginal income tax rates increase the incentive for, and the rewards from, joining the workforce, working more hours, and putting more into education and skill acquisition. These incentives are especially important for women with children and older workers.

Also, lower personal income tax rates reduce distortions to household decisions on how much to save and where to invest savings in owner occupied homes, other property, financial deposits, shares, superannuation and other options.

The current income tax system imposes different forms of income tax on the different options with very different effective tax rates. For example, income earned on owner occupied housing (of imputed rent and capital gains) is exempt from income tax while the nominal interest on financial deposits (associated with offsetting inflation as well as the returns for delayed consumption) faces the personal rate. Lower personal income tax rates reduce the magnitudes of the distortions caused by different effective tax rates on different saving and investment options.

The difference is in the timing

Lowering the rate of corporate or personal income tax will generate a larger and more productive economy. A larger economy means larger tax bases, and not just income tax, but also GST, payroll and excise. The enlarged tax bases generate larger tax revenues and a partial recapture over time of the first round revenue cost of the income tax rate reductions.

The revenue recapture is expected to be larger for the corporate income tax rate reduction option. With the imputation system, for domestic shareholders a reduction in corporate income tax and less franking credits would be offset by a larger direct personal income tax payment on dividend income.

The greater price sensitivity of the international supply of funds to Australia enticed by a lower corporate tax rate is expected to boost the size of the Australian economy, and tax bases, more than the labour supply response to lower personal tax rates.

Models don’t have the answer

Ultimately, quantifying the relative national productivity, distribution and revenue effects of the lower corporate tax and personal income tax options requires detailed computable general equilibrium models.

Arguably, available models, including those used by government, lack the detail of progressive personal income tax rates for different households, and details of household choices among different investment options with different effective tax rates, to confidently measure the relative effects of the two options.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Sira Anamwong at FreeDigitalPhotos.net

Rate for 2025-26 Related Property LRBA is 8.95%and Listed Shares 10.95%

Old Rate for 2024-25 Related Property LRBA was 9.35% and Listed Shares 11.35%

The ATO have issued long-awaited guidelines providing SMSF trustees with suggested ‘Safe Harbour’ loan terms on which trustees may use to structure a related party Limited Recourse Borrowing Arrangement (LRBA) consistent with dealing at arm’s length with that related party.

By implementing these “Safe Harbour” loan terms, SMSF trustees are assured by the ATO Commissioner that

..for income tax purposes, the Commissioner accepts that an LRBA structured in accordance with this Guideline is consistent with an arm’s length dealing and that the NALI provisions do not apply purelybecause of the terms of the borrowing arrangement.

It is absolutely essential that all non-bank SMSF borrowing arrangements (LRBAs) be reviewed prior now extended to 1 Jan 2017

Where has this come from?

The ATO first released and then re-issued ATO Interpretative Decisions in 2015 (ATO ID 2015/27 and ATO ID 2015/28), dealing with Non-Arm’s Length Income(NALI) derived from listed shares and real property purchased by an SMSF under an LRBA involving a related party lender – where the terms of the loan were not deemed to be on commercial terms.

These ATOIDs state that the use of a non-arm’s length LRBA gives rise to NALI in the SMSF. Broadly, the rationale for this view is that the income derived from an investment that was purchased using a related party LRBA, where the terms of the loan are more favorable to the SMSF, is more than the income the fund would have derived if it had otherwise being dealing on an arm’s length basis.

NALI is taxed at the top marginal tax rate, currently 47% – regardless of whether the income is derived while the fund is in accumulation phase where tax is normally 15% or in pension phase when the income would usually be tax exempt.

After that bombshell, the ATO announced that it would not take proactive compliance action from a NALI perspective against an SMSF trustee where an existing non-commercial related party LRBA was already in place, as long as such an LRBA was brought onto commercial terms or wound up by 30 June 2016.

The Nitty Gritty Details of the Safe Harbour Steps

The ATO has issued Practical Compliance Guideline PCG 2016/5. As a result, provided an SMSF trustee follows these guidelines in good faith, they can be assured that (for income tax compliance purposes) their arrangement will be taken to be consistent with an arm’s length dealing.

The ‘Safe Harbour’ provisions are for any non-bank LRBA entered into before 30 June 2016, and also those that will be entered into after 30 June 2016.

Broadly, this PCG outlines two ‘Safe Harbours’. These Safe Harbours provide the terms on which SMSF trustees may structure their LRBAs. An LRBA structured in accordance with the relevant Safe Harbour will be deemed to be consistent with an arm’s length dealing and the NALI provisions will not apply due merely to of the terms of the borrowing arrangement.

The terms of the borrowing under the LRBA must be established and maintained throughout the duration of the LRBA in accordance with the guidelines provided.

Safe Harbour 1

Safe Harbour 2

Asset Type

Investment in Real Property

Investment in a collection of Listed Shares or Units

Interest RateNote: as of 10 Jan 2019: The RBA no longer round the rates to the nearest 5 basis points.

RBA Indicator Lending Rates for banks providing standard variable housing loans for investors. Use the May rate immediately preceding the tax year. (2015/16 year = 5.75%)(2016-17 year = 5.65%)(2017-18 year = 5.8%)(2018-19 year = 5.8%)(2019-2020 year = 5.94%)(2020-2021 year = 5.1%) (2021-2022 year = 5.1%)(2022-2023 year = 5.35%)2024 FY = 8.85% (2024-25 year = 9.35%) (2025-26 year 8.95%)

Same as Real Property + a margin of 2%

Fixed / Variable

Interest rate may be fixed or variable.

Interest rate may be fixed or variable.

Term of Loan

Variable interest rate loans:Original loan – 15 year maximum loan term (both residential and commercial).Re-financing – maximum loan term is 15 years less the duration(s) of any previous loan(s) in respect of the asset (for both residential and commercial).Fixed interest rate loan:

Rate may be fixed for a maximum period of 5 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 5.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 5 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 15 years.

Variable interest rate loans:Original loan – 7 year maximum loan term.Re-financing – maximum loan term is 7 years less the duration(s) of any previous loan(s) in respect of the collection of assets.Fixed interest rate loan:

Rate may be fixed up to for a maximum period of 3 years and must convert to a variable interest rate loan at the end of the nominated period. The total loan term cannot exceed 7 years.

For an LRBA in existence on publication of these guidelines, the trustees may adopt the rate of 7.75% as their fixed rate provided that the total period for which the interest rate is fixed does not exceed 3 years. The interest rate must convert to a variable interest rate loan at the end of the nominated period. The total loan cannot exceed 7 years.

Loan-Value –RatioLVR

Maximum 70% LVR for both commercial & residential property. Total LVR of 70% if more than one loan.

Maximum 50% LVR.Total LVR of 50% if more than one loan.

Security

A registered mortgage over the property.

A registered charge/mortgage or similar security (that provides security for loans for such assets).

Personal Guarantee

Not required

Not required

Nature & frequency of repayments

Each repayment is to be both principal and interest.Repayments to be made monthly.

Each repayment is to be both principal and interest.Repayments to be made monthly.

Loan Agreement

A written and executed loan agreement is required.

A written and executed loan agreement is required.

Information sourced from Practical Compliance Guidelines PCG 2016/5.

Potential Trap to be aware of: Importantly, as part of this announcement, the ATO also indicated that the amount of principal and interest payments actually made with respect to a borrowing under an LRBA for the year ended 30 June 2016 must be in accordance with terms that are consistent with an arm’s length dealing.Information sourced from Practical Compliance Guidelines PCG 2016/5.

For the 2017-18 and 2018-19 years the rate is 5.8%

For the 2019-20 year the rate is 5.94%

For the 2020-21 year the rate is 5.1%

For the 2021-22 year the rate is 5.1%

For the 2022-23 year the rate is 5.35%

For the 2023-24 year the rate is 8.85%

For the 2024-25 year the rate is 9.35% until 30 June 2025

For the 2025-26 year the rate is 8.95%

For 2019-20 and later years, the rate published for May (the rate for the month of May immediately prior to the start of the relevant financial year)

It is the applicable rate under Column H of the above spreadsheet (click on link). The rate seems to have started in August 2015 but I assume we must use the May rate from now on.

In referencing the Indicator Rate you can use: Ref: Title: Lending rates; Housing loans; Banks; Variable; Standard; Investor Lending rates; Housing loans; Banks; Variable; Standard; Investor Frequency: Monthly Units: Per cent per annum Source RBA Publication Date 04-Apr-2016 Series ID: FILRHLBVSI

A complying SMSF borrowed money under an LRBA, using the funds to acquire commercial property valued at $500,000 on 1 July 2011.

The borrower is the SMSF trustee.

The lender is an SMSF member’s father (a related party).

A holding trust has been established, and the holding trust trustee is the legal owner of the property until the borrowing is repaid.

The loan has the following features:

the total amount borrowed is $500,000

the SMSF met all the costs associated with purchasing the property from existing fund assets.

the loan is interest free

the principal is repayable at the end of the term of the loan, but may be repaid earlier if the SMSF chooses to do so

the term of the loan is 25 years

the lender’s recourse against the SMSF is limited to the rights relating to the property held in the holding trust, and

the loan agreement is in writing.

We do not consider that this LRBA has been established or maintained on arm’s length terms. The income earned from the property, which is rented to an unrelated party, may give rise to NALI.

At 1 July 2015, the property was valued at $643,000, and the SMSF has not repaid any of the principal since the loan commenced.

If after considering TD 2016/16, it is determined that the income earned from the property is in fact NALI, to avoid having to report NALI for the 2015-16 year (and prior years) the Fund has a number of options.

Option 1 – Alter the terms of the loan to meet guidelines

The SMSF and the lender could alter the terms of the loan arrangement to meet Safe Harbour 1 (for real property).

To bring the terms of the loan into line with this Safe Harbour, the trustees of the SMSF must ensure that:

The 70% LVR is met (in this case, the value of the property at 1 July 2015 may be used).

Based on a property valuation of $643,000 at 1 July 2015, the maximum the SMSF can borrow is $450,100. The SMSF needs to repay $49,900 of principal as soon as practical before 30 June 2016.

The loan term cannot exceed 11 years from 1 July 2015.

The SMSF must recognise that the loan commenced 4 years earlier. An additional 11 years would not exceed the maximum 15 year term.

The SMSF can use a variable interest rate. Alternatively, it can alter the terms of the loan to use a fixed rate of interest for a period that ensures the total period for which the rate of interest is fixed does not exceed 5 years. The loan must convert to a variable interest rate loan at the end of the nominated period.

The interest rate of 5.75% applies for 2015-16 and 5.65% p.a. applies from 1 July 2016 to 30 June 2017. The SMSF trustee must determine and pay the appropriate amount of principal and interest payable for the year. This calculation must take the opening balance of $500,000, the remaining term of 11 years, and the timing of the capital repayment, into account.

After 1 July 2016, the new LRBA must continue under terms complying with the ATO’s guidelines relating to real property at all times.

For example, the SMSF must ensure that it updates the interest rate used for the loan on 1 July each year (if variable) or as appropriate (if fixed), and make monthly principal and interest repayments accordingly.

Option 2 – Refinance through a commercial lender

The fund could refinance the LRBA with a commercial lender, extinguish the original arrangement and pay the associated costs.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant part of the 2015-16 year.

Option 3 – Payout the LRBA

The SMSF may decide to repay the loan to the related party, and bring the LRBA to an end before 30 January 2017.

For any period after 1 July 2015 that the original loan remains in place, the SMSF must ensure that the terms of the loan are consistent with an arm’s length dealing, and the relevant amounts of principal and interest are paid to the original lender.

The SMSF may choose to apply the terms set out under Safe Harbour 1 to calculate the amounts of principal and interest to be paid to the original lender for the relevant period.

Each option will have many advantages and disadvantages – so it is important to understand what the practical implications of each option are, and how physically you will approach each option. Seek specialised advice on this matter as it is not a strategy suitable for DIY implementation

Important Note to 13.22C or Unrelated Unit Trust Investors

The guidelines provided in this PCG are not applicable to an SMSF LRBA involving an investment in an unlisted company or unit trust (e.g. where a related party LRBA has been entered into to acquire a collection of units in an unrelated private trust or a 13.22C compliant trust). As such, trustees who have entered into such an arrangement will have no option but to benchmark their particular loan arrangement based on commercial loan terms, or to bring the LRBA to an end.

Please visit out SMSF Property page to get details on all available strategies for SMSF property investors.

UPDATE (Relief for those caught by Budget measures)

In a letter to an industry association, the Treasurer, Scott Morrison, has outlined transitional arrangements to allow additional non-concessional contributions above the proposed lifetime limit in certain limited circumstances. Contributions made in the following circumstances may be permitted without causing a breach of the lifetime cap:

where the trustees of a self managed superannuation fund (SMSF) have entered into a contract to purchase an asset prior to 3 May 2016 that completes after this date and non-concessional contributions were planned to be made to complete the contract of sale. Non-concessional contributions will be permitted only to allow the contract to complete provided they are within the relevant non-concessional cap that was applicable prior to Budget night, and

where additional contributions are made in order to comply with the Australian Taxation Office’s (ATO) Practical Compliance Guideline (PCG) 2016/5 related to limited recourse borrowing arrangements, provided they are made prior to 31 January 2017.

Additional non-concessional contributions made under these proposed transitional arrangements will count towards the lifetime cap, but will not result in an excess.

I hope this guidance has been helpful and please take the time to comment. Feedback always appreciated. Please reblog, retweet, like on Facebook etc to make sure we get the news out there. As always please contact me if you want to look at your own options. We have offices in Castle Hill and Windsor but can meet clients anywhere in Sydney or via Skype. Click here for appointment options.

Liam Shorte B.Bus FSSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 9899 3693, Mobile: 0413 936 299

PO Box 6002, Norwest NSW 2153

U40, 8 Victoria Ave., Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Until recently, I tended to base retirement planning strategies for clients on a book from the late 90s titled The Prosperous Retirement: Guide to the New Reality by Michael Stein.

Stein divided retirement into 3 stages. Each of these stages affected spending patterns differently, so we could plan for clients’ needs at each stage.

Under the accepted system, the first stage is the Active stage — those first early retirement years when most people are looking to see the world (or at least Australia) and/or engage in other active pursuits. They’ve suddenly got 50-60 more hours per week of free time and are still healthy enough to get out there and make the most of life and opportunities.

The second is the Passive stage — a time when they still look forward to some travel and active pursuits but, with the onset of age-related injuries and illnesses, just not as often as when they first retired. Maybe they’d take shorter trips around parts of Australia rather than long overseas trips through three countries at a time.

Then, eventually retirees move into the last stage, the Sedentary stage, when physical or mental limitations — or setbacks like the death of a spouse or close friends — lead to a much more sedentary, home-based lifestyle. It may also involve losing independence and increasing dependency on others.

The new stage of retirement

In my experience, I’m seeing a new stage of retirement forming, that can have a major effect on people. This new stage has to be managed carefully.

It happens between just retired and the first stage, the Active stage. I call it the Family Support stage.

This is a stage where more and more newly retired people are finding themselves as almost full-time carers for their grandchildren, meaning they cannot plan to travel, undertake volunteering or pursue personal activities due to commitments they make to help struggling children.

This is not the traditional, one-day-a-week “day with nanny and pop,” but a full on five, sometimes six-days-a-week commitment. Often this commitment comes the added cost of taking care of the grandchildren. The costs may not be recovered from their parents, who are often battling a huge mortgage and/or an expensive lifestyle, so the grandparents pick up the tab and deplete their own savings in doing so. You just need to plan for these expenses that can blow out a retirement budget.

I am not saying this is a major negative, as many people cherish time with their grandchildren and would not swap it for the world. However, as a result, they need to be aware that too much time spent in the initial Family Support stage may mean they miss out completely on the most active years of retirement. Some of us may move into the Passive and Sedentary stages much sooner than expected due to illness, and in reality, some of us may not live to reach the later stages.

I usually urge clients to put limits on the commitment to family and put aside “me time” throughout the year for some personal travel and other activities. This does not mean going on holidays with the family to be the babysitters while parents relax. I often recommend that you ensure that Fridays and Mondays are free so you can go away for long weekends so make sure your children know this upfront so they can plan what days they need alternative arrangements.

It is important to put these limits in place at the outset, as kids may come to rely on the arrangements and so they are hard to reverse later. If people do not plan, then they can end up at the wrong end of their 70s with no energy left to embark on their dream retirement.

What do you think? What are your arrangements like in the family? Are child care costs bringing you down? You can comment if you scroll down further.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of photostock at FreeDigitalPhotos.net

OK I am going to be a bit morbid today but based on the lack of preparation by many new clients I think we need to talk death, mental incapacity and other things legal. Why me? Because for some reason many seem scared of lawyers so I want to give you good reasons to overcome that fear!

When did you last review your will, your enduring power of attorney (“EPOA”) and your appointment of enduring guardian (“EG”) documents and of course your SMSF Trust Deed.

As a financial planner we recommend you personally review these documents every 3 years and have a solicitor review them every 5 years. Just take them out (if you haven’t forgotten the “safe place” you put them!) and have a look through them after considering changes to you family circumstances including the following triggers.

So here is a list of the changes to your circumstances that should prompt you to review these documents as soon as possible and which may even require you to create new documents or update existing ones.

These changes include:

1. Setting up an SMSF or making a large or non-standard investment via your SMSF

Ok as a SMSF blog you know I had to deal with this first. When you first set up an SMSF you may have been told to read the deed but did anyone tell you it’s essential to appoint your Enduring Power of Attorney to ensure the SMSF can continue to run smoothly if your health deteriorates.

If you decide to make an unusual investment or loan or arrangement in your fund the you must first know that your SMSF Deed and Investment Strategy allows such a move. So read the SMSF deed and have a written SMSF investment strategy.

2. Marriage automatically revokes a will, unless the will was made in contemplation of marriage. After you marry, you should make a new will.

Your Power Of Attorney is not revoked by marriage. If your EPOA was signed before your marriage it is still effective. However, if, for example, your EPOA appointed your former spouse, you may wish to formally revoke the EPOA and make a new EPOA appointing another person as your attorney.

Your appointment of an Enduring Guardian is revoked on marriage even if you appointed your current spouse as your EG. After marriage, you need to sign a new appointment of EG document.

If you wish to bring your new spouse into your SMSF then you need to follow the rules of appointing a new trustee or director and accepting a new member. Read the deed and the company trustee constitution. Don’t forget to notify ASIC.

Check your Binding Death Nomination and any reversionary pensions.

3. Separation

Unlike marriage, separation does not affect the validity of your will. As a result, there have been several cases where a couple have separated, one spouse has died after separation but before the divorce and their former spouse has been entitled to the whole of their estate either due to their failure to update their will after separating or by not having any will in place at all and the rules of intestacy applying in favour of their former spouse.

Similarly, your EPOA and EG documents will not be affected by separation. You should consider whether you need to revoke the existing appointments and make a new EPOA and appoint a new EG after separating

There maybe some allowances for the transfer of SMSF assets in the event of a finalised property settlement and again you need to understand the exceptions that apply once the financial/property settlement has been agreed and signed off and read the deed before assuming you can move or split assets.

Check your Binding Death Nomination, insurance nominations and any reversionary pensions

4. Divorce

I know I am repeating myself but Check your Binding Death Nomination , insurance nominations and any reversionary pensions.

There are specific rules allowing the transfer of SMSF assets in the event of divorce without triggering CGT or Stamp Duties and again you need to understand the exceptions, the process and read the deed before assuming you can move or split assets.

Divorce does not revoke your EPOA or EG documents appointing your former spouse. In order to cancel these appointments, you need to sign a revocation and serve it on your former spouse.

Divorce only revokes or cancels any gift made in your will to your former spouse. It also cancels your spouse’s appointment as executor, trustee or guardian in your will. It does not cancel the appointment of your former spouse as trustee of property left on trust for beneficiaries that include the children of you and your former spouse. However this will not apply if the Court is satisfied you did not intend to revoke the gift or the appointment by the divorce. Instead of leaving these matters to the Court, if you have not made a new will after separating, it is imperative that you make a new will as soon as possible after your divorce.

5. Birth of an additional beneficiary.

This is likely to necessitate a change to an existing will unless your solicitor has catered for future arrivals. This is another care where being too specific can require frequent updates and legal fees.

6. Death of a spouse, an existing beneficiary, your executor, your attorney or your EG.

Review your will, Enduring Powers of Attorney and Enduring Guardianship, Binding Death Nomination, insurance nominations and any reversionary pensions.

Do you need to appoint a new individual SMSF trustee or director to keep your SMSF compliant?

7. A change to the needs of your children or grandchildren

Review your will and look at Testamentary Trusts or Special Disability Trusts. Last thing you want is for your beneficiary to lose their Disability Pension because of an inheritance.

8. A material change in your financial circumstances.

Have you sold or transferred assets that would have formed part of your estate? Make sure you have not mistakenly left someone with nothing.

If you have been bankrupted or considering filing for bankruptcy then you will not be able to continue as a member of your SMSF. You need to look at rolling to a Small APRA fund or a retail fund.

You also need to have your own parents if still with us to reconsider any direct inheritances to you as your creditors may grab them.

9. A breakdown in a relationship with relatives or friends who you may have appointed as:

the executors of your estate;

beneficiaries under your will;

guardians of your minor children; and/or

your attorney or your EG

10. The decline in health or some other change of circumstances

For example bankruptcy of a child (let’s face it, everyone under 30 thinks they are an entrepreneur and that’s going to lead to trouble!) so that, for example, a beneficiary under your will may no longer be able to manage their own finances,

The person you appointed as your executor, your attorney or your EG may no longer be suitable or capable of administering your estate or managing your affairs or making personal decisions for you.

If it is you or your spouse who have been diagnosed with onset of dementia or Alzheimer’s for example then you need to decide if you should have your EPOA step in now rather than later to help manage your self managed superannuation fund.

11. Retirement

Retirement often results in people restructuring their affairs. This is an ideal time to be proactive in your estate planning and possibly consider setting up tax effective arrangements through your will that you have not done previously.

Have you started a pension in your SMSF? Have you documented it properly including a reversionary pension election or Binding death nomination?

Have you sold assets like a business premises or investment property previously allotted to someone specific in your will? Are they losing that benefit!

When any of these events occur, you should review your SMSF and estate planning documents and, if necessary, create new documents taking into account the relevant change of circumstances. Don’t be afraid to ask advice but make sure you are dealing with a specialist in each area.

If you have been paying attention you will notice I said “12 Triggers”. Well I’ll leave the 12th for you to add in the comments section below. Come on I must have missed a few and I know some really sharp minds read this blog so help us out! I will add the best one to this list after a month or add my own, so why not subscribe to the blog in the “Free email updates” section on the left hand-side of the page.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Adapted from an original article “Time for an estate planning “check-up” by BWS Lawyers

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

What if you are not sure a proposed investment ticks all the boxes?

While you should make your best effort to ensure that the SMSF investments in your fund are compliant with the legislation, it can often be difficult to tell whether a particular investment strategy would be compliant or not.

For example, an SMSF trustee would be able to acquire a property from a member if that property was deemed to be business real property (BRP) but while for most BRP it is obvious that it satisfies the definition like a stand alone warehouse, for other properties it is far from clear such as a retail shop with 2 residential units above it.

In this case, as trustee, you could either decide not to proceed with the acquisition or else they could seek further guidance. you should initially seek guidance from your fund Auditor and other adviser but you may often get a grey answer. While trustees always have the option of seeking legal advice, they also have the ability to go straight to the ATO to seek their opinion before entering the transaction.

The ATO can provide SMSF specific advice about the following topics:

investment rules including

an investment by an SMSF in a company or unit trust

acquisition of assets from related parties

borrowing and charges

in-house assets

business real property

in specie contributions/payments

payment of benefits under a condition of release.

You should use this service if you want specific advice about how the super law applies to a particular transaction or arrangement for a self-managed superannuation fund, but you cannot use this service for tax related questions so that is when you need to look for a Private Ruling.

Private Ruling for Tax Related Scenarios

As an SMSF Trustee, if you have a concern that your circumstances or those of the fund may put you in an unusual tax position, or that a particular financial arrangement doesn’t fit any known approach for tax purposes, or you simply wants to minimise the risk of an unanticipated tax outcome, you can apply for a ‘private ruling’ from the Tax Office.

A private ruling may deal with anything involved in the application of a relevant provision of the law, including issues relating to liability, administration and ultimate conclusions of fact (such as residency status).When you apply for a private ruling about an arrangement, you can also ask the ATO to consider whether Part IVA (general anti-avoidance rule) applies to the arrangement.

In fact a lot of the proposed SMSF projects or strategies we are asked to advise on do not have a clear definable answer. Specific advice is often required on unusual scenarios for contributions involving residency or the work test or benefit payments for those under age 65. Asking for a private ruling can be a good way to ‘test-drive’ a tax arrangement you may be considering, especially where the already existing information from the Tax Office doesn’t seem to adequately cover all the bases and you are concerned about the level of tax or penalties if you get it wrong.

You can apply for a private ruling on behalf of your SMSF yourself but I would recommend using your tax agent or tax law specialist (click here for access to the private ruling instructions, plus additional ATO guidance).

Each ruling is specific to the entity that applied for it, and only to the specific facts and situation considered by the ruling, and can’t be picked up as a standard by any other taxpayer. These are one-off decisions, made only about a certain set of circumstances, and they set out how the Tax Office views that situation.

Binding If you get a private ruling, and base your SMSF tax affairs on that advice, the Tax Office is bound to administer the tax law as set out in that ruling. But, if later, the ATO issues a public ruling and the tax outcome conflicts with the one in your private ruling, you generally have the choice of which one to apply.

A ruling made in respect of a particular tax law will be changed if that law is altered by legislation or by the result of a court decision. But it’s worthwhile remembering that if you follow a ruling’s advice, and that ruling is later found to have not applied the law correctly, that you’re protected from having to repay any tax that would have otherwise been owed, as well as interest and penalties.

If a private ruling affects one of your earlier tax assessments, the Tax Office will not automatically amend it unless you make a point of submitting a written request for an amendment.

But just because you apply for a private ruling doesn’t mean you are going to get one. The Tax Office can refuse if it thinks a ruling would prejudice or restrict the law, if you are being audited over the same issue, or if it deems your application to be ‘frivolous’ or ‘vexatious’.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why not contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

I deal everyday with people’s money and more importantly their dreams. Often we have to question clients about what they really want out of life and yes we encourage responsible saving but also a balanced lifestyle to ensure they are healthy enough to enjoy retirement and wise enough to keep relationships strong to share that retirement with loved ones and friends. This is an excellent video that shows money and fame are not the be all and end all of achieving happiness in life.

What keeps us happy and healthy as we go through life? If you think it’s fame and money, you’re not alone – but, according to psychiatrist Robert Waldinger, you’re mistaken. As the director of a 75-year-old study on adult development, Waldinger has unprecedented access to data on true happiness and satisfaction. In this talk, he shares three important lessons learned from the study as well as some practical, old-as-the-hills wisdom on how to build a fulfilling, long life.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

There has been a huge increase in Self Managed Super Funds being set up by people in their 30’s and 40’s according to ATO statistics, with 42.7% of new trustees under the age of 45. So I am going to address an issue that until now has rarely been mentioned with SMSFs strategies, as previously they were seen as the territory of crusty old men.

Maintaining momentum with your super during times out of the workforce

There finally seems to be a push on at the moment to improve the superannuation of all women in Australia. They have been lagging behind when it comes to their superannuation due to breaks in their careers as mothers or carers or because they have chosen professions that are crucial to the economy but underpaid. Statistics repeatedly show, women will retire with a super balance that’s almost half that of men. The problem of this lower level of retirement savings is compounded when you understand that women live longer and therefore need more not less super that their male cohorts.

Taking time to raise a family as a stay-at-home-mum or having part-time employment to allow for caring for a sick family member leads to loss of contributions in those critical early and later years of superannuation savings. Money that could have been invested in their 20’s or 30’s that would have compounded year on year up to retirement has been foregone. The women who also take on the burden of carer for their parents or ill spouse in later years can miss the boost in savings capacity when the mortgage has been paid off.

But what can you do for your super while we wait for politicians, business and unions to come up with a long-term solution. If you are in the position of having to take a break in your career here are five strategies for continuing to build your super during those years where employer contributions are not available.

Personal contribution to access the Government Co-Contribution

Pregnancy and illness rarely fall in line with financial years so as long as you have worked any period during a tax year you can contribute up to $1,000 of your own savings to super and also be eligible to receive a government superannuation co-contribution of up to $0.50 for every $1 of non-concessional (after-tax) contributions you make to your super account.

You will be eligible for the super co-contribution if you can answer yes to all of the following:

you made one or more eligible personal super contributions to your super account during the financial year

you pass the two income tests

your total income for the financial year is less than the higher income threshold($53,564 for 2019-20)

10% or more of your total income comes from eligible employment-related activities or carrying on a business, or a combination of both

you were less than 71 years old at the end of the financial year

you did not hold a temporary visa at any time during the financial year (unless you are a New Zealand citizen or it was a prescribed visa)

you lodged your tax return for the relevant financial year.

have a total superannuation balance less than the transfer balance cap ($1.6 million for the 2019–20 financial year) at the end of 30 June of the previous financial year

A spouse contribution is an after-tax super contribution made by your partner directly into your superannuation account. This is a good for both parties as you get a boost to your super and your partner gets a tax offset to lower their taxable income.

Your partner may be able to claim an 18% tax offset (maximum $540) on spouse contributions of up to $3,000 if:

the sum of your spouse’s assessable income, total reportable fringe benefits amounts and reportable employer super contributions was less than $37,000 from 1 July 2019

the contributions were not deductible to you

the contributions were made to a super fund that was a complying super fund for the income year in which you made the contribution

both you and your spouse were Australian residents when the contributions were made

when making the contributions you and your spouse were not living separately and apart on a permanent basis.

As is currently the case, the offset is gradually reduced for income above this level and completely phases out at income above $40,000.

For SMSF Trustees, make sure you clearly nominate in the reference or accompanying minute that this is a spouse contribution so the administrators can allocate it correctly.

Superannuation contributions splitting

This is a great way for partner to show commitment to maintaining your financial equality and showing taking care of family is a team effort. Contribution splitting which is fully explained in the linked article involves your partner directing a portion of their concessional superannuation contributions into your super account. The split occurs as a lump sum rollover and must be made in the financial year immediately after the one in which the contributions were made.

In any financial year, it is possible to split the lesser of:

Contribution splitting can be a highly effective way to build your super while you take a career break and can work even if you had done some work before the pregnancy in the tax year or if you worked part-time afterwards.

Within an SMSF you should just minute the request to split the contributions and confirm the receiving member’s eligibility and then pass that minute to the administrators or accountant. They may have template minutes available to make this easier.

Choose the right long-term investment strategy

If you are in your 20’s to early 40’s then you should not just accept the standard “core” or “balanced” asset allocation in your Superannuation fund. You have the right to choose your profile and especially as an SMSF trustee. With the preservation age of 60 and likely to rise towards 65 or 70, you should be choosing an investment asset allocation that is growth or high growth orientated to make the most of compounding returns on growth assets like shares and property during those earlier years.

Of course if you personally cannot take on that much risk without worrying then you may need to be more conservative but with some guidance and education on long-term returns and investing I believe you can step up to the higher allocations to shares and property confidently.

Personal Non-concessional contributions

Now this one may be a stretch as when you have had a baby or are caring for a sick family member, you may not be flush with savings or may be focusing on paying off the mortgage. However ,if you do have a surplus, then boosting your retirement savings with personal contributions is a good move.

Non-concessional super contributions are made by you out of your take-home (after-tax) pay, savings or for example an inheritance. You can add as little as you wish and whenever you wish subject to a maximum of $100,000 in any one year from 1 July 2017 or $300,000 if you are so lucky! using the 3 year bring forward rule.

The first $1,000 may be assessed for the government co-contributions as mentioned above, further boosting your savings.

So if you are one of the new breed of younger SMSF trustees who has to take time out for family or health reasons, you are not alone. You can maintain momentum with your super and use some or all of the above strategies to ensure your Superannuation powers ahead during time out of the workforce.

Budget 2016 had some positives for those with broken careers and one will be that you will be able to use unused contributions over a rolling 5 year period to play catch up on concessional (SG and salary sacrifice) contributions from 1 July 2018.

Are you looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

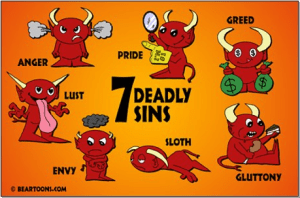

I know plenty of people prefer video content when learning so when colleagues at Eviser.com.au (free trial still running) sent me a short video link on “sloth” as an “Investment sin” I did a bit of searching and came across the whole series of these short videos below from Aberdeen Asset Management’s “Thinking Aloud” website I thought they were excellent and worth sharing to Self-Managed Super Fund Trustees. Their preface to the video series says “Don’t be led astray or make decisions for the wrong reasons.” So I encourage new and experienced SMSF Trustees to watch Aberdeen Asset Management’s guide to the seven deadly sins of multi-asset investing narrated by Joanna Lumley below

Multi-Asset Investing – Sin 1: Lust

Tip: Seeking immediate satisfaction can encourage impatient and shortsighted behavior. While a short-term view has its place, an overall less lusty approach, weathering up’s and down’s, can prove to be more fruitful in the long term.

Multi-Asset Investing – Sin 2: Gluttony

Tip: When it comes to information, less is very often more. Having the discipline to screen out market noise is likely to be key to rich investment pickings.

Multi-Asset Investing – Sin 3: Greed

Tip: Whether its equities, bonds or property, if everyone is rushing to invest, it’s probably best you don’t. The greed of the herd should always be treated with caution, take a breath, be patient. It may take a while for others to come round to your point of view, so wherever you invest, invest for the right reasons.

Multi-Asset Investing – Sin 4: Sloth

In investment, there are few shortcuts. Understanding what you’re investing in means doing the hard work, even though it’s rarely the quickest way. Only once due diligence has been done, can you truly rest comfortably.

Multi-Asset Investing – Sin 5: Wrath

Tip: When markets are plummeting and everyone is selling, it’s easy to panic, but if your portfolio is properly diversified, you can afford to be an oasis of calm. Keep a portfolio of varied assets, and you’ll be able to withstand the wrath and unpredictably of the markets.

Multi-Asset Investing – Sin 6: Envy

Tip: Imitating the index is the poorest form of flattery. Benchmark hugging is driven largely by fear. Instead of investing in assets which have just done well in the past, you should invest in those that offer the best potential for future returns.

Multi-Asset Investing – Sin 7: Pride

Tip: As we know, pride can become before a fall. Overconfidence and ignoring the warning signs can be fatal. Investors often make the same mistakes over and over again.

Are you looking for an adviser that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

If you want to add the ultimate in flexibility then look a the use of a Self Managed Superannuation Fund ( SMSF ) to allow access to a greater range of investment options for your pension, with the flexibility you need and the control you want!

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Stepping out of my comfort zone and doing some video as I am told that is what people are looking for now. I am fine when I do TV, Seminars or meetings as they are live and not scripted.

I have always been more comfortable with just speaking my mind than trying to follow my own scripted content or reciting. Takes me back to my childhood Religion class in the Christian Brothers School in Ireland when I struggled to stand up and recite the Hail Mary (a prayer we said many times each day but when I had to stand up an recite on my own I would blank and be chastised by the Brother Kenny for my lack of religious conviction). I know now that I am a story-teller and a good listener but not good at recitation!

Dave Power and his team from Power Creative let me have a delicate balance by guiding the conversation but letting me ad-lib. Hopefully the message gets through that we love helping clients achieve their goals and dreams.

If you want to add the ultimate in flexibility then look a the use of a Self Managed Superannuation Fund ( SMSF ) to allow access to a greater range of investment options for your pension, with the flexibility you need and the control you want!

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of digitalart at FreeDigitalPhotos.net

With all the talk of the government bringing out rules to tax superannuation or limit balances, I have been having some very interesting conversations with colleagues and clients, especially those whose retirement savings are expected to be in the $600,000 $900,000 level.

Many are conservative investors and would hold 30-40% of these funds in Cash and Term Deposits normally, which at current levels would earn them 2.0-3.1% at best.

They are concerned that they may not qualify for the Age Pension when the Asset Test limits apply in 2017 or lose a substantial portion of what they currently receive. Further they don’t trust that the rules for the Commonwealth Seniors Health Care card won’t tighten further so that offers no solace. Now with the added worry that the government may tax or tighten superannuation pension rules and affect them, they are looking for some alternatives that offer more security.

So I did the figures on one option I had discussed with my colleague Richard Livingston at Eviser.com.au (our online General Advice service). I looked at a couple who are currently retired and have $850,000 in assets that for example purposes are all deemed and of which $400,000 is in Term Deposits.

They currently receive $6,104 each of Age Pension per year which has helped them as the rates on their Term Deposits have dropped significantly in the preceding 5 years. The problem is that with the new asset test in 2017 they will lose that Age Pension completely or $12,208 as a couple per year.

The table below summarises these changes and the likely impacts for a home owning couple:

Table 1: Age Pension Asset test changes and impact on our clients

Asset test threshold

Couples -Home Owners

Impact on combined pensioners increase (decrease)

Announced lower threshold

(current threshold)

$375,000

($286,500)

$49 pf or $1275 p.a. extra

Announced Cut-off threshold

(current cut-off threshold)

$823,000

($1,151,500)

($510) pf or ($13,260) pa

Calculations are based on pension rates as at 20 September 2015.

Strategy to both secure some Age Pension and provide a better return that Term Deposits.

Note: this is not a recommendation to implement this strategy and you should seek personal advice before doing anything like this with your savings.

So what if instead of keeping $400,000 of their funds in Term Deposits as they currently do, they put that $200,000 in to a value adding extension to their current home (say a kitchen or extra bathroom and bedroom extension). To be clear, THEY DO NOT NEED THE EXTRA ROOM!.

Well even at the best current Term Deposit Rates, say 3%, they would lose $6,000 per year in investment income. However as their assets for Centrelink Age Pension purposes have now dropped from $850,000 to $650,000 their Age Pension would increase to $10,004 each per year until January 2017 and they would receive $6,747 each or $13,554 as a couple from 2017 onward based on current rates.

Can you see the perverse nature of using this strategy. They reduce their assessable assets by $200,000 and probably add significant value to their home if a smart extension is done while at the same time getting over $13,554 from the Age Pension as opposed to only foregoing $6,000 of investment income.

So instead of the 3% return on that Term Deposit they are getting a 6.78% per year return plus potential for increased value in their property going forward.

Is this really what we want to see? Clients refusing to downsize or actually pumping more of their savings in to their family home which is exactly what the country does not need in terms of housing affordability issues.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

Every time I see the SMSF statistical results issued by the ATO I am dismayed by the number of new SMSF funds being set up with Individual Trustees. I can only assume this is people setting up self managed superannuation funds without good advice or reasonable research.

A few times over the last 5 years I have run polls asking professionals in the SMSF industry whether they would recommend individual or corporate trustees. Every time the overwhelming result is in favour of Corporate Trustees.

So over 90% of professionals who deal day in day out with SMSF issues and like myself deal with some of the fallout when approached by grieving widows(ers), recommend a Corporate trustee for an SMSF.

I have set out my arguments for a Corporate Trustee in this previous article Why Self Managed Super Funds Should Have A Corporate Trustee. If you are considering an SMSF the I would encourage you to read through that article and feel free to pass it on to your friends, family or advisors.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

OK I realise I might have to shout a little to get people’s attention when it comes to tax and investing but while watching the recent media hype and political spat about Malcolm Turnbull investing in the Cayman Islands I did have to laugh to myself. Most Australians do not need to go that far to secure a good deal when it comes to their tax affairs.

Do you understand that someone over the age of 60 here in Australia can have an account with the following characteristics most sought after in tax havens?

Tax free income from investments

Non-reportable Income – no need to inform the tax man of your income

No Capital Gains Tax on sale of assets

I can see your eyes light up! So where can you go to organise these facilities?

YOUR SUPERANNUATION ACCOUNT CAN BECOME A TAX FREE HAVEN!

Why am I shouting? Because so many people are not making use of the tax and superannuation strategies that could put them in the exact same tax-advantaged position that a multi-millionaire has to use islands in the Pacific Ocean or Caribbean sea to achieve.

After age 56 you can start a Transition to Retirement Pension and the earnings in your fund can be tax free. From 56-59 you may some tax on the income (4%) you have to drawdown from the pension but from 60 onwards it is tax free and you don’t even have to report it on your tax return.

Don’t think it’s all too hard or it’s a scam or it seems to hard or only available to SMSF members . It is really easy and as long as you are over 56 you are 95% likely to benefit from this strategy. give me or your own adviser 5 minutes to run your figures and your will see the worthwhile savings.

I believe for most people they can save enough for 2-4 overseas holidays extra in retirement and often much more.

To learn more about superannuation Pensions here are some of my previous articles:

Don’t think your balance is too low or too high. I have clients with $50,000 to $2,500,000 in this strategy that is 100% legal. even the ATO have a video on pensions

If you want to add the ultimate in flexibility then look a the use of a Self Managed Superannuation Fund ( SMSF ) to allow access to a greater range of investment options for your pension, with the flexibility you need and the control you want!

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of digitalart at FreeDigitalPhotos.net

The Prime Minister, Malcolm Turnbull has indicated that superannuation is back on the table in terms of tax reform and that the government will look at Labor’s proposals and consider them. I have had a few calls from people reacting to this announcement in panic and considering their use of the superannuation system.

No one , especially me as an SMSF advisor , likes to see governments tinkering with the Superannuation rules and I normally see it as akin to “dipping in to a honey pot” by desperate treasurers. However the switch to completely tax-free pensions for over 60’s in the 2006 Budget was a step to far by Peter Costello.

At the time Peter Costello trumpeted them as “the most significant change to Australia’s superannuation system in decades” but what Costello and his treasury advisers did not mention or properly cost out was their long-term cost to the budget with an ageing population and economy that goes through mining and property booms and busts. I and indeed many of my clients in conversation realised that this was overly generous and we have always expected that the largesse would be rained in at some time in the future. Yes, I am prepared to resist any changes but more so to ensure the government of the day does not over step the mark and hurt the confidence in the system but I and others realise that the 2o06/7 move to tax exempt pensions for those over 60 was a too far a leap for our economy.

So what are Labor’s recommendations?

Now let’s look at the Labor proposals which are not overly draconian and will affect few people, mostly the “one percenters”. Lets look at them carefully.

Labour promised in April that if it won the election, it would impose a 15 per cent tax on the super income of retirees on all earnings of more than $75,000. Well this is per person so a pensioner couple could earn $150,000 in their SMSF or Superannuation before they have to pay any tax on earnings above this amount. The “above” is important as lets say a SMSF had $200,000 had net earnings to apportion to members for a year; well the tax would be only on the last $50,000 (assuming even balances) and would amount to $7,500 less some of the funds expenses which would become tax-deductible. Assuming a return of 6% per annum net for a super fund, the fund would have to be valued at over $2,500,000 before attracting any tax on earnings above the $75,000 per member.

Labor have also proposed a 30 per cent tax rate on contributions would apply to those on incomes from $250,000 and more, down from the current threshold of $300,000. Again this means that salary sacrifice by some earning more than $250,000 would still save them 19% per dollar as opposed to taking the money after tax at their marginal tax rates of 49% (including Medicare and Levies). so the benefit of making contribution still outweighs not saving the funds.

The old argument that these people would stop saving for retirement, spend the money and rely on government support in retirement via the age pension is just rubbish. The people affected (earning personal income over $250,000 per annum or super balances over $2,500,000) are smart enough to realise they need to take care of their own retirement and that access to the full couples pension of $33,717 is just not going to meet their needs. they will continue to use the tax, property and superannuation systems to maximise their returns using the most tax efficient options available to them.

The real danger in any change to the rules would be if a government were to change the superannuation rules to affect middle-income earners or if the media drummed up enough fear that confidence in the superannuation system was severely reduced. That is why even Labor has been careful to only target the fringes of the population or the 1% high income earners and we can also expect some degree of “Grandfathering” of any changes where anyone already committed to pension may not be affected by the changes.

The other danger is that once your start taxing pensions and increasing tax on contributions at certain limits, the temptation is always there to move the goal posts further and reduce those limits like the suggested move from additional 15% tax on contributions for earners over $300,000 to applying that additional tax to those on over $250,000 as Labor proposes. Once they start the precedence is set and future governments will find reasons to dip in deeper to our savings.

Strategies:

If you are near the edge of the limits mentioned what can you do:

Review any salary packaging options

If self-employed look to restructure your business to allow division of income across entities and family members

Make sure to even up balances using targeted withdrawals from the larger balance holder and re contributions to a lower balance spouse or partner’s account

Use Super Splitting from your 40’s onwards to ensure contributions are moved to a lower earning spouses account consistently over time to even up balances. Click hereto read more on how super splitting works.

If entitled to start a Transition to Retirement pension (TTR) do so now rather than waiting and losing the benefits of any grandfathering of changes to legislation. Click the link to read more on TTRs

In summary, I believe any changes will be targeted and that the coalition under Malcolm Turnbull will be more conservative in their changes than Labor proposes. You should however do all you can to protect your own position and use strategies available to you. It also does not harm to argue the changes and force the government to justify clearly any changes to be made to ensure they understand our displeasure at tinkering with our retirement nest eggs.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? Then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

I get enquiries from so many people now with holdings from an employee share scheme or listings such as IAG (the old NRMA) , CBA, Telstra and now Medibank Private who wish to simplify the shares held in their own personal names as they approach 67 so they don’t have to do a tax return for themselves in retirement. One option often considered is making an in specie transfer to your SMSF.

In specie is the process of transferring shares, business real property or managed funds without selling the underlying investment.

An in-specie contribution occurs when a member transfers ownership of an asset they own to the SMSF. In this case, the capital value of the fund has increased and the increase in value is considered a contribution for the member whose member balance has grown.

While most superannuation funds can accept in-specie contributions, it occurs far more commonly with SMSFs than with industry or retail superannuation funds.